Are We Nearly There?

Any adult who has embarked on a journey with a young child is undoubtedly well-acquainted with the infamous question, “Are we nearly there?” During a recent road trip, my five-year-old posed this question no less than ten times - the initial query occurring just a few minutes into our two-and-a-half-hour drive.

Reflecting on the multiple recession predictions made by economists at the start of 2022, 2023, and now 2024 (all of which have yet to materialise), one can draw parallels with the experience of children on a long journey. In essence, both groups grapple with the challenge of accurately gauging their proximity to the “destination”. In economic terms, our position within the current business cycle remains unclear, leaving many to regularly ponder the question: Are we nearly there?

UNPACKING THE BUSINESS CYCLE

The business cycle is regarded as one of the most accurate frameworks depicting how economies fluctuate every few years. Given its theoretical soundness, it is often used by investors for both asset and sector allocation decisions. For investors, understanding the current phase of the economic cycle can provide valuable insights into which sectors of the equity market should be considered for exposure. The table below summarises the four key stages of the business cycle. While the validity of the framework is broadly accepted, ongoing debates often arise regarding the precise stage at which an economy currently resides. This challenge becomes especially pronounced when economic data presents mixed signals, as is currently the case.

THE BUSINESS CYCLE STAGES & ASSOCIATED SECTORAL PERFORMANCE

CONFLICTING SIGNALS

The US is a prime example of an economy currently contending with a confluence of mixed economic signals. Despite the US Federal Reserve (Fed) emphasising a data-dependent approach to future interest rate decisions, Morningstar Research highlights that bond market volatility in 2023 surpassed any period over the last decade. This trend has persisted into 2024 as investors attempt to interpret conflicting economic data that will ultimately determine the Fed’s next interest rate move.

The latest major US data that surprised market participants were the unemployment numbers. Rather than indicating a slowdown in hiring (typically associated with a late-cycle economy), the data revealed an acceleration in both hiring and hourly earnings. This suggests a healthy and robust economy that is some distance away from any slowdown. The US GDP numbers reported in January conveyed a similar story, showing a faster growth rate (3.3%) in the fourth quarter of 2023 compared to earlier in the year, resulting in above trend growth for the US economy last year.

However, conflicting signals have emerged from indicators tracking corporate profits, inventories, consumer credit and US vehicle sales over the last few months. These somewhat contradict the strong GDP and employment numbers, suggesting that the US economy may in fact be in the later stages of the current cycle.

On the local front, while the SA economy broadly follows the same cyclical framework, there are notable nuances. Particularly impactful have been factors that have constrained economic growth over the last decade, such as load shedding and other infrastructure bottlenecks. The resultant impact on confidence has meant that even during periods of expansionary fiscal and monetary policies (such as those experienced post the COVID-19 pandemic), the proverbial “animal spirits” that typically accompany post-recession phases of the economic cycle have not materialised. With both business and consumer sentiment yet to show any signs of material improvement, forecasters are expecting another year of below-trend growth and no cyclical recovery for the local economy.

HOW OUR PORTFOLIOS ARE POSITIONED

While mindful of the current economic environment, our approach at the start of every year is not to attempt to forecast economic developments and then position our portfolios for that outcome. Instead, our investment process involves constructing well-balanced, diverse portfolios that consist of high-quality businesses capable of weathering various economic conditions. This bottom-up (or company-specific) approach is then supplemented with a top-down (or macroeconomic) perspective to ensure that we are not overly exposed to any singular risk.

Investing in quality businesses is inherently tied to the careful selection of companies led by exceptional management teams. Our experience has shown that great management teams are adept at steering companies through varying economic cycles, which often negates any benefit of trying to predict economic outcomes and timing the ownership of such businesses.

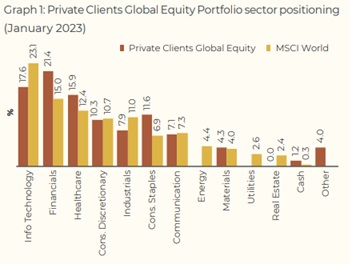

Graph 1 shows our Global Equity Portfolio’s sector exposure relative to the MSC World Index at the beginning of the year. At first glance, it appears as though our largest deviation from the overall market is within the IT (underweight by 5.5%) and financial (overweight by 6.4%) sectors. However, it is important to note that Visa, one of our largest holdings, was recently shifted out of the IT sector into the financial sector. Furthermore, Berkshire Hathaway, classified as a financial company, is a highly diversified business with operations spanning multiple industries. These nuances underscore an additional rationale behind our process of not merely mirroring the index. Instead, we focus on the underlying holdings in the portfolio and the specific exposure each holding provides.

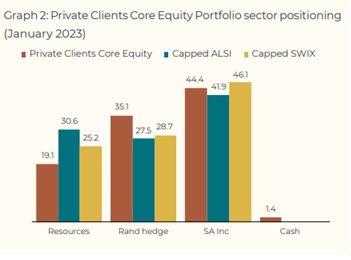

Locally, in addition to traditional sector positioning, we further categorise our holdings across three broad categories - resources, rand hedges and SA-exposed businesses. Graph 2 shows our Core Equity Portfolio’s positioning relative to the Capped All Share Index and Shareholder Weighted Index. Mirroring our global process, we do not have a target sector exposure based on economic forecasts. Instead, we focus on the underlying holdings within the portfolio, with the sector positioning emerging as a result of the process rather than being the primary objective.

Similarly, when building our multi-asset class portfolios, our emphasis lies on security selection within each asset class, steering clear of extreme positions driven by specific economic predictions. This approach is designed to create well-balanced portfolios capable of performing effectively in diverse market and economic conditions.