Brighter times, hard questions

Things have been going very well lately. Investment returns over the past year have been fantastic, certainly better than anyone could’ve hoped for given the Covid-19 pandemic. And the global economic growth outlook for the next year or so is bright. But instead of sitting back complacently, ask tough questions on what could go wrong.

Viral load?

The coronavirus is the best place to start. There has been good news and bad news. The global vaccination rollout continues, though unevenly. Pfizer’s jab has been approved for vaccinating teenagers for the first time, broadening the fightback against the virus. In the US and much of Europe, the worst of the third wave is over, and reopening is underway. On the other hand, the crisis in India is still severe, and naturally the fear is that a nasty new variant could still cause havoc elsewhere.

Closer to home, there has been a noticeable increase in new confirmed Covid-19 cases over the past few days, after a long period of stability. Scientific opinion seems divided on how bad this wave will get. South Africa continues to lag in terms of vaccinations, but estimates of prior infection are as high as 50%, which could limit the severity of further outbreaks. Either way, a return to the harsh lockdown of a year ago seems highly unlikely.

The economic impact of a third wave in South Africa is therefore likely to be much smaller than that of the previous two waves. Meanwhile, the big drivers of economic recovery, such as commodity prices and lower interest rates, remain in place.

The great global inflation?

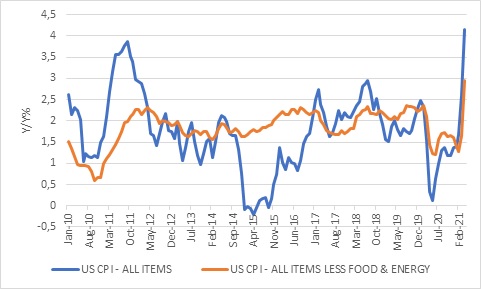

Global markets suffered a serious wobble last week after the US consumer price index rose much more than expected in April. Headline consumer inflation hit 4.2% year-on-year, the highest since 2008. Fears of sustained higher inflation across the world had already been brewing for some time, due to a combination of a lower starting point because of lockdowns last year (known as a base effect, which is just a statistical illusion), and the more tangible impact of global shortages and bottlenecks.

Chart 1: US consumer inflation, year-on-year %

Source: Refinitiv Datastream

Prices are set by the interaction of demand and supply, so when demand for a specific item increases faster than supply, the price rises. A year ago demand for toilet paper suddenly increased as people began stockpiling. Factories couldn’t immediately increase output, so prices had to rise. But supply eventually responded, and today toilet paper is neither scarce nor expensive.

At the moment there is a particularly acute shortage of computer chips, which is holding back production of new cars at a time when demand has increased. As a result, used car prices are also increasing rapidly, and this was one of the big contributors to the blockbuster April CPI number in the US. Also pushing up used car prices is the fact that car rental companies had fewer vehicles to sell into the used market, since fleet upgrades were kept to a minimum last year.

In contrast, a company like Netflix could effortlessly and immediately respond to increased demand for its services, and this is one of the reasons why investors love these technology platform businesses. At the other extreme is copper (and other raw materials). Demand for copper is increasing due to higher economic growth rates, as well as the shift towards electric vehicles and other green technologies. Copper output has barely budged, and indeed it may take several years before any sizable new mines open. Prices have shot up to reflect this.

Will this result in sustained consumer inflation? Remember that this will require prices to rise across a broad range of goods and services at the same pace year after year. Companies have every incentive to respond to supply chain bottlenecks, and it seems unlikely that these shortages will persist for years and years. A big once-off jump is not the same as inflation.

It’s easy to understand why inflation is bad for consumers, but why does the market care? Simply put, because it results in higher interest rates. At some point, central banks will respond with increases in short-term interest rates, and long-term interest rates set by the market will anticipate this well in advance. Higher rates can also slow economic growth, denting expectations for future earnings growth. For bonds, this implies capital losses, and the higher the duration of the bond, the bigger the loss. For equities, this usually means a de-rating: every future dollar of earnings becomes less valuable even if actual earnings growth is still strong.

Equities too expensive?

Global equities are particularly exposed to a surprise increase in sustained inflation since it appears that is not priced in, certainly not for the big technology companies that trade on very elevated multiples. The first two months of the year provided something of a dress-rehearsal when long-term interest rates rose sharply and the “growth” sectors of the market sold off. Growth companies are called that because they can generate their own growth, while cyclical companies require a strong economy to perform well. It is these cyclical companies that have outperformed this year as the global economy has heated up.

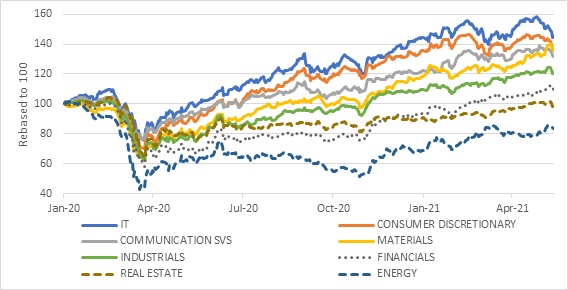

The chart below shows the main global equity sectors from the eve of the pandemic. Clearly, the performance diverged strongly, with the pandemic winners concentrated in the IT, communication services, and consumer discretionary sectors. The losers were mostly in energy, real estate and financials. This divergence also plays out in the valuations of these sectors. As global growth has heated up this year, and long-term interest rates increased, the relative performance has reversed somewhat.

Chart 2: Global equity sectors (MSCI All Country World Index $)

Source: Refinitiv Datastream

While a nasty inflation surprise might cause indiscriminate selling on global equity markets, the stronger underlying economic growth that gives rise to higher inflation should benefit these cyclical companies that are already much cheaper.

So there are still areas of value within global equities – it is a vast asset class after all, comprising thousands of companies across all imaginable regions and sectors. And of course, one of the corners of the global market that is still attractively priced by most metrics despite a recent run is South African equity.

Financial stability risks?

Related to the risk of sustained higher inflation is the risk that financial vulnerabilities accumulate while central bank policy remains extremely loose. Simply put, there is too much borrowing and too much speculative activity. When rates do eventually rise, the piper has to be paid.

The International Monetary Fund’s Financial Stability Report recently noted that unprecedented policy support could have unintended consequences, namely “excessive risk taking in markets is contributing to stretched valuations, and rising financial vulnerabilities”.

Global debt levels have indeed increased meaningfully. Many companies are making use of ultra-low interest rates to build cash positions or make acquisitions. This has been mild compared to the increase in government debt in response to the pandemic. In the US and to a lesser extent, the European Union, spending has arguably gone beyond what was needed in direct reaction to the pandemic, focusing on longer-term structural transformation as a part of a “build back better” agenda.

As long as interest remains low and markets liquid, and while economic growth is decent, debt levels are not a problem. While much of the focus is on government debt-to-GDP ratios, for instance, debt service ratios are more useful indicators, particularly for countries that borrow in their own currencies. Historically, big culprits causing financial crises are excessively borrowing in foreign currency, where servicing the debt depends on somehow earning enough of that currency, and being at risk of adverse exchange rate movements. And to make things worse, the central bank responsible for the currency you borrow in sets interest rates with no regard for your domestic economic conditions. Interest rates could rise just when your economy needs lower rates, for instance.

The other big culprit is usually runaway residential property markets, fuelled by households borrowing beyond their means. When property booms go bust, households sit with elevated debt levels even as the value of their assets declines. This can impair confidence levels for several years, and even low interest rates cannot induce more spending. At the same time, banks end up with bad debt on their books, limiting their appetite to lend. The economic damage from a burst property bubble can be deep and prolonged. In contrast, when equity markets fall (bubble or not), the broader economic impact is often limited to shareholders being poorer on paper.

Therefore, the substantial increase in housing market activity in many countries since the pandemic struck is of interest. This has been fuelled by lower interest rates and a greater need for space to work and live. In some cases, such as Australia, Canada and Sweden, household debt levels were already high going into the pandemic, and further increases are worrying. However, a house price correction in Australia is not going to crash the global economy. Only the US and China can do that.

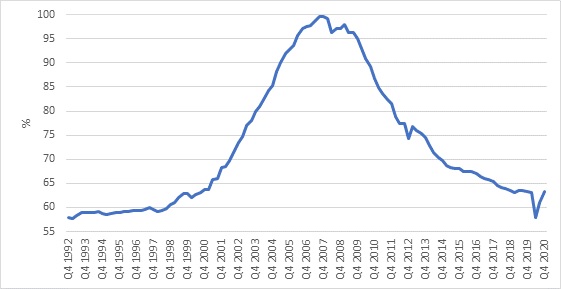

The $10 trillion US mortgage market is by far the largest in the world. The memory of the housing bubble that led to the 2008 Global Financial Crisis remains fresh and the current boom is causing some concern. The nationwide Case-Shiller house price index declined 30% from its 2006 peak and only recovered in 2017. In the year to February, it increased 12%. Crucially though, despite a recent increase in mortgage origination, overall outstanding mortgage debt only returned to 2006 levels a few months ago. But incomes have grown substantially since then, and interest rates have fallen, so the burden of servicing this debt is much lower.

There is also no sign yet of a return to the kind of reckless loans made during the previous boom when lenders happily issued mortgages to people who had no hope of making interest payments over the long term. In other words, the risk of the US housing market destabilising global financial markets is still small, but will need to be watched. The risk that the Fed raises interest rates in response to a bubbly housing market – to avoid the mistake they made the last time – is also still small but could grow over time.

Chart 3: US outstanding mortgages as % of household disposable income

Source: Refinitiv Datastream

In China, the long-running housing boom has played a big role in the country’s rapid economic growth and its voracious commodity demand. Land sales to property developers have also long been a big revenue source. The Chinese household savings rate is high, but recent years have seen a definite speculative activity and rising debt levels. Corporate debt levels have also increased sharply, supported by a widespread idea that the state will bail out struggling borrowers. Chinese regulators are deeply aware of the risks this poses to the banking sector and the broader economy. Authorities’ emphasis is likely to shift away from growth to addressing these risks.

But it is a tricky balance, since growth is what makes debt sustainable. If income growth is higher than prevailing interest rates, debt can be serviced and paid down. So far that is the case. The problem is often that a long period of rapid growth encourages borrowing, and when economic growth eventually slows, it is a double whammy.

South Africa’s dependence on China has increased in recent years. A financial crisis in China will hit South Africa directly – commodity exports and the fact that the biggest shares on the JSE are directly exposed (Naspers, Richemont, BHP, Anglo American) and indirectly through the knock to global investor sentiment and global economic activity.

In summary

Despite the massive global shock of the pandemic, risk assets recovered quickly and have performed very well over a 15-month period that includes the crash and the rebound. This can lead to a sense that equities only ever go up while central banks will always be there to bail out markets and the best thing to do is just to own a concentrated portfolio of, say, tech shares.

But these hard questions show that there are many risks out there, inevitably leading to the conclusion that one should take different scenarios into account and that a diversified portfolio is necessary. It is not about making forecasts. It’s simply about thinking of the many things that could go wrong or right, and constructing a balanced portfolio that can still deliver real returns in a variety of different outcomes.