Avoiding fiscal fireworks

Most people cannot imagine anything more boring than fiscal policy. They are not necessarily misguided. It is usually good when fiscal policy is boring, calm and predictable. Fortunately, that is increasingly the case in South Africa, but not so much elsewhere.

The South African Medium Term Budget Policy Statement (MTBPS), also known as the mini-Budget, updates the numbers presented in the annual February Budget Speech. Budget projections are done on a three-year forward basis, allowing for transparency. There are problems in the South African fiscal landscape, but at least we know about them. Though government debt levels have increased rapidly since 2009, debt itself is not necessarily the biggest problem.

Chart 1: SA nominal GDP growth and 10-year government bond yield, %

Source: LSEG Datastream

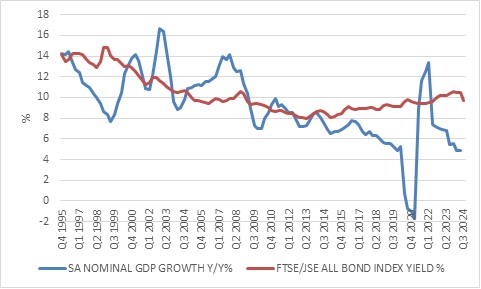

Rather, it is the disastrous combination of low economic growth and high interest rates. Put simply, the government is borrowing at around 10%, but since growth in tax revenues correlates with nominal economic growth, its income has only been growing around 6%. As chart 1 shows, this gap started widening about a decade ago; before then, the nominal economic growth rate was higher than the government’s borrowing costs and debt levels were sustainable. But as growth slowed, the market was increasingly concerned about South Africa’s fiscal sustainability, pushing up bond yields. Higher borrowing costs in turn put downward pressure on economic activity. This was a vicious cycle that we are hopefully in the early stages of reversing. Bond yields have declined since the election, and growth prospects are higher. Nothing should be taken for granted, however.

The MTBPS somewhat disappointed markets by projecting a wider-than-expected deficit for the current year at 4.7% of gross domestic product (GDP). This is mainly due to tax revenues undershooting by R22 billion. Ironically, lower-than-projected tax revenues are partly due to the improvement in electricity supply. Eskom has been burning less diesel, lowering fuel tax revenues, while import VAT receipts were also lower as imports of solar panels and other electrical equipment have declined.

However, the commitment to fiscal consolidation remains. Treasury will still run a primary surplus this year and over the next few years, meaning tax revenues will exceed non-interest spending. This is projected to result in the debt-to-GDP ratio peaking in the next fiscal year (2025/26) at 75% and drifting lower thereafter.

Click here to read more...