Case for Africa

13 February 2014 | Investments | General | Johan Steyn, Prescient

Africa as an investment destination has been receiving a lot of attention in the popular press as international investors are increasingly scanning the globe in search of yield. The presence of more accommodative monetary policies globally has resulted in large amounts of liquidity in global financial markets. In the current low interest rate environment in developed markets, investors are more and more forced into a risk-on mind-set in order to generate decent real returns. This is where Africa with its higher economic growth and the potential for higher investment returns has captured the attention of money managers. There are a number of major trends that have resulted in making an allocation to Africa an attractive option.

Economic Growth

Over the past decade structural and economic reforms across the African continent have generally lead to substantial improvement of government budget deficits, significant advances in controlling inflation and the creation of foreign currency reserves. This has set many African countries on an impressive growth trajectory which is expected to continue as these countries cultivate sustainable domestic demand.

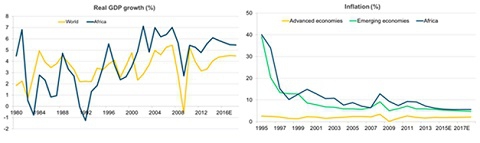

Economic growth on the continent has outpaced global growth, as seen in the chart above. According to the IMF, Africa is the second fastest growing region after Asia, and is set to take the lead going forward. Sub-Saharan economic growth is expected to be in excess of 6% in the short term, and set to exceed the average global growth for many years to come. Currently Africa only contributes to 3% of global GDP, but accounts for almost 14% of the global population.

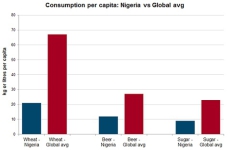

Industrialisation and economic diversification has also contributed to higher growth rates, as countries are moving away from overdependence on agriculture and resources. This also led to the emergence of the middle classes, as GDP per capita increased. Nigeria’s GDP per capita, for example, has been rising and accelerated since the return to democratic rule in 1999. The country’s GDP per capita averaged 0.1% between 1990 and 1999, with a jump to 13% between 1999 and 2011. It is from this base that the International Monetary Fund (IMF) estimated a per capita GDP growth of 5.3% over the next 5 years with GDP per capita expected to hit $2,000 by 2016. Higher levels of GDP per capita translates into higher levels of discretionary income which increases demand for goods and services that in turn drives robust, internally generated growth. As per capita consumption increases there will be a corresponding top line growth for companies positioned to take advantage of this trend. A country like Nigeria’s low consumption (in per capita terms) of basic food items and commodities such as flour, sugar and beer relative to other emerging market countries will continue to underpin a robust growth outlook for the consumer goods sector.

Source: Food and Agriculture Organisation (FAO) 2012, Prescient

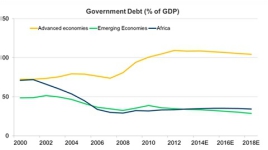

Not only do African countries produce high levels of GDP growth, but they do so with relatively low levels of government debt. This is in stark contrast to the high levels of indebtedness seen in most advanced economies. The presence of debt relief combined with sustained fiscal improvement have aided in Africa’s debt-to-GDP ratio having more than halved from around 70% in 1990 to 30% today.

Source: IMF (WEO April 2013), Prescient

Population Growth

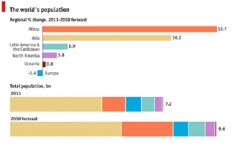

Africa is forecast to have the fastest growing population, where the population could triple to 3.6 billion by the end of the century according to a United Nations report. If current demographic trends persist, the population will increase to 1.4 billion in 2025 and 1.9 billion in 2050. One in every three children in the world will be born in Sub Saharan Africa. This rapid population growth brings both opportunities and challenges.

Source: The Economist

The most significant implication of the high population growth is the increase of the working age population. In 2010, 34 per cent of Africans were aged between 25 and 59, which is about 353 million people. By 2050 this number is expected to reach 892 million people, representing 45 per cent of the population. This would represent a dramatic shift in the world`s labour force, with Africa likely to replace China as the biggest contributor to the global workforce.

Africa also has a large youthful population. According to the United Nations World Population Prospects 2012, the average age on the continent is 18 years. Forty per cent of Africans - 416 million people - are below the age of 14 years. Mortality rates are decreasing due to improvements in health facilities, vaccination campaigns and policies to combat HIV and Malaria. Increasing moderation of the high rates of desired fertility will naturally occur as the status and education of women improve and couples increasingly recognise that they will be better off with smaller families. This slowing fertility combined with lower mortality rates will result in a demographic bonus from the positive impact of improved dependency ratios.

The challenge for governments becomes absorbing the large numbers of working age population into productive employment. However, a young, expanding and relatively cheaper workforce in Africa could persuade foreign companies to move their businesses out of Europe to countries on the African continent.

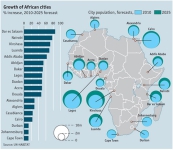

Urbanisation

Africa is as urbanised as China in terms of rural-urban split, and has as many cities of 1 million people as Europe. Nigeria’s rural-urban split is estimated at 50/50 with an urbanisation rate of 3.8% or approximately 3 million people per annum. In a report published by the OECD, before 1950, the urban population in West Africa was less than 7.5% of the total population but by 2000 this figure had risen to over 30% of the total population, thus making the rapid urbanisation of this region one of the fastest in the world. As a result of these changes, West African farmers have been developing more and more sophisticated methods of farming which have increased production to cope with the population growth. It has also seen the development of peri-urban farms specialising in food production for the urban population.

Urbanisation tends to drive consumption growth as people move from rural areas, where they predominantly practice a subsistence living, to urban areas where they begin to contribute to the formal economy. In urban areas these migrants typically have better access to education, health facilities and job opportunities. As societies become more urbanised, their productivity tends to increase. It is important to note that rapid urbanisation often brings its own challenges, especially in areas where a lack of urban planning results in overcrowding and housing shortages, as well as putting pressure on existing infrastructure such as sanitation, water and electricity.

Connectivity

Over the past decade total African mobile connections have increased from about 17 million to over 906 million, which represents a compound annual growth rate of over 30%. According to the GSMA Africa Mobile Observatory, the mobile penetration rate on the continent has grown from about 2% in 2000 to about 80% in 2013. The penetration rate is forecast to reach 85% by 2015. This substantial increase in the level of connectedness of Africans has important implications for economic growth as it serves to increase business efficacy and acts as an enabler of entrepreneurial activity. It also has significant knock-on effects as is allows companies to leverage off of the combination of improved technological development, including 4G and fibre optic networks, to access the consumer in innovative ways. An example of technological innovation in this sector is the proliferation of mobile money platforms. In Kenya, 15 million of the 41 million population actively uses Safaricom’s MPESA mobile money platform. About 80 billion Kenyan shillings are transacted between customers per month; this represents an eye-watering 31% of GDP. Not only has this innovation substantially deepened financial inclusion in Kenya, but it has also opened the door to further product innovations such as MShwari, which allows customers to take out short term loans or deposit money into a savings account using their mobile phone. This progression away from a cash based economy to a less cash intensive economy has benefits such as increases in transparency and the reduction of fraud, corruption and tax evasion. Additionally, low cash usage results in more money inside the formal economy, thus increasing the effectiveness of monetary policy in managing inflation and encouraging economic growth.

Increased privatisation and electrification

Currently Sub-Saharan Africa generates the same amount of power as Spain, although there are 20 times as many people. Electrification remains an important structural impediment to facilitating increased economic activity. In this regard some countries, like Nigeria, have made significant progress in addressing this vital shortage. After instigating a number of reforms, the country has launched itself on a privatisation drive that saw the privatisation of 10 electricity generation and 5 distribution companies in October 2012, as well as the privatisation of another 10 state power plants planned by middle 2014. By transferring the responsibility of power generation to the more efficient and effective private sector, the government is hoping to provide a sustainable supply of electricity to 75% of the population in 13 years. This has important implications for economic growth as business across the spectrum stand to benefit from a more affordable and stable power supply. By lowering the cost of doing business the government is hoping to boost the industrialisation drive and diversify the economy away from a dependence on oil. A company like United Bank for Africa, with its 700 branches across the continent, stand to benefit directly as many of their branches operate on costly diesel powered generators. Replacing the generators can shave as much as 30% off of their branch operating costs. As an enabler of entrepreneurial activity a more consistent and ubiquitous power supply will have a vital multiplier effect in creating jobs and lowering the unemployment rate.

Political Risk

African countries generally have a bad reputation when it comes to political risk. They are often perceived as being politically unstable and undemocratic. However, since the fall of the Berlin wall there has been a clear trend towards increasing stability and political maturity on the continent. The trend over the last couple of decades has seen countries moving from autocracy to semi-democracy and from semi-democracy to democracy. According to NKC Independent Economists, there were 36 autocracies and 4 democracies on the African continent in 1972. The political landscape has shifted significantly up to 2012 where there are only 5 autocracies, 24 democracies and 22 countries that can be considered partial democracies. Apart from anecdotal evidence that suggest that democratic regimes are more inclined to put in place reforms conducive to economic growth, there is empirical evidence to support a strong link between demographic transitions and both GDP growth and capital market returns (Arnott and Chaves, 2012). Of the five autocracies that are left in Africa, including Sudan, Zimbabwe and Cameroon, the despots in power are old and few have workable succession plans in place.

There is also a clear trend of increasing intolerance of political oppression by the general population. People are demanding higher levels of accountability from political leaders and are encouraged by the visible new democratic freedoms enjoyed in newly democratic African countries. A country like Kenya has proven that it is possible to conduct relatively peaceful and fair elections, as well as successfully implement constitutional reforms.

Africa is typically subject to higher volatility than more developed markets and should be approached with a long term view, which sometimes requires looking through short term fluctuations and instability. One therefore needs to critically balance the urge to react to political or economic instability with an objective and emotionless approach, and thereby avoid a kneejerk reaction that could be detrimental to the Fund. There are merits in a valuation driven investment management approach where emotions don't play an overriding role.