An investor-friendly Budget against a favourable global backdrop

by Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

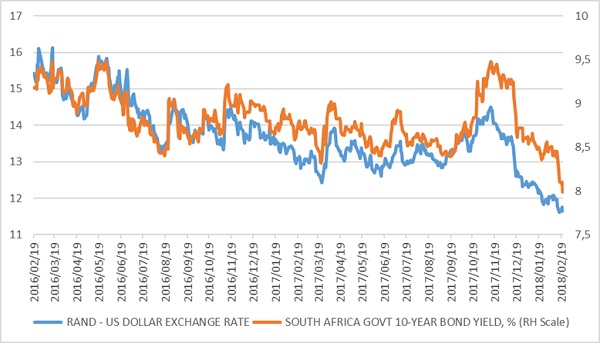

There were more jitters on global markets last week as investors tried to price in the pace of interest rate increases, but most indices ended the week in positive territory. Minutes from the Federal Reserve’s January monetary policy meeting – released with a three-week lag – show that the participants are currently comfortable with the US inflation outlook, but increasingly think US growth will surprise on the upside. The fear of many investors is that this would lead to interest rates rising faster than currently expected. The yield on the US 10-year Treasury, the global benchmark, has almost doubled from 1.6% in mid-2016 to close to 3% last week. Rising yields do not just imply higher borrowing costs for companies and governments, but also potentially make shares relatively less attractive, hence the renewed volatility on equity markets.

In a quarterly outlook for monetary policy, Fed officials indicated in December that there were likely to be three hikes this year. Could the Fed instead hike four times? It still seems unlikely. The Fed did not overreact last year when inflation unexpectedly declined and stayed low. There is no reason to overreact now that growth is strong and inflation is rising, partly due to the low base set last year. Moreover, the Fed started hiking rates in December 2015 – when there was no inflation in sight - precisely so that they wouldn’t have to overreact when inflation did make a comeback, as forecasts suggested.

The European Central Bank (ECB) also released minutes from its monetary policy meeting last week. It has been impressed by the “robust and broad-based” economic expansion in the Eurozone and is now more confident that inflation will eventually move up to its 2% target. However, the ECB is not in a hurry, especially as a strong euro could put downward pressure on prices and export revenues.

The global backdrop therefore remains supportive for South Africa, with strong global economic growth, firmer commodity prices, inflation that is still mild (but rising) and central banks that are careful not to overreact.

An investor-friendly Budget

While global markets were choppy last week, Wednesday’s Budget is positive for local markets even though consumers will cough up more at the tills and petrol pumps. From the point of view of individual investors, the Budget is positive too. For one thing, there are no additional taxes on investment returns (in the form of capital gains tax or dividend withholding tax).

The deficit for the current fiscal year is likely to be 4.3% of GDP, in line with the October Medium-Term Budget’s revised projection. But unlike October, there is now a plan in place to narrow the deficit over time by cutting R85bn on the spending side over the next three years and raising additional revenue.

An additional R36bn in revenue will be raised, mostly by hiking the Value-Added Tax (VAT) rate from 14% to 15%, the first such increase in 25 years. The VAT increase will raise an additional R22bn. Other indirect taxes such as the fuel levy and excise duties will add around R2bn. On the direct personal tax side, there is some fiscal drag relief (R7.3bn) but government will still get R6.8bn from the impact of inflation pushing taxpayers into higher tax brackets (fiscal drag). But there are no further increases in direct individual taxes.

The budget deficit is therefore projected to decline to 3.6% in the subsequent two years, eventually settling at 3.5%. If this is achieved, the debt-to-GDP ratio can stabilise at 56% in 2022, an acceptable level in the global context, and much better than the 60% ratio predicted in October.

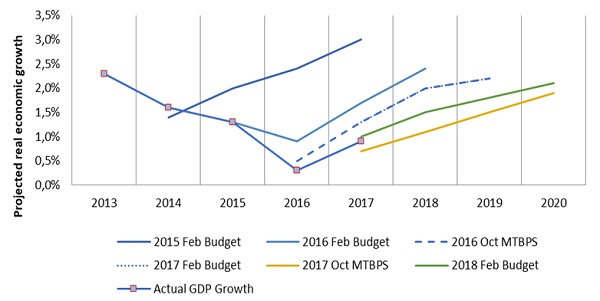

The deficit projections are made on fairly conservative growth assumptions. National Treasury expects growth to increase from 1% in 2017 to 1.5% next year and 1.8% in 2019. It is the first time since 2012 that Treasury is upgrading its forecasts from the prior year’s estimates, rather than cutting them. The persistent disappointment in growth over the past few years is the main reason why the deficit failed to narrow below 4% (though Treasury noted in the Budget review “policy choices” and high public sector wage increases also played a role).

Budget should support current rating

By putting state finances on a more sustainable path, the government should create a more accommodative overall investment climate. The Budget probably did enough to secure South Africa’s current Moody’s credit rating. Moody’s is the last of the three main ratings agencies to still rate South African local currency bonds as investment grade. A downgrade from Moody’s would see government bonds fall out of the Citigroup World Government Bond Index, leading to forced selling by those foreign investors who track the index.

However, the Budget on its own will not be enough to result in ratings upgrades. The ratings agencies will want to see, firstly, progress on achieving fiscal consolidation; and secondly, improved growth. Thirdly, they will want to see evidence that the financial risks at State-owned Enterprises are being reduced and that promises to introduce private sector participation are being translated into action.

The renewed focus on fiscal consolidation should help push longer-term borrowing costs (bond yields) down further, supporting other asset classes in the process. The yield on the 10-year SA government bond fell below 8% for the first time since May 2015, as the bond market cheered the Budget speech.

More freedom to choose

With the offshore allocation of balanced funds lifted from 25% to 30%, fund managers will have more freedom to allocate based on expected return and valuation. Institutional investors can also increase African exposure from 5% to 10%. This is probably the biggest surprise for local investors. The further easing of capital controls demonstrates government’s confidence in the local economy and local assets. The experience of recent times (2011- 2015) showed that it was useful to the domestic economy (and the fiscus) for South Africans to have substantial foreign assets in a declining rand environment, acting as a shock absorber.

Changes to offshore exposure (currently at the maximum of 25% for most balanced funds, including ours) will need careful reconsideration. For one thing, the rand is probably in fair to slightly overvalued territory on a purchasing power parity (PPP) basis after the strong appreciation of the past two years.

Tighter fiscal policy allows for looser monetary policy

Last week’s Budget also makes it easier for the Reserve Bank to focus on the inflation outlook, rather than playing a risk management role (being an anchor of institutional stability and independence during the turbulent recent past). Though the SARB’s thinking has shifted towards a greater emphasis on getting inflation to the midpoint of the 3% - 6% target range, rather than simply within the range, there is scope for interest rate cuts.

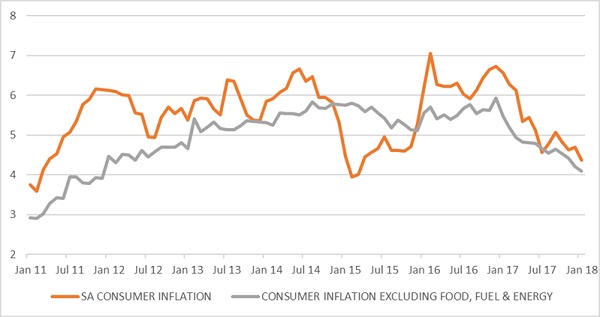

Local inflation eased to 4.4% in January from 4.7% in December. Food inflation declined to 4.6%, but meat inflation remains elevated at 13.4% (it is the only item in the consumer price index that posted double-digit gains on an annual basis). The petrol price fell by 1.3% in January, lowering annual inflation to 9.1%. The February petrol inflation should fall further to 3.7%, while a current over-recovery of 34 cents per litre should see March petrol inflation fall to 2.2%. However, a 22 cents per litre hike in the fuel levy and 30 cents per litre hike in the Road Accident Fund levy are effective from April.

Core inflation, a measure that excludes volatile food and fuel inflation to isolate underlying price pressures, fell to 4.1% in January, the lowest level since December 2011.

The increases in indirect taxes such as the fuel levy and the VAT rate will likely put some upward pressure on inflation, but won’t materially change the positive inflation outlook. The VAT hike in particular is likely to be a once-off, and will roll out of the year-on-year inflation numbers within 12 months of taking effect.

In other words, consumers will feel a bit of a pinch in the coming year as a result of the indirect tax increases. However, by taking this step towards restoring credibility in fiscal policymaking and putting state finances on a sounder footing, the Budget serves the longer-term interests of all South Africans, including investors. The prospects for decent investment returns from local assets have therefore improved over the past few days.

Chart 1: South African rand and bond yield

Source: Datastream

Chart 2: Treasury economic growth forecasts versus actual performance

Source: National Treasury

Chart 3: Headline and core consumer inflation

Source: StatsSA