A dynamic environment requires a flexible approach

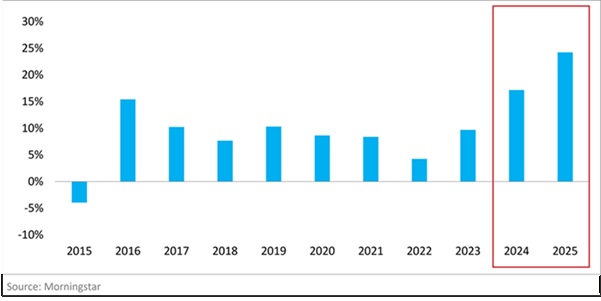

South African bond markets rewarded fixed income investors with exceptional calendar year returns in both 2024 and 2025 – the All Bond Index (ALBI) returned 17% and 24% respectively.

These returns are far above the norm, and so we anticipated moderating performance in 2026, especially as the market had repriced strongly as risk perceptions around the local economy and political climate improved, the risk premium decreased and foreign investors started finding our bonds attractive again.

FTSE/JSE All Bond

Thus, we entered 2026 with the prospects for local nominal government bond returns looking respectable, if less attractive than over the previous two years.

It’s been a tough year for bonds so far

Global developments in 2026 so far have not been supportive of bonds. The conflict in Iran sent oil prices sharply higher, triggering inflation spikes.

Compounding the inflation picture, the United States (US) is confronting a structural fiscal challenge that markets are no longer willing to ignore. With the federal deficit running at levels historically associated with wartime or crisis, and the Treasury needing to roll over and issue new debt at scale, bond investors (the so-called bond vigilantes) have reasserted themselves as an effective constraint on fiscal and monetary excess. In the absence of a credible consolidation path, the market itself is doing the work that policymakers have deferred, demanding higher yields as the price of continued financing. Consequently, we have seen US long-term bond yields edge up, with US 30-year paper trading at yields in excess of 5%. In this sense, rising US long yields are not a temporary tantrum but a considered repricing of sovereign risk.

What is often underappreciated is that even a bond that ultimately repays in full can inflict meaningful mark-to-market losses in the interim, and in the current environment, where short-term inflation fears are flaring, investors are demanding additional compensation simply to bear that uncertainty. This inflation risk premium – compensation for bearing uncertainty about future inflation rather than inflation itself – has pushed up nominal yields while also representing a higher hurdle for real returns globally.

Against this backdrop, South African nominal government bonds have perhaps held up better than expected. Despite weakening appreciably since mid-April, current yields on the 10-year bond of around 8.6% (27 May 2026) are still appreciably lower than the levels of above 11% recorded at the height of uncertainty around Budget 3.0 and the Government of National Unity (GNU) in March/April 2025.

Click here to read more...