Another pivotal budget

Almost every Budget Speech of the past decade has been called “pivotal”, “make or break” or something similar. And yet the great pivot never seems to arrive. Except for the brief post-Covid commodity boom, a decisive change in the country’s fiscal dynamics has yet to materialise.

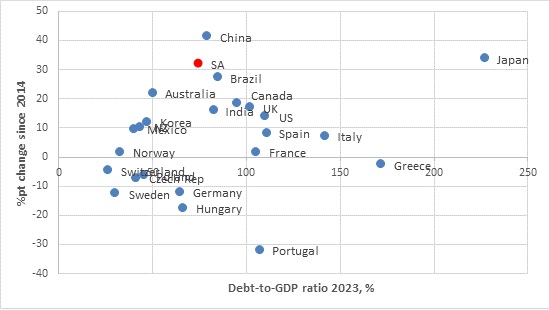

Instead, government debt levels have increased sharply. Year after year, the Budget has projected a stabilisation of the debt-to-GDP ratio, and yet it still rises. It is not high by international standards, as chart one shows, but stands out for how quickly it has increased in the last decade.

Chart 1: Government debt-to-GDP ratios

Source: Bank for International Settlements

That is not because National Treasury lacks intent. Rather, it does not control all the levers of government finances, and external circumstances have not been helpful, particularly when Covid hit.

Importantly, National Treasury does not set wage increases for public servants. It is another government department that leads the negotiations with public sector unions, and ultimately it is a political, not technocratic decision that determines the outcome. Successive rounds of wage agreements have been higher than what was pencilled in by Treasury, though there was some claw-back when wages were frozen during the pandemic, breaking the steady upward trend. The other problem has been the ongoing need to provide financial support to struggling state-owned Enterprises that are not viable on their own anymore. Eskom and Transnet bailouts were necessary due to their critical role in the South African economy (further support for Transnet could be announced this week). However, support for other entities like SAA and the Post Office are arguably overtly political, since they could easily be replaced by private companies. The introduction of free tertiary education for low-income students in 2017 was also an unbudgeted political decision imposed on Treasury.

The Big Problem

But the biggest problem Treasury had to contend with is simply that the economy has underperformed expectations from 2014 onwards. Weaker-than-expected growth means lower- than-expected tax revenues – not helped by the hollowing out of SARS’ capacity during the Tom Moyane years (now thankfully largely reversed).

The current fiscal year (2023/24) has not been different. Although economic growth in 2023 has largely been as expected (the February 2023 Budget Speech forecast 0.8% growth), corporate tax revenues have disappointed. This is partly because of the big decline in commodity prices, particularly coal, from 2022 but also as 2023 was the worst year for loadshedding on record. Companies had to spend billions on running generators and investing in solar and other alternative forms, denting their profitability.

Meanwhile, spending has been running somewhat ahead of projections. This means the budget deficit – the difference between spending and tax revenue that must then be made up by borrowing – will be larger than anticipated in the 2023 Medium-Term Budget Policy Statement (MTBPS). Expressed as a percentage of GDP, the deficit could be greater than 5%, compared to the 4.9% shown in the MTBPS.

This is politely termed ‘fiscal slippage’ by economists. While the finance minister will reiterate plans to reduce the deficit over the next three years, the larger new starting point means that it will take longer to stabilise the debt ratio, with a higher peak than the 77% forecast in November.

Of interest

All this borrowing (more than R350 billion per year in new debt, and more than R100 billion in redemptions) takes place at very high interest rates. South African interest rates have always been relatively high because inflation has been rather high. However, in recent years we have seen real borrowing costs rise as the bond market demands yields to compensate for the perceived higher risk of lending to the South African government.

And this creates a vicious cycle.

As chart two shows, the government’s borrowing cost has exceeded the economy’s nominal growth rate over the past decade. This is not a complete coincidence, since weaker growth has caused higher yields due to concerns over fiscal sustainability. This is a reversal from the usual international pattern where lower growth drags yields down as inflation expectations decline. Today, however, the South African government borrows at 10% while national income only grows at 6%. Left unchecked, this is a recipe for trouble.

Click here to read more...