Are we not sailing into the wind?

The more things change, the more they stay the same. For investors, with 2020 still fresh in their minds, this year has been yet another case in point.

With so much having changed this year, it is easy to believe we’ve entered a new paradigm.

But although much has changed, the future is no less certain than it was a year, or two, or even ten years ago.

Investing today is equally challenging, because we’re still looking to make portfolio decisions in highly uncertain times.

We still need to carefully review the opportunity set, try to put emotions aside and take calculated risks.

The reward then lies in waiting to see whether we realise a return better than risk-free. This sounds simple, but it is far from easy.

For most investors, it’s challenging to set aside emotions and avoid the tendency to extrapolate an often-biased view of today’s reality into the future. Motivated by instant gratification, many investors struggle to see beyond the short term. However, it’s important to note that investing is a long-term pursuit.

But if investing is for the long term, and given that the further out we look the greater the uncertainty, are there any guideposts to lead us on the journey? Fortunately, there are. Investing successfully is like the task of a seasoned sailor navigating uncharted waters.

Knowing where true north lies is a useful start, and when it comes to investing, true north is having a sense of valuations. But that’s not all. Just like the sailor should also know how to harness, or else risk being buffeted by the wind, investors need to be aware of the prevailing cyclical economic factors driving asset prices.

It goes without saying that it is easier to steer across calm rather than choppy waters, and the same applies in investing. And market conditions this year have been anything but calm. However, it is in these less-than-ideal conditions that seasoned investors are generally able to separate themselves from the crowd.

Where is true north today? It appears the strongest “pull” in valuation terms exists outside of the US. Even though US stocks have been derated, there is still better value to be found elsewhere. South African assets, for example, are very attractively valued, with the SA equity market currently as cheap as it was during the 2008 Global Financial Crisis.

South African government bonds are also attractively valued, having become cheaper despite the creditworthiness of the South African government having improved. Unlike SA equity and bonds, most other major asset classes are either fairly valued or somewhat expensive.

For an investor looking for true north, we believe that lies somewhere in the region of being overweight South African equity and bonds in a multi-asset portfolio. Be that as it may, the obvious question to ask is “Are we not sailing into the wind?”, with economic headwinds and signs of an oncoming recession in major economies.

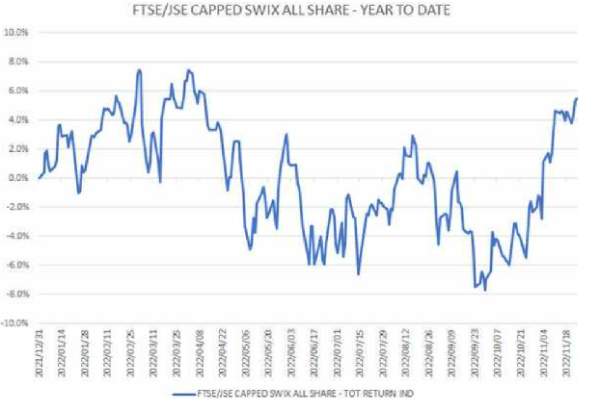

Perhaps, but it is worth pointing out that we’ve already been facing stiff headwinds all year long. Headwinds such as the Russian-Ukraine war, Europe’s cost-of-living crisis, record high developed-market inflation, the most aggressive US Fed tightening cycle ever, and China, the world’s former growth engine, having stalled. Yet, at the time of writing, the South African equity (and bond) market is up for the year to date.

Source: Refinitiv Datastream, January 1 – November 25, 2022

This goes to show that economic headwinds don’t necessarily mean all asset prices will be dragged off course. Just like the seasoned sailor might still be able to zig-zag windward and advance relative to true north, the trick is avoiding the major obstacles on the horizon and staying the course.

Indeed, we are still sailing into the wind. The global economy is decelerating, and central banks continue to tighten policy to combat concerns that high inflation may become entrenched. Investors might also worry that higher interest rates, after a long period of ultra-loose policy, could well expose vulnerable and debt-laden markets to unforeseen shocks.

Now is not the time to be making bold calls, but it is also not the environment to shy away from risk completely. While there are some astute investors who are exceedingly adept at actively dialling portfolio risk up and down at the right time, this is not true for most investors. The best bet for most is not to veer too far from their longer-term ideal asset allocation in their multi-asset portfolios until the wind subsides.