A brave new world

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

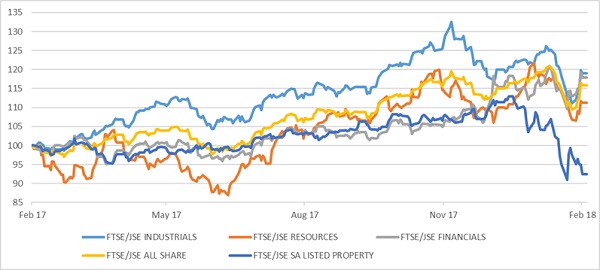

Investors cheered Jacob Zuma’s resignation as President on Valentine’s Day and were excited to see Cyril Ramaphosa sworn in as his successor the following afternoon. Markets had priced in the greater prospect for sensible policymaking, a tougher stance on corruption and economic reform since December, but with the certainty that the Zuma era is over, came a bounce in the rand, local equities and bonds. Listed property is still struggling as governance concerns weigh on the Resilient stable of companies.

Buoyant mood on the markets and the street

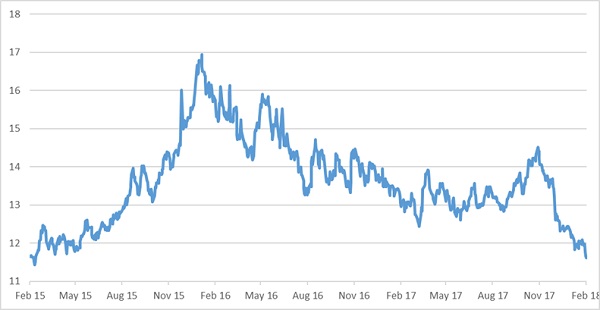

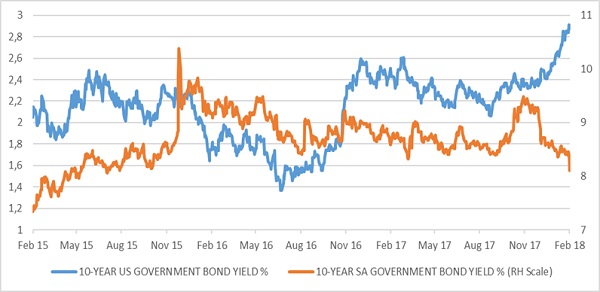

The FTSE/JSE All Share Index ended the week just shy of 60 000 points, while the 10-year government bond yield declined to 8.2%, a level last seen in October 2015. At the end of the week, the rand was trading at R11.60 against the US dollar, the strongest level since April 2015. The surge in the rand has been supported by a weaker dollar, but it also gained against the pound and euro.

Though the mood in the country has lifted considerably in recent days, there is much work to be done to capitalise on the optimism and also global goodwill. The first big test will be the appointment of a new Cabinet and the 2018 Budget Speech in Parliament on Wednesday. The timing is opportune, with strong global growth and positive investor sentiment towards emerging markets creating a window of opportunity to implement the necessary reforms, including ones that are potentially unpopular. A scan of international news media, including the financial press, makes it clear that the political changes are viewed very favourably and that South Africa is on investors’ radar screens again.

There are also indications that the local economy is improving on its own steam, after years of underperformance. Compared to a year ago, real retail sales growth was very healthy at 5.3%, while nominal growth was 7.3%. Along with wholesale sales, motor trade and manufacturing, electricity posted positive growth in the fourth quarter, suggesting that fourth quarter GDP could be 2%, which would put 2017’s growth as a whole at around 1%. Growth is clearly still very low and at the heart of the fiscal problems that the Budget Speech will seek to address this week, but it is up from only 0.3% growth in 2016.

Greater political and policy certainty from President Ramaphosa’s administration can add to the positive growth momentum. Confidence-boosting measures need to be implemented immediately, with the promise of more growth-enhancing structural reforms to follow. It will be tough, but for the first time in years the prospect of real improvement is on the horizon. The overall tone of Friday’s State of the Nation Address, with its emphasis on economic growth, job creation, corruption fighting and greater cooperation between the state and private sector, is therefore welcome. This points to improved creditworthiness against the backdrop of a supportive global environment, which reduces the probability of further ratings downgrades.

A new paradigm

On global markets, the question can also be asked if we are entering a brave new world. For years now, equity investors enjoyed the benefit of low inflation, low bond yields and supportive central banks. But we are slowly moving into a new paradigm as central banks, led by the US Federal Reserve, aim to gradually return monetary policy to a more normal stance, removing the emergency post-crisis stimulus measures of zero (or negative) rates and quantitative easing. The word “gradually” is key, and well-behaved inflation in turn is necessary for the monetary policy normalisation to proceed at a gradual pace.

That is why the market suddenly panicked two weeks ago when a data release showed rising US wage growth, seen as a precursor to rising inflation and therefore higher interest rates. Bonds and equities sold off very sharply in the case of the latter. US 10-year government bond yield touched 2.9%, the highest level since December 2013. This is driven largely by a rise in inflation expectations on the part of bond investors. The “breakeven” inflation rate over 10 years – the difference between the yield on nominal and inflation-linked bonds – has increased to 2% from a recent low of 1.6% in June last year.

But curiously, when data released last week showed that actual consumer inflation increased faster than expected (2.1% on an annual basis), the equity market shrugged it off. In fact, the main global markets were all strongly positive last week.

Fiscal and monetary policy at odds

A further complication in the case of the US is that monetary and fiscal policy are now moving in very different directions. In contrast to South Africa, where the Budget this week is expected to focus on measures that will reduce the government’s sticky 4% of GDP fiscal deficit through tax hikes and spending restraint, the Republican-controlled US government has implemented three budget-busting policy changes in just as many months.

First up was the December tax cuts for corporates and (mostly wealthy) individuals. This will cost $1.5 trillion over a decade. Then came a budget deal that sees spending increase by $300 billion over the next two years. And most recently, a $1.5 trillion infrastructure plan (of which the federal government will be on the hook for $200 billion). Fiscal stimulus of this nature works well when the economy is depressed with low interest rates and plenty of underutilised resources. It would have been very useful a few years ago. But the US is close to full employment now, and there is a small risk that this stimulus could push the economy into overheating territory, causing inflation to rise faster than expected and forcing the Fed’s hand to hike. Rather than the current slow and steady cycle, this could mean faster growth coming to a quicker end.

However, one also shouldn’t forget that the forces that suppressed inflation in recent years, including excess global productive capacity, a global labour force and technological advances, are still in place, while some of the factors behind the recent rise in inflation, such as the jump in the oil price above $60 per barrel, might prove temporary.

Trying to price in different scenarios

These are all the scenarios markets are grappling with which could lead to investor focus shifting in the coming months between strong economic growth and rising corporate earnings on the one hand, and the fear of rising inflation and interest rates on the other. How should investors handle such volatility? Diversification means not being fully exposed to the swings in any one sector or asset class.

Making regular investments (such as monthly pension fund contributions) means benefiting from dips in the market, so-called rand cost averaging. Investors who draw income have the opposite problem – potentially selling on the dips - and need to carefully consider their exposure to more volatile assets. But the trade-off between higher risk and higher return won’t disappear, unfortunately.

In all this it is important to keep emotions away from investment decisions. The surge in optimism among South Africans in recent days stands in stark contrast to the pessimism a year or two ago. Investment decisions based on that fear and gloom have probably backfired in many cases. Sensible and balanced decision-making from our new national leadership and the world’s central bankers is imperative, but it is also recommended for investors.

Chart 1: Rand-dollar exchange rate

Chart 2: South African and US 10-year government bond yields

Chart 3: FTSE/JSE All Share Index with main subsectors

Source: Datastream