All about the oil

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

Financial markets have been dominated by the collapse in the oil price over the past few weeks. The fall in the oil price is partly due to lower-than-expected demand because of slower global growth. It is easy to forget that China’s nominal economic growth rate has halved since 2011, while Japanese and European growth is also disappointing. According to the International Energy Agency (IEA), global oil demand in the third quarter of 2014 was estimated 93.06 millions of barrels per day (mbpd), up from 91.02 mbpd two years ago. All the action has been happening on the supply side. According to the IEA, oil supply has surged to 93.6mbpd from 90mbpd in the third quarter of 2012. Most of this increase comes from North America, where shale oil has doubled American output over the past five years, and is set to continue increasing as oil is extracted from shale and tar sands.

The other factor behind the falling oil price is the surging US dollar. Since oil (and other commodities) is priced in dollars, a strong dollar tends to result in lower prices. The dollar touched $1.23 against the euro last week as investors continue to contrast the improving economic fortunes of the US with the ongoing stagnation in the Eurozone. The accompanying expectation is that US interest rates will increase relative to European rates over time. Ditto for Japan, where the yen has fallen to almost ¥120/$.

Winners and losers

The collapse in the price of crude oil creates winners and losers. (This is true of other commodity prices too, but to less dramatic extent since they began sliding much earlier.)

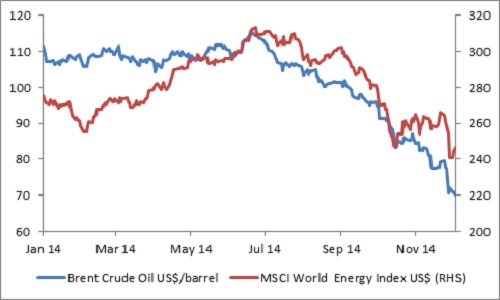

With oil falling briefly below $70/barrel last week, it is the producers – both companies and countries – that suffer. The OPEC (Organisation of Petroleum Exporting Countries) nations that used to control half of global production could manipulate the oil price agreeing to increase or decrease production. But OPEC’s share of world oil production has fallen to around 30%. It is more difficult for them to agree, and Saudi Arabia, the major OPEC producer appears to be more focused on market share than maintaining a high price. While most OPEC countries have very low production costs and can therefore still profitably pump oil at current levels, their government budgets are so reliant on oil revenues that $100/b is necessary to balance the books.

Russia, Norway, Venezuela and Nigeria all saw large declines in their currencies. The depreciation of the Nigerian naira placed pressure on the MTN share price. With large dollar-denominated debts, Russian companies are taking strain. The oil market can succeed where sanctions have failed.

The shares of oil companies have taken a pounding. The MSCI Energy Index has lost 20% since the end of June. Locally, Sasol’s share prices slumped, while the broader resources sector also suffered. These shares have large weights in the JSE All Share Index, resulting in the largest one-day fall on the local market in over four years.

Net oil importers obviously benefit, especially those like India that run large current account deficits. Global consumers will be the biggest beneficiary. This is important at a time when global growth is slowing (witness the softer PMI numbers discussed below).

On a net basis, the collapse in the oil price is good for the world economy, especially when demand is so weak. The consumers of oil – households and businesses - are distributed widely across the surface of the earth, while the producers are concentrated in specific regions, often volatile parts of the world (such as the Middle East). In fact, it is no coincidence that geopolitical concerns are often centred on oil producing regions. As a consequence, the oil price normally carried a significant risk premium. It appears that the shale revolution in the US has removed this premium for the time being.

Lower oil prices will also result in lower headline inflation numbers. The Federal Reserve focuses on ‘core’ inflation, excluding volatile food and energy prices. They will therefore probably attempt to look through the current low oil price, but it does buy them time. For the SA Reserve Bank, the lower oil price also creates breathing room. For the European Central Bank, it creates a headache, with its targeted inflation level already at 0.3% and falling.

Will it last?

In market economies, price moves elicit a supply response. However, with commodity prices there is always a lag. This is partly because producers tend to hedge output at prevailing prices, but mostly because it takes so long to bring new supply to market (sometimes several years). High real prices of oil over the past decade encouraged the current flood of production and also lead to consumers trying to find alternatives or consume less. Low prices have the opposite effect, and the world could still find itself short of oil in a few years’ time. But for now it appears that oil prices are unlikely to reach triple digits soon.

Chart 1: The oil price and energy equities in 2014

Source: Datastream

Global manufacturing softer in November

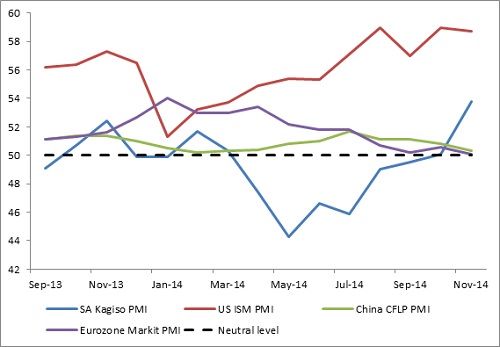

The local Kagiso purchasing managers’ index (PMI) improved for the fourth consecutive month to 53.3 index points in November. A reading above 50 index points means that the sector is expanding. However, rather than pointing to strong underlying momentum in local manufacturing, the PMI probably reflects a normalisation of conditions after the strikes in the platinum and metals sectors. A large part of the local manufacturing sector services mining. And while there haven’t been any more mining-related strikes, falling commodity prices have made mine bosses reticent to invest. JSE-listed manufacturer Bell Equipment last week announced plans to restructure and cut jobs as mines postpone orders for its earthmoving equipment. While new sales orders rose and inventories remained virtually unchanged, the PMI leading indicator improved but remained below one, signalling that there is still limited incentive to ramp up production.

Fourth quarter looking better

The average PMI for the first two months of the fourth quarter is 3.8 points higher than the average in the third quarter, suggesting positive growth for the manufacturing sector in the final quarter after contracting during the first three quarters. However, data from Naamsa shows that new vehicle sales fell in November, and the average for the fourth quarter so far is lower than last quarter. The silver lining in the new vehicle sales numbers is the continued increase in vehicle exports. New vehicle sales are a useful indicator of business and consumer confidence, credit conditions and the manufacturing environment.

China and Eurozone hugging the 50 points line

South Africa’s PMI moved in the opposite direction to most other major economies, another reason not to assume that local industry has entered a strong growth phase, rather than just rebounding from a depressed base. The JP Morgan Global Manufacturing PMI fell to 51.8 in November, the lowest level in 14 months. But this reading still suggests that 90% of global manufacturing output is experiencing positive growth. China’s HSBC manufacturing PMI fell to a six-month low of 50 as output dipped and employment fell. The official PMI, which focuses on larger state-influenced firms, fell from 50.8 in October to 50.3 in November, mirroring the fall in the HSBC PMI. The growth slowdown in China, in turn, is of course a big reason behind lower commodity prices.

The Eurozone manufacturing PMI came in at 50.1 in November, down from 50.6 in October due to slower output growth and falling levels of new business. Growth in Spain, Ireland and the Netherlands was offset by contractions in Germany, France and Italy. The latter three are the biggest economies in the Eurozone, so this is a concerning development.

US and Japan still in positive territory

Japan’s manufacturing was down slightly from 52.4 in October at 52.0 in November, but remained above 50. The weak yen has not resulted in an export surge for Japanese manufacturers, but it has allowed them to improve margins.

The US Markit manufacturing PMI fell to 54.8 from 55.9 in October. The more long-standing ISM index was at 58.7, down from 59 in October. While manufacturing sentiment in the US has dipped over the past three months, it remains at levels consistent with a sustainable expansion. A separate data release last week showed that vehicle sales in the US remains close to record levels at 16 million a year, while the proportion of locally-manufactured vehicles sold continues to climb to above 80%.

Chart 2: global manufacturing PMIs

Source: Markit, BER, ISM