A new high

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

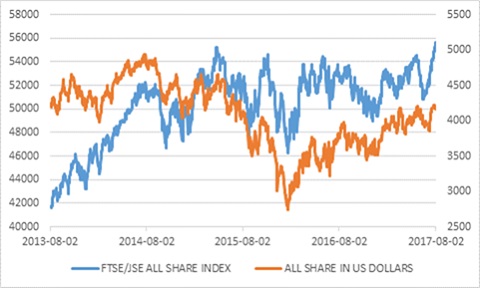

The FTSE/JSE All Share Index (Alsi) finally hit a new all-time high closing price above 55 400 points, surpassing a record set in April 2015. This is a relief for most South African investors as local equities would constitute the bulk of their portfolios (and will likely continue to do so as long as the Pension Funds Act limits offshore exposure to 25%).

A few observations on the new record: Firstly, the index level excludes dividends. When included, the total return index hit new highs in 2016 and earlier this year as well. Dividends are a crucial part of any investor’s portfolio, and cannot be ignored, but since the Alsi’s index level is more widely quoted in the news, we’ll stick to that for now.

Secondly, it really is not an achievement to reach a new record after 26 months, when global markets have surged ahead. In the US, the Dow Jones Industrial Average topped 22 000 points for the first time amid much fanfare last week; it was at 17 000 in April 2015. (As an equity benchmark the Dow is not that useful as it weighs companies by how high their share price is, not on their market capitalisation, but it does illustrate the point.) In dollar terms, the Alsi peaked in July 2008, and despite a strong rally since early 2016, it is still well below that level - a lost decade for global investors in South Africa.

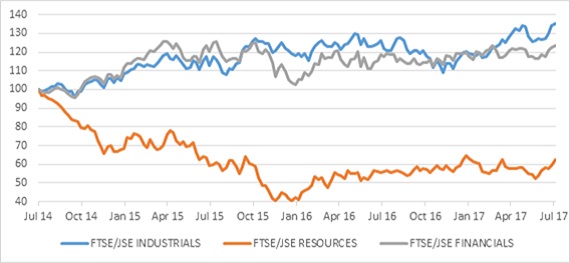

So why did the Alsi take so long to surpass its previous peak? Broadly speaking, the JSE’s resources index collapsed in 2015 along with commodity prices. In particular, there were concerns that some large mining companies might fold under the weight of debt accumulated when commodity prices were much higher. In 2016 resources recovered but the stronger rand weighed on rand-hedge industrials. Finally, in 2017, there was a fairly broad-based recovery across sectors on the local market. Resource companies have been delivering decent results based on more favourable commodity prices. Though volatile, the rand has broadly trended sideways this year, meaning that the global consumer shares listed on the JSE could rise along with their international peers. Finally, financials have benefited from declining interest rate expectations. There are still sectors that are struggling, particularly healthcare, which is down 7% year-to-date, construction (-5%) and household goods (-5%). It is also worth pointing out that while the gains this year are spread across sectors, they are not spread across the market capitalisation scale. Large caps (the Top 40 index) delivered 14% year-to-date, but the mid-cap index and small cap indices are both negative.

Looking ahead

So what is the outlook? Ultimately, nobody knows where the Alsi will be next week, next month or next year. What we do know is that its constituent companies grow their profits over time (paying some of it out as a dividend, retaining the rest for reinvestment) and that share prices should rise to reflect those growing profits over time. But in the short term, the price that investors are willing to pay for future earnings is volatile and subject to sentiment.

Currently, the price investors are prepared today for future earnings (price to earnings ratio) at an index level is on the high side compared to its history (not excessively though, and not out of line with valuations of global). Other valuation measures like the price to book ratio are more reasonable, and at a company level there are individual shares offering value. Nevertheless, it means that there is limited scope for a re-rating for investors to further increase the price they are prepared to pay for each R1 of future earnings. Global sentiment will play a big role in whether the market re-rates or de-rates (i.e. how much investors are prepared to pay for that same R1 of future profits).

Global risk appetite improved

Global risk appetite has improved, with the US markets pushing to new record levels amid solid economic growth, a benign interest rate outlook, strong earnings results and a weaker dollar (which benefits US multinationals). European stocks face a bit of a headwind from a stronger euro, but are booming in dollar terms.

Emerging markets continue to storm ahead. The MSCI Emerging Markets Index’s 2017 return so far is 24% in US dollars. Despite this rally, the index is only back to its April 2015 level (much like the Alsi), and still well below its all-time peak set in October 2007. The weaker dollar – due to a combination of dampened expectations for US interest rate hikes, doubts over President Trump’s ability to implement growth-enhancing tax reform and overvaluation – helps emerging markets in three ways: firstly, dollar returns look much better (since most global investors measure returns in US dollar); secondly, stronger currencies support an improvement in some domestic fundamentals, by putting downward pressure on interest rates; thirdly, a weaker dollar reduces concerns over the sustainability of the estimated $9 trillion in dollar-denominated debt on the balance sheets of emerging market corporates.

Earnings outlook

In terms of earnings growth, company management plays a big role, but from a macro point of view, global growth, the rand, commodity prices and the state of the domestic economy will be key.

Commodity prices have bounced across a broad front over the past few weeks, as China reports healthy economic growth numbers, but overall commodity prices are still low compared to long-term real levels. A weak dollar and solid global growth should in theory support commodity prices. However, higher prices can lead to increased supply which will cap price increases.

Increasing importance of the rand

The rand is playing an increasing role in the prospects of the JSE, since it is now dominated by global, not domestic companies, while even companies that traditionally focused on the local economy are diversifying abroad (for instance, The Foschini Group recently acquired an Australian retailer, while Bidvest is expanding into Ireland and the UK). Already more than half of the earnings of JSE-listed companies are foreign and will be boosted by a weak rand. Stronger global growth should also benefit JSE-listed companies that operate abroad. Political and policy uncertainty will probably continue to add volatility to the rand in the run up to the ANC’s elective conference in December. The rand has also weakened ahead of the release of a scheduled Moody’s rating announcement on Friday. But the primary drivers of the rand remain global, especially sentiment towards emerging markets.

For those remaining companies that focus mostly on the domestic economy (mainly mid and small caps), the outlook for local growth is important and unfortunately not rosy. At least the second quarter data suggests that the economy has already exited the technical recession. For instance, retail sales posted a third consecutive positive month of annual growth in May and South Africa posted another trade surplus in June. The surplus for the first six months of the year is R27 billion, compared to a R5 billion deficit for the same period in 2016. New vehicle sales levels appear to have stabilised after relentlessly declining for two years. However, business and consumer confidence remain depressed. The BER/FNB Consumer Confidence Index spent a record twelfth consecutive quarter in net negative territory in the second quarter.

The manufacturing sector also continues to struggle, with the Absa/BER Manufacturing Purchasing Managers’ Index slumping by 3.8 index points to 42.9 in July, and thereby bucking the trend of global Purchasing Managers’ Indexes that have been quite strong. Ultimately, stronger global growth should benefit domestic firms too, given that South Africa tends to follow the global cycle with a lag.

Despite the SARB’s cut, real interest rates are still very high for the weak economy (the repo is around 1.5% when adjusted for inflation, but most borrowers pay prime-linked rates which are closer to 5% in real terms). There is a strong case for further rate cuts, which would relieve pressure on consumers. This should benefit rate-sensitive shares.

Keep calm and carry on

The improved performance from the local equity market is encouraging and future real return prospects are reasonable, if below the long-term average. It remains a very important part of South African investors’ portfolios, and should outperform bonds and cash over time. However, short-term volatility is always a factor with equity investing and investors’ patience and perseverance will be tested. History shows that it is worth it though.

Chart 1: FTSE/JSE All Share Index in rands and US dollars

Chart 2: JSE sector total return indices over the past three years, rebased to 100

Source: Datastream