An eventful first half of the year

Dave Mohr, Old Mutual Multi-Manager.

Izak Odendaal, Old Mutual Multi-Manager.

Reaching the half-way mark of the year offers an opportunity to reflect on the main events and trends shaping market dynamics.

Brexit – more questions than answers

The United Kingdom’s (UK) unexpected vote to leave the European Union (EU) sent the pound in a tailspin and caused equity markets to sell off. It also saw Standard and Poors’ stripping the UK’s AAA credit rating by two notches, while the two major political parties, the Conservatives and the Labour Party, seem to be tearing apart. This climate of uncertainty is undoubtedly negative for the UK economy (businesses are unlikely to make long-term decisions until there is greater clarity and households will also hold back), but the spill-overs to the rest of the global economy might not be so bad. The Brexit might not even happen. The UK remains a member of the EU until it submits the so-called Article 50 notice to leave. European leaders have indicated that they want things to move swiftly, but they cannot force the Brexit. The referendum only asked an in/out question, but not what should happen after a Leave vote and it is clear that many Leave voters misunderstood the implications of Brexit. At the very least, it will be up to the new Prime Minister to submit the Article 50 notice. David Cameron said that he will step down in September and by then the appetite to leave might be lacking.

If there is a Brexit, the UK will probably push for the ‘Norway model’, maintaining a free-trade relationship with the EU without being a member. The sticking point will be that the EU will link trade access to free movement of people, which has been the key issue for the Leave campaign.

While equities were sharply down the first two days after the vote, global markets appear to have stabilised. It means that year-to-date, US equities are flat, having somewhat recovered from the sharp declines in January. The S&P500 ended June flat, returning 4% year-to-date and 3.5% over the past year. UK equities recovered after the shock vote with a return of 4.7% in June, taking the year-to-date return to 7%. European equities took more pain on the Brexit vote. This is partly because the weaker pound softened the blow for the FTSE (much like the JSE generally benefits from a weaker rand), and partly because European bank shares suffered heavy blows. The Eurostoxx Banks Index lost almost 20% in June. The broad Eurostoxx 600 Index lost 4% in June, and 5% in the first six months of the year.

As the yen strengthened on rising global risk aversion, Japanese equities suffered with the Nikkei losing 9% in June and almost 16% down year-to-date. The stronger yen is a massive headache for the Bank of Japan and the Government, who are still trying to lift the country out of its deflationary condition.

Looking at the local equity market, the FTSE/JSE All Share lost 3% in June, with all three major sectors in the red. The All Share returned 2% for the first six months of the year and flat over one year.

Bond yields still falling

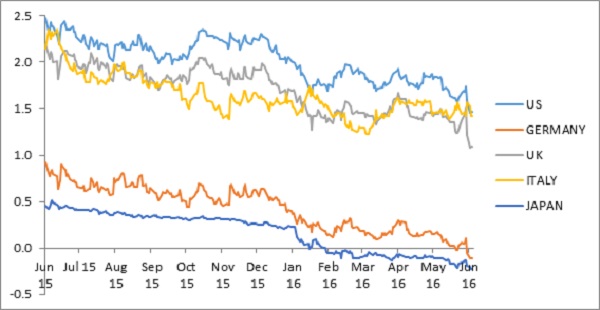

Bond yields, in contrast, continued to collapse post the Brexit vote, responding to more deep-seated forces. At the start of the year, the consensus forecast was that the US 10-year yield would rise above 2.5%. Instead it touched 1.4%. At the start of the year, the US Federal Reserve (Fed) saw four interest rate hikes; but now only perceives two hikes while the market expects one at the most. The UK 10-year fell below 1%, the lowest level ever. German and Japanese yields fell further into negative territory. Despite the renewed concerns over the future of the European single market, the yields of vulnerable countries (and the spread over German yields) increased marginally. Unlike in 2012, the European Central Bank’s presence appears to be a source of stability in the bond market. Emerging market bonds were bumpy in the aftermath of the vote, but most emerging market bond yields are lower than at the start of the year. For instance, the South African 10-year bond yield fell from 9.7% at the beginning of 2016 to 8.6%. The All Bond Index returned 11% this year, handsomely beating local equities, as the probability has increased that we are close to the peak of the local interest rate cycle. Brexit has therefore not caused an interest rate shock to the world economy.

Part of the reason why emerging market bonds have been stable is that emerging market currencies have been remarkably stable. Although the rand has swung around before and after the Brexit vote, these moves were within its normal range of volatility. The rand is still 17% weaker against the US dollar over one year providing a significant boost to the offshore returns of South African investors (especially since the underlying US dollar returns were unexciting). However, for the first six months of the year the rand gained 5% against the US dollar. It was, slightly stronger against the euro and 16% stronger against the globally weak British pound.

Brexit fall-out contained

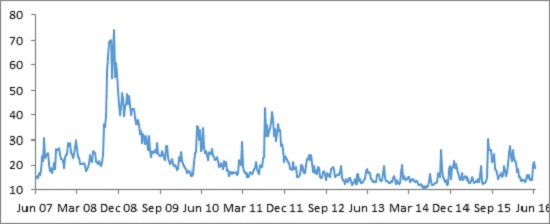

So far, the fall-out from Brexit remains contained to certain corners of the market, unlike the panic-attacks the market experienced in August last year and again in January this year when the oil price was slumping, the Fed was in tightening mode and fears of a hard landing in China (and sharp devaluation of the yuan) took centre stage. A simple comparison of the CBOE Volatility Index in chart 2 shows the relative market calm. This has been a picnic compared to 2008, and is clearly not another ‘Lehman moment’. These three areas of concern – oil, the Fed, and China – have each been taken care of mostly. Although weaker immediately after the Brexit vote, oil is back around US$50 per barrel, a level producers and consumers could probably live with. The Fed has turned dovish and will require really strong US data to resume hiking. Chinese authorities threw the kitchen sink at their economy earlier in the year and it appears to have worked. Growth has stabilised (although the long-term trajectory is still lower); the yuan is now weaker, but not dramatically so and trading more freely, which means that the bleeding of foreign exchange reserves has come to an end.

A difficult year for investors

In summary, the first half of 2016 has been difficult for investors, with volatility taking its usual psychological toll. Although returns have been better than feared in January after the worst start to a calendar year in decades, one-year returns are subdued across all asset classes. Investors might be tempted to turn to the few areas of the market that have done well (like gold or German bonds), but the shock Brexit outcome reminds us that surprises always lurk and when they do, they create challenges and opportunities. An appropriately diversified remains the best way to be positioned for future uncertainty.

Chart 1: Developed market 10-year Government bond yields, %

Source: Datastream

Chart 2: The CBOE Volatility Index (VIX)

Source: Datastream

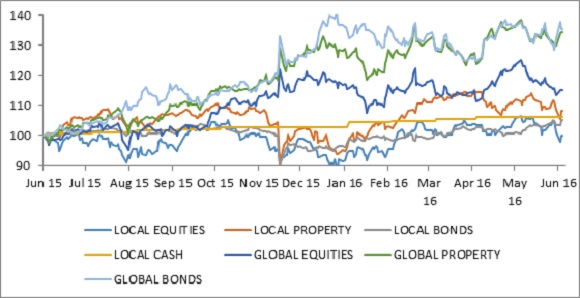

Chart 3: South Africa asset classes over 1 year in rand

Source: Datastream