Bond yields plunge as Brexit vote draws near

Dave Mohr, Old Mutual Multi-Manager.

Izak Odendaal, Old Mutual Multi-Manager.

Global risk appetite took a sharp negative turn over the past few days, partly as a result of an increased risk that the UK could exit the European Union (EU).

Polls show shift in support

Several polls conducted over the past week showed a shift in support towards leaving the European Union, but the outcome is unclear given the large number of undecided voters (the latest polls released over the weekend appear to have swung back to favour the Remain camp). We eagerly await what’s to come on Thursday. If there is a Brexit, it could have negative long-term consequences for the UK. However, it is unlikely to be a shock to global financial markets (although the pound sterling is likely to fall, which should benefit some sectors) as firstly, the UK has its own currency which would move but not disappear (unlike a Greece exit), and secondly the UK has its own central bank to provide ample liquidity. Lastly, the process of uncoupling from the EU is likely to be a protracted negotiated affair. But markets also don’t like uncertainty. The spread of bond yields of peripheral European economies (especially Portugal and Greece) over German equivalents widened. After all, if the UK leaves the EU and thrives, voters in these countries might get similar ideas.

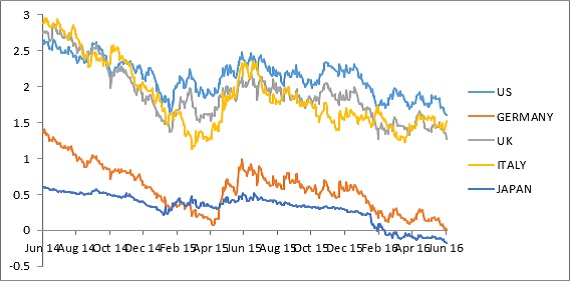

Yields collapse

While global equity markets retreated, and peripheral bonds sold off, bond yields of the most important economies plummeted. The German 10-year Government bond yield fell below 0% for the first time in history. That said, many of the world’s fixed income assets trade at unprecedented negative yields. After all, investors who hold for a negative-yielding bond to maturity are guaranteed a loss. The only rational reason to buy such a bond would be the expectation that it could be sold at a profit before it matures (as yields fall prices increase) or if you were forced by regulation to do so (e.g. banks or insurance companies). With the European Central Bank (ECB) also actively buying, such forced purchasers in the Eurozone are finding bonds scarce, especially with Germany running a budget surplus and therefore issuing very little new debt. The third circumstance would be if investors expect deflation, in other words that returns would be positive in real terms because of falling prices. It would be a ghastly scenario to have falling prices over 10 years, the ECB and the Bank of Japan are fighting tooth and nail to prevent this. Yet inflation expectations on both sides of the Atlantic have fallen in recent weeks, despite a higher oil price – now trading around US$50 per barrel – which should lift expected future inflation.

US rates on hold

Against this backdrop, the US central banks, the Federal Reserve (Fed) opted to leave rates unchanged despite its own stated intention to steadily raise interest rates. Over the past two years it had to hold back on hiking on several occasions when faced with an unexpected weakening of the US economy, falling inflation or financial market volatility (in the US and abroad).

Notably, the Fed’s rate-setting committee cut its projections for future interest rate increases despite its forecasts for future growth, unemployment and inflation. The Fed appears to be coming round to the argument that the “neutral” interest rate – the rate consistent with stable inflation – is structurally lower, and not just temporarily depressed due to the global financial crisis.

South Africa’s current account deficit wider than expected

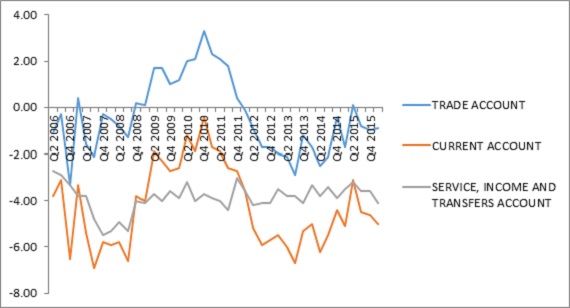

Apart from the increased global risk aversion, local markets were rattled when the South African Reserve Bank announced that the current account deficit was larger than expected in the first quarter. This was largely due to a sharp decline in dividend receipts from abroad. The trade deficit was slightly smaller in the first quarter compared to the fourth, due to an increase in the value manufactured exports while commodity exports remained more or less the same. The value of imports also increased, but by less.

Therefore, while the trade deficit narrowed to 1% of Gross Domestic Product (GDP), the deficit on the services and income account widened from 3.6% of GDP in the fourth quarter to 4.1% in the first quarter. Dividend outflows increased during the quarter, while dividend outflows fell for the fifth consecutive quarter.

Disappearing foreign dividends

In other words, despite the fact that the rand weakened by 30% against the US dollar over the past year and South African companies spent R77 billion on acquisitions abroad over the year to end-March, dividend inflows halved over the period. Part of this might be related to investments in Africa, where a lack of foreign exchange in Angola and Nigeria has “trapped” dividends, but it might also be that companies are choosing to leave their profits in the countries they are operating in. This is hardly a vote of confidence in a South African economy plagued by very low levels of business sentiment. Private sector fixed investment fell at an annualised rate of almost 7% in the first quarter.

If there is some good news hidden in the current account numbers, it was the 9% increase in travel receipts as tourism flows continue to improve. However, the large current account deficit means we are still dependent on foreign portfolio inflows, or what the Bank of England’s Governor Mark Carney called the “kindness of strangers”. The UK, with its 7% GDP current account deficit seems mad to flirt with the inherent uncertainty of Brexit at a time when global financial flows are particularly fickle; South Africa even more so, needs to stick to sound policies to lift confidence in the economy and get growth going again.

Chart 1: Developed market 10-year government bond yields

Source: Datastream

Chart 2: South Africa current account balances, % of GDP

Source: SA Reserve Bank