Bonds behaving badly

As the three-month mark of the Gulf War approaches, a barrel of oil is still close to triple digits and the pressure on the global economy continues to build. Business profit margins are squeezed, and household real incomes are slipping.

Reported inflation is already higher due to the direct weight of fuel prices in consumer price indices. Companies will pass on some of their cost increases to consumers, making a broadening of inflation pressures likely in the months ahead. However, that will largely depend on how long energy prices remain high.

Equity markets have largely ignored these concerns, focusing instead on strong earnings growth and enthusiasm around the artificial intelligence (AI) capex boom and anticipated blockbuster listings of SpaceX, Anthropic and OpenAI.

Downbeat bonds

Bond markets, in contrast, have been much more worried. In one sense, this is to be expected. Bond investors are always a bit nervous. Their preoccupation tends to be to preserve money, whether in nominal or real (after-inflation) terms. Equity investors have more of a blue-sky view of the world, focusing on potential upside. Stereotypically, they fear missing out more than almost anything else. And the AI rally seems to be FOMO on steroids.

The prices of government bonds have slumped since the start of the war, pushing up yields. The proximate cause is the inflationary impact of higher oil prices. In many developed countries, inflation had only just returned to target after the 2021/22 surge. In the case of the US, inflation was still in the process of hitting the Federal Reserve’s 2% target. The last time the Fed’s preferred inflation measure was close to target was March 2021, and it is once again moving in the wrong direction.

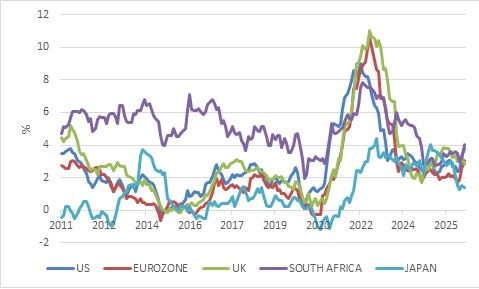

Chart 1: Headline consumer inflation rates in selected countries

Source: LSEG Datastream

Bond valuations are particularly allergic to unexpected inflation, since it erodes the fixed income bonds provide. The unexpected bit is key, because markets adjust quickly to what is expected and the war upended the narrative of gentle global disinflation in force at the start of the year. There is a category of bonds whose values are protected against inflation, but these inflation-linked bonds are a small slice of the overall pie. Most bonds issued by governments leave investors at the mercy of shifts in the inflation outlook. That wasn’t always a problem, since inflation across the developed world tended to be well behaved over the past few decades. Not anymore, it seems, with the post-Covid global surge in inflation potentially signalling a regime shift.

Inflation’s negative impact on bond valuations is compounded if central banks hike interest rates. Higher short-term interest rates offer competition to longer-term bond yields and money can flow from bond markets into cash.

It is at times like these when central bank credibility is important. If investors sense that central banks are willing to tolerate higher inflation than in the past, they will want higher bond yields to compensate for this risk. It is notable, for instance, that in the emerging markets where central banks have adopted inflation targeting and shown a willingness to tackle inflation, bond markets have been more stable. In the past, a similar risk-off event would have seen an indiscriminate sell-off of bonds and currencies of emerging markets, including South Africa (more on that below).

Nonetheless, central banks have different sensitivities to the oil price. Expectations for European Central Bank rate hikes jumped as soon as the bombs started falling. However, until very recently, the US Federal Reserve, the world’s most important central bank, was still expected to cut rates. No longer.

Minutes from its April policy meeting, released with the customary three-week lag, showed officials growing more concerned about inflation. A “majority” indicated they could support “some policy firming” if inflation remains above the 2% target, though “most” participants continued to see downside risks to the labour market. While Fed rate hikes are still unlikely, so are rate cuts. Incoming Chairman Kevin Warsh is widely believed to be dovish (i.e. in favour of lower rates and less concerned with inflation) but he will have a hard time convincing his colleagues that rate cuts are appropriate when inflation is rising, even temporarily, and the latest labour market date points to some stabilisation.

Click here to read more...