An Uncertain Birthday

Friday was the 249th anniversary of the US Declaration of Independence, signed on the 4th of July 1776 in Philadelphia.

Next year will see huge celebrations and 250 candles on the cake. These will not be enough to overcome the deep political divisions, however, and the focus will quickly turn to the midterm elections in November. Whether the strength of the US economy will still be cheered is a big question for investors around the world. If the US economy can maintain a degree of vigour, it can sustain the rally in US equities. However, it might also limit the scope for interest rate cuts, at least while Jerome Powell is holding the reins as Federal Reserve chair.

With big social and political changes underway, the longer-term direction of the world’s largest economy is also in question. The topic of the US dollar and its central role in the global system will be tackled in a separate upcoming note.

Less miserable

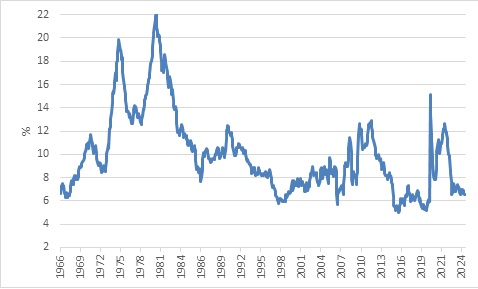

Let’s start with the near-term outlook. Despite his protestations to the contrary, Trump won the election with the US economy in decent shape, at least at the aggregate level, and certainly compared to other developed markets. One way of showing this is the so-called Misery Index, which simply adds together the unemployment and inflation rate. It jumped between 2020 and 2022 as a result of massive job losses and then due to the post-pandemic inflation surge. By late-2023, however, it was close to pre-pandemic levels.

Chart 1: US Misery Index

Source: LSEG Datastream

Inflation has been slow to return to the Federal Reserve’s 2% target, but has generally drifted lower, while the unemployment rate was 4.1% in June, near historic lows. The US economy added a healthy 147,000 jobs in June, more than expected by economists. However, most of the new jobs were in the public and healthcare sectors, and not in cyclical industries. While there is little indication of widespread job losses, there are signs that people who have lost jobs are struggling to find work again. This suggests some weakness underneath the surface.

Tariff trouble

There is an obvious headwind: President Trump’s tariffs. These are already clearly visible in customs data, with $23 billion collected in May, a significant jump from previously. What we don’t know is where exactly tariff rates will settle. A handful of countries, notably the UK, China and Vietnam, have reached trade agreements with the US, but for the rest we’ll find out this week when the 90-pause on reciprocal tariffs will expire. It is unlikely to be the end of the matter completely, and new threats and deadlines are likely to emerge from time to time. The uncertainty is not helpful, but the effective tariff US rate (the average across all categories and countries) will probably eventually end up somewhere between 10% and 15%, much higher than the 2.5% at the start of the year, but not quite as bad as feared in April.

Click here to read more...