Active investment managers more likely to outperform at the next market inflection point

While popular wisdom holds that passive investment strategies will always be better than an active strategy, this will not always be the case, particularly at market inflection points like the one that potentially lies ahead.

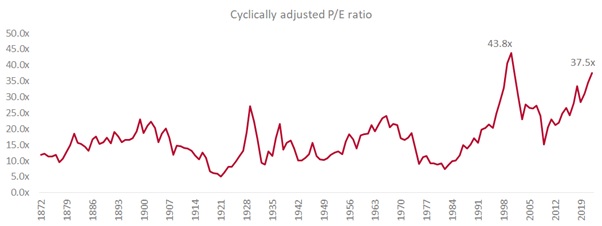

Flagship Asset Management fund manager Kyle Wales points out that market inflection points typically arise when markets generally appear expensive or cheap – and a key valuation measure, the cyclically adjusted price-earnings ratio, is currently trading at its second-highest level over the last century.

He argues that not only have well-selected actively managed equity funds demonstrated an ability to outperform the market over time, but the likelihood of any active manager doing so is higher at market inflection points because they can construct portfolios that are less correlated to overall market performance

The ability to outperform passive investment strategies is especially true of flexible funds because fund managers have an additional bow in their quivers as they can adjust allocation in addition to only being able to select equities. It is much harder to craft an index that does the former effectively.

Wales notes that while the benefits of active and passive management have been given a lot of airtime, questions that are raised less frequently are: If I commit a portion of my funds to an active asset manager:

• How do I choose the right active manager? and

• When is the best time to buy or increase my allocation to the right active manager?

Choosing the right active manager

On the first, Wales says: “Choosing the right active manager is essential if you want to achieve returns that outperform the market and don’t just follow the market up and down.” Firstly investors need to select an active manager that is actually an active asset manager. Secondly, they need to choose a manager that has demonstrated their ability to outperform over extended periods.

“Regarding the first point, many managers claim to be active managers, but their portfolios resemble the benchmarks they are paid to outperform so closely that they are virtually guaranteed to underperform. The reason for this is that the extra fee they charge is unlikely to be offset by the potential outperformance that their portfolio can generate,” says Wales.

Signs that a manager is guilty of this practice (referred to as “index hugging”) is that they hold a diluted portfolio with many small positions. Their portfolios exhibit a low tracking error, with the fund performance closely matching the benchmark and a low active share, where the portfolio looks very much like the benchmark weightings. The last two measures show how different the manager’s portfolio is from the market as a whole.

“At Flagship,” says Wales, “we run concentrated portfolios that by default will look nothing like the index they are benchmarked against.”

The second key consideration should be whether an active manager has demonstrated their ability to outperform over extended periods and done so by following a consistent philosophy and process. This is essential because it indicates that the portfolio manager’s performance is more due to skill than to luck

When is the best time to increase my allocation to an active manager?

While certain active managers have proved their ability to outperform the market consistently over time, there are certain times when active managers in aggregate have outperformed the market.

According to the SPIVA Report, published by S&P Global annually, active managers in aggregate outperformed the S&P 500 in both 2001 (after the dotcom bubble) and 2009 (after the global financial crisis).

Says Wales: “The reason why active managers tend to outperform during these times of massive dislocation is that index funds are, by their nature, procyclical. The nature of indexing forces the passive investor to buy more of the shares that are becoming more expensive and to sell the shares that are becoming cheaper. This is the opposite of what active investors, who believe that every asset has a fair price, try to do. They aim to buy assets for below what they are worth and sell them when their prices get ahead of themselves.”

Could we be sitting at such an inflection point today? Perhaps. Post the COVID crisis sell-off in the first quarter of 2020, the S&P 500 is now up 40.7% over one year , up 65.3% over three years and 120.5% over five years. The current expansionary cycle has lasted more than ten years, twice as long as the typical expansionary cycle.

A useful measure of the equity market’s valuation, cyclically adjusted price/earnings (CAPE) ratio for the S&P 500, tells us that the risks of a correction are building, notes Wales. The CAPE ratio is calculated by taking the current price of the S&P 500 and dividing it by the average inflation-adjusted earnings over the last ten years to adjust for cyclicality. It is currently at its second-highest level over the last century. The only time the market has been more expensive than today was at the peak of the dot com bubble of the early 2000s.

Source: Bloomberg

“It is at moments such as these that an actively managed equity fund can provide one with protection because even though the market as a whole may appear expensive,” says Wales, “there will always be individual stocks that are underpriced relative to their long-term growth prospects.” Flexible funds also come into their own because fund managers can adjust asset allocations as well. Wales adds that Flagship’s longest-running strategy, the flexible strategy, created significant value for clients during the COVID led sell-off by adding aggressively to the equity allocation as market prices fell.

The media is awash with articles decrying active managers, but the situation is more nuanced than this. In every human endeavour, there will be winners and losers. Wales highlights that to be a “winner” in active asset management, you have to generate better returns than those that would deliver the same returns as the index when adjusting for higher fees. It is excellence that all of us are after, and it is possible to find excellent fund managers if we look for them in the right way and try to find them at the right time.”