Avoiding risk a risky move for investors

Paul Bosman, fund manager at PSG Asset Management.

SA investors have experienced more than their fair share of volatility over the last few years. It’s been a rough, tough ride in the market and even dedicated long-term investors have found themselves looking for ‘safer bets’ until things settle down.

Paul Bosman, a fund manager at PSG Asset Management, urges investors to resist the urge to hide in cash in an attempt to avoid drawdowns in a volatile market.

“Cash may feel ‘safer’ for now, but research shows that in the long term, not taking on enough risk is likely to leave you significantly worse off,” says Bosman.

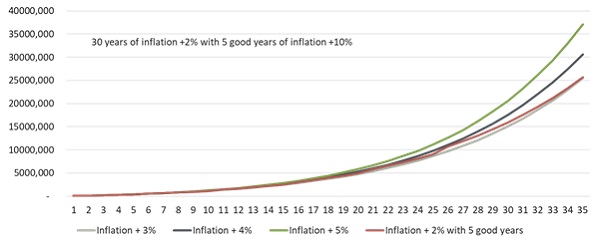

Consider an investor putting aside R5 000 per month (adjusted for inflation) for his retirement over a 35-year horizon. He takes a conservative approach, with a cash portfolio that generates inflation +2% a year. Every now and then, he takes on a bit more risk when he feels the market is going to run. Let’s assume that he does this with great success and generates inflation + 10% in five of the 35 years for which he is invested. He would still be left with a portfolio that generates an average of inflation +3% per annum over the period.

Compared to inflation +5% per annum (a typical balanced fund mandate), the conservative investor would have underperformed by 2% a year. While this may sound innocuous to some, the cumulative result would have been a 31% reduction in his retirement savings: R25.5 million instead of R37 million (future value terms).

Source: PSG Asset Management

“It is one of the great ironies of investing that ‘playing it safe’ is not really safe at all over the long term,” says Bosman. To make matters worse, the average investor will only start to see this the closer they get to retirement – when they have less time to recoup losses.

On the other hand, when investing in equities, you may feel like you’re on the losing end many times over a 35-year period. It takes a strong resolve to stay committed, but it’s critical. “Research shows that investors are unlikely to generate returns of inflation +5% after fees over the long term without significant equity exposure,” says Bosman. Counterintuitively, this makes equities a safer long-term bet than cash.

Balanced funds are excellent vehicles for long-term savings

Balanced funds have become a popular choice for investors saving towards retirement. They invest sufficiently in equities to avoid the low-risk, low-return trap but are also required to have at least 25% invested in other asset classes to moderate risk.

“The last two years have been tough for investors in South African balanced funds, but the important thing to remember is that their performance needs to be evaluated over the long term, and not from year to year,” says Bosman.

The average balanced fund in the South African multi-asset high-equity sub-category has returned about 13% a year since inception of the category in February 1994.

“This means that, over the long term, every R1 000 put into a balanced fund has doubled about every six years,” says Bosman. “Even if you take a more conservative return of 10% a year, your initial investment doubles every seven years.”

The PSG Balanced Fund has returned 14.1% per year since its inception in June 1999, outperforming its benchmark of CPI +5%.