A roundup of risks

Risk comes in many forms. In the investment industry “risk” is often used as shorthand for “volatility”, as in the risk/return scatterplots that are a staple of fund performance presentations.

But volatility is not the same as risk. Volatility is a form of risk for some people, especially when drawing down retirement savings, but an opportunity for others. Volatile markets can create attractive entry points for long-term investors, particularly when making regular contributions. Traders also love the chance to ride prices up and down.

Risk therefore is very subjective and not fixed. Our perceptions of risk also change. We tend to be more risk-averse after a scary event, and more risk tolerant when things are going well. This is exactly the wrong way round.

Minsky moment

A version of this is the once-forgotten three-stage “financial instability hypothesis” of economist Hyman Minsky, which came back to prominence after the 2008 Financial Crisis. Basically, the theory is that a period of stability leads to instability. Initially after a recession or financial crisis, banks and borrowers are cautious and risk appetite is low. But in the second stage, as asset prices recover, so does confidence, causing borrowing to increase. The third stage is reached when the crisis is a distant memory and borrowing increases to an extent where neither interest nor capital can be repaid unless asset prices keep rising. When they stop rising, the house of cards collapses and the ‘Minsky moment’ is reached.

In other words, as an investor you should be most worried precisely when no one else is worried. When everything seems to be going swimmingly, there is probably a shark lurking beneath the waves.

This is clearly not the case now, as jitters abound. Health risks are an ongoing major source of concern as the world continues to grapple with the Covid-19 pandemic and the highly contagious Delta variant. Top of mind for many South African investors in the wake of the devastating recent unrest and looting in KZN and Gauteng is socio-political risk. Last week highlighted other forms of risk for investors.

Regulatory risk

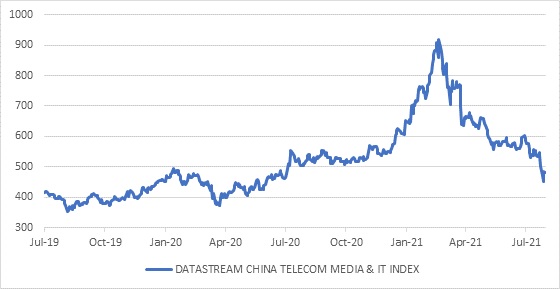

Last week’s headline-grabbing market moves were caused by plunging Chinese technology shares as authorities take a tougher stance on the sector. China is not the only country seeking to tighten the regulation of its big technology firms. Internet technology has generally developed faster than rules on data protection, cyber security and competition and there is a degree of consensus globally that the big tech companies have abused their dominance.

Chinese regulators just tend to be more heavy-handed than their counterparts elsewhere. After all, it is not a democracy and reasserting state control over this fast-growing sector (and the individuals who become very wealthy from it) also seems to be playing a role in recent actions.

Chart 1: Chinese technology shares

Source: Refinitiv Datastream

Beijing is also worried that the rising cost of urban living is making it unaffordable to raise children. It has abandoned its one-child policy and now wants to encourage larger families, to counteract its shrinking labour force. To this end, authorities ruled that companies offering home-schooling or off-campus education would have to become non-profits, a huge blow to a sector that was flourishing and profitable.

There have been similar interventions in the past, such as the 2013 crackdown on the giving of expensive gifts to officials, which temporarily knocked the sales of luxury goods. Things tend to settle down after a period of uncertainty once Beijing is satisfied that everyone is playing by its rules. This is likely to be the case now as well.

Concentration risk

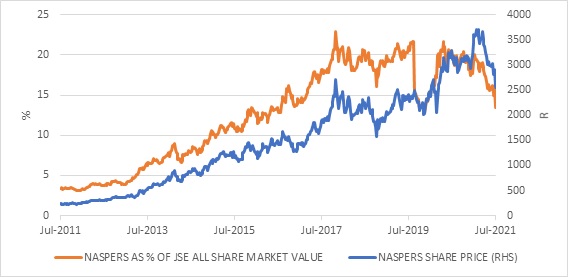

One of the Chinese tech giants, Tencent, is of course well-known to South African investors. The biggest share on the JSE, Naspers, derives most of its value from its holding in Tencent.

Based on Tencent’s staggering growth, Naspers went from a 4% weight in the FTSE/ All Share Index to 15% in the past decade. We introduced the FTSE/JSE Capped SWIX as an equity benchmark in 2018 to reduce concentration risk (it caps the weight of any one share at 10%). Although Naspers created phenomenal value for investors in the past decade, there are risks in falling in love with any investment and letting it become too big a part of your portfolio.

In any event, diversification worked in recent days, as the local market enjoyed a strong month in July despite its biggest share falling and despite the impact of the unrest and looting on retailers and property stocks.

Chart 2: Naspers market value as % of JSE All Share market value

Policy risk

Ultra-easy monetary policy in the form of negative real interest rates and massive central bank purchases of bonds has been a feature of the global financial landscape for 12 and a half years. Well before the pandemic, in other words.

However, as the world starts returning to normal, the need for some of these emergency measures is reduced. This is particularly true for the US, the world’s most important economy, where real economic activity surpassed pre-pandemic levels in the second quarter.

Its central bank, the Federal Reserve, noted at last week’s monetary policy meeting that there had been progress towards its goals of low unemployment and 2% average inflation over the medium term. The Fed had previously stated that “substantial progress” would be needed before tapering of its $120 billion a month bond buying programme would begin. So, is the progress substantial enough? There is disagreement among Fed policymakers on when and how to proceed, and no further announcements were made.

The mixed messages on policy create a tricky backdrop, but as much as everyone wants certainty from the Fed and other central banks, they are also observing the economy and making decisions based on what they see happening. The future is as unpredictable for them as it is for us. A Fed with itchy trigger fingers is one of the biggest single risks investors face. As much as it always tries to engineer a soft landing, it has historically overdone interest rate hikes. However, in the current cycle, it seems particularly careful not to repeat past mistakes. This could, however, lead to Minsky problems down the road if rates remain too low for too long.

Cyber risk

As the world becomes more reliant on technology, we also become more vulnerable to technological disruptions. A cyber-attack on Transnet’s IT system caused it to declare force majeure at the country’s main container terminals. It had to switch to manual processing, paralysing trade for several days at a time when it is exports that have been keeping the economy afloat. The reasons behind the attack and the cost in lost trade are still unknown, but it is concerning that vital national infrastructure is this vulnerable.

The latest trade numbers from SARS predate this incident and show that the economy posted yet another massive trade surplus in June to the tune of R57 billion, with exports of R166 billion lifted by the commodity price boom. A back-of-the-matchbox calculation suggests that a week’s shutdown of the country’s ports could have disrupted trade to the value of R68 billion.

Fiscal risk

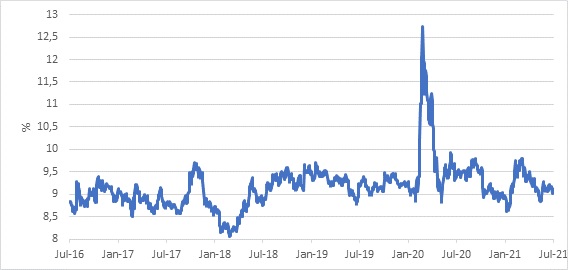

For buyers of bonds, there are typically three big risks. Inflation erodes the purchasing power of fixed interest payments. Rising short-term interest rates is an opportunity cost if you are locked into a long-term bond with lower rates. The third risk is the failure of the borrower to make interest payments or to repay the full capital amount (or both). Bond prices therefore include investors’ assessment of future inflation, interest rates and also creditworthiness of the borrower.

For South African government bonds, the latter looms large, as the government has accumulated a sizable pile of debt and continues to fund a large budget deficit through ongoing borrowing. If debt becomes too much, the risk of default increases. However, historically countries have often defaulted on relatively low levels of debt when faced with a cash crunch, or massive short-term debt maturities particularly if the debt is in hard currency. The South African government does not have much hard currency debt, which helps.

Chart 3: 10-year South African government bond yield, %

Source: Refinitiv Datastream

The government has long promised to address its rising debt burden by slowing spending and raising tax revenue, but this has proved to be difficult. The hard lockdown early last year made things much worse, as tax revenues plunged while health and social assistance spending increased. In the past few months, however, tax revenues have risen better than anticipated, thanks to the commodity boom and faster growth in the broader economy.

Therefore, the government could respond to the recent unrest mostly by utilising this tax revenue overrun rather than borrowing more. The bulk of the R39 billion assistance package - R27 billion in total - will go towards a reinstatement of the R350 per month social relief of distress grant until March 2022.

The debate on the social safety net has shifted since the July unrest. There is now broader agreement that extreme poverty and inequality can lead to future episodes of damaging instability. The debate is now on the “how”, not the “whether”. Some argue for a basic income grant, while the Finance Minister has reiterated that he would rather expand measures that encourage employment (such as youth employment subsidies and public works). Either way, it will have to be accommodated by changing government spending or raising taxes, or both. We cannot bank on commodity price windfalls every year.

Some good news is that the majority of public labour unions have accepted government's wage offer of a 1.5% increase plus a monthly non-pensionable cash gratuity of between R1 200 and R1 600. While this is clearly more than the zero increase the government initially offered, all things considered it is a reasonable outcome. It can largely be accommodated within the existing fiscal framework, demonstrating that the government is still committed to sticking to its consolidation plans.

Ultimately, we need faster economic growth and job creation along with spending discipline to ensure long-term debt sustainability. But for now, the risk of debt default remains low and bonds delivered a positive return in the month of July.

Luck, risk and balance

Markets are usually pretty good at pricing in known risks. By the time you read about something in the media, it is already reflected in asset prices. However, there are always risks, both old and new, and the consensus view is sometimes wrong. Sometimes, too much risk can be priced in, which creates an investment opportunity. Sometimes, investors are complacent in the face of real danger. And of course, any number of unpredictable things might happen. There’s no denying luck plays a part.

Risks can cause three behavioural errors. Firstly, investors can panic when a new worry emerges and completely abandon their investments. By the time they do so, however, the new risk has probably already been discounted by the market and they just end up locking in losses.

Secondly, people surveying the landscape can conclude that things are just too uncertain to invest, and they stay on the sidelines. By the time they finally have the confidence to dip their toes in the water, they’ve missed out. The last year and a half is a perfect example.

The third risk is the inverse of the second. When everything seems rosy and there are a hundred reasons why a particular investment can only keep going up, there is the risk of overexposure (even worse when fuelled with debt) and a Minsky moment.

On the other hand, investors with appropriately diversified portfolios can have confidence that they are protected from these three errors. A sensibly balanced portfolio is not going to be wiped out by any single risk materialising.