Bubble territory or not - should my investments change?

Debra Slabber, Portfolio Specialist at Morningstar Investment Management SA

It is hard to imagine that only a year ago, markets hit rock bottom and investors were worried about how the rest of 2020 would pan out.

Across the globe, investors were faced with questions such as - will valuations decline even further? How and when will markets recover? Is it perhaps time to deploy cash into the market? Should we disinvest and wait for better days? Should we sit on our hands and do nothing?

Today we are facing a different dilemma. Markets are at an all-time high. In a short space of time, everything has changed. The rollout of Covid-19 vaccines and associated hopes for imminent economic recovery, along with unprecedented fiscal and monetary support from governments and central banks around the world, has driven equity markets beyond or close to record highs of late. With stock market valuations at historically high levels speculation about a market bubble has been rekindled.

The Price-to-Earnings (P/E) ratio as a measure of valuation

Investors often look at a valuation in its most traditional form, also known as the P/E multiple. A P/E multiple (price to earnings ratio) gives investors an indication of what the market is willing to pay for every R1 of earnings generated. Setting aside the impact of short-term changes to profit, a high P/E ratio typically indicates the expectation and/or perception that a company could/would have good growth prospects, or less risk to profits, than the average company. Thus, a company with a proven long-term track record of growing profits would normally trade at a high P/E ratio and a company with low growth, or a patchy profit history, would trade at a lower P/E ratio.

While P/E is an incredibly good starting point to assess the valuation of a company or a market, many investors fail to look deeper.

Delving deeper into markets

The P/E ratio of the S&P 500 is trading at near-record highs. One could argue that it is, perhaps, a very blunt way to look at the world. It is important to unpack what drove the performance of the S&P 500 to these levels.

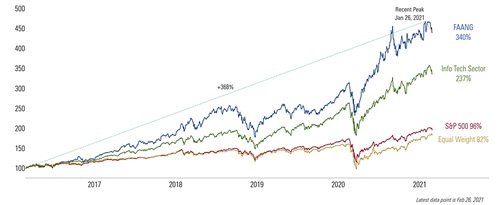

When analyzing the data depicted in the below two graphs, it is clear that most of the performance of the S&P 500 came from large FAANG stocks. [FAANG is an acronym referring to the stocks of the five most popular and best-performing American technology companies: Facebook, Amazon, Apple, Netflix and Alphabet (formerly known as Google)].

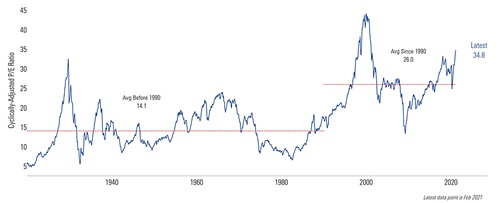

Exhibit 1 depicts the cyclically adjusted P/E ratio for the US market.

Exhibit 1 | The Shiller P/E Ratio – Valuation Using Ten Years of Inflation Adjusted Earnings

Source: Clearonomics, Robert Shiller. Data as at February 2021. Past performance is not an indication of future performance.

Exhibit 2 differentiates between the performance of FAANG stocks, other technology stocks and the S&P 500 as a whole, over the last couple of years.

Exhibit 2 | FAANG Stock Performance – Facebook, Amazon, Apple, Netflix and Alphabet (Google)

Source: Clearonomics, Standard & Poor’s, Refinitiv. Data as at February 2021. Past performance is not an indication of future performance.

There is no doubt that most of the large tech giants are good companies, with robust business models and incredible management teams. However, one must keep in mind the two tailwinds that existed – the first being record low interest rates for a prolonged period of time and the second being that most of these FAANG stocks were direct beneficiaries of lockdowns worldwide. Therefore, caution should be applied when assessing if they will continue to generate such exceptional performance indefinitely.

Looking at the opposite side of the coin - what about the other sectors that have not enjoyed such lucrative returns over the last number of years? Could the grass be greener on the other side but investors are not seeing it?

Is local still lekker?

On the local front, investors have enjoyed good returns from the JSE All Share index over the last few months. The question remains - will this continue or are we due for a correction? The truth is that nobody knows how long a rally can and/or will continue.

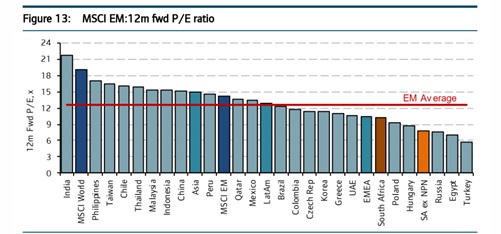

What we do know is that emerging markets have been severely out of favour for the last decade or so. Within the emerging markets group, South Africa has been out of favour for such an extended period that both local and foreign investors seem to have lost hope.

Exhibit 3 | MSCI Emerging Markets 12-month forward P/E Ratio

Source: MSCI, FactSet, SBG Securities analysis. Data as at January 2021. Past performance is not an indication of future performance.

The recent rally could be the market playing catch up coupled with a positive global backdrop for South African equities. The domestic economy may well continue to face structural headwinds going forward but could also recover from depressed levels gradually as activity normalises and accommodative interest rates stimulate incremental demand.

While we contemplate whether this partial recovery will be enough to generate satisfactory returns from domestic shares (from current price levels), there is the possibility for a more pronounced and sustained recovery in activity and sentiment as the global economy reflates and South Africa receives a natural slice of emerging market flows.

At Morningstar, we believe some areas in the domestic market still offer a very good opportunity and has lagged in the recent recovery. Financials are a good example of such an area.

What is the alternative?

A few years ago, South African investors could generate a real return (a return over and above inflation) of about 3%, by simply remaining in cash. It was an easy choice for those that did not want to expose themselves to equity market risk. Today, this picture is quite different. Cash rates are at historic lows with returns from money market funds sitting at about 4% and there is not much yield either if you look at developed markets.

Long dated South African Government bonds on the other hand still offer very attractive yields and continue to make up an overweight percentage within the Morningstar Portfolios. As far as equity risk is concerned, we continue to assess all individual opportunities through a valuation lens as well as the fundamental risk associated with each asset class. We continue to find value in areas of the market like UK Equities, European Equities, S.A. Financials, Energy etc.

Getting back to the question, are markets in a bubble at the moment?

At Morningstar, we believe a blunt expression like this one is probably foolish. The truth is there is always a bubble somewhere, whether it is Tesla, Bitcoin or the FAANGs. The best you can do is to continue to assess opportunities as they arise and patiently allocate money to the areas that will best serve your investment goals.

Although the obvious opportunity set has declined in equity markets over the last couple of months, there is still ample opportunity for investors who are willing to look a little deeper.