A better – and very different – tomorrow

Following the endless stream of Covid-19 headlines, extended lockdowns and associated economic hardships, we are all suffering from Armageddon fatigue.

It is easy to become pessimistic in the face of the very real challenges we are grappling with. But history teaches us that periods of disruption and uncertainty go hand-in-hand with innovation, sparking a wealth of investment trends and opportunities.

The Covid-19 pandemic will force sectors to fast-forward changes which otherwise may have taken years to come about, and industries are likely to be either materially reformed or made redundant. As a consequence, the future will look very different to what we now imagine.

As Dr Peter Diamandis and Steven Kotler note in their book, “Abundance”, artificial intelligence, robotics, digital manufacturing, nanomaterials, synthetic biology and other rapidly developing technologies will enable us to make greater gains in the next two decades than we have made in the last two hundred years.

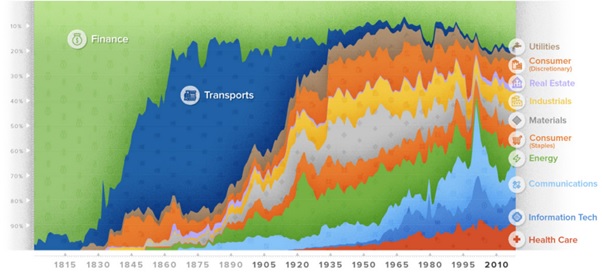

Consider, for instance, that in the 1900s, around two thirds of the Dow Jones Industrial Average was made up of railroad stocks. Today, a large portion of the US index is instead made up of technology and healthcare companies – companies whose roles have become even more prominent amidst new social distancing norms and the hunt for a vaccine, and whose agility, scalability and automation lead us into the future.

Chart 1: Visualising 200 years of U.S. Stock Market History – 20/20 Hindsight*

*Global Financial Data divides the stock market into twelve sectors. The 12 sectors include 11 sectors similar to the 11 sectors in the GICS, but adds a twelfth sector for Transportation stocks since these were historically important to the US, UK and other economies. The Communications sector includes not only Telecommunications stocks, but general communications such as Media and Publishing. The Real Estate sector is separated from the Financial Sector throughout its history.

Source: Visual Capitalist (2019): https://www.visualcapitalist.com/200-years-u-s-stock-market-sectors/

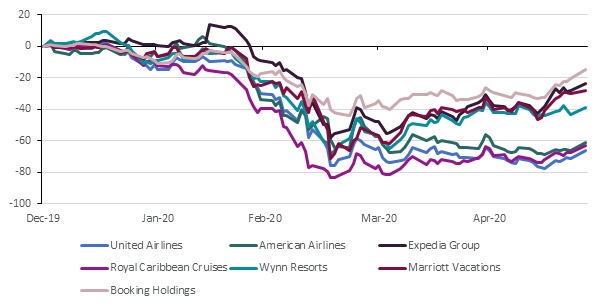

By contrast, it will come as no surprise that stocks in “BEACH” industries (booking, entertainment and live events, airlines, cruises and casinos, and hotels and resorts) have declined by more than $332 billion this year. (To put this in perspective, that figure is equivalent to the GDP of Israel.) The graph below illustrates just how far global travel and entertainment companies have fallen.

Chart 2: BEACH Stocks

Source: Cannon Asset Managers (2020)

Some have speculated that once a vaccine is available, pent-up demand and millions of would-be-travelers suffering from cabin fever will result in a V-shaped recovery. On the other hand, this may be hampered by significant job losses in these sectors and beyond, and just the threat of a global recession could hamper a recovery in consumer spending for some time to come. Depending on how optimistic or pessimistic you are, the shape and timing of a recovery is anyone’s guess.

Where to invest for the future?

While no one knows exactly what the future may hold, seeking to identify broad themes or mega-trends may offer investors a powerful advantage in decision making, as long-term investment success is all about having a view of the direction in which you think the world may be headed.

To this end, we see a future dominated by more people – as people live longer due to improvements in healthcare – and more machines. And given the changes brought on by Covid-19, it is especially worth considering the rapid digitisation of industries worldwide.

In terms of investment trends, digitisation of sectors is key. One local example of this, tucked away in the mid-cap sector of the JSE, is Altron. As people rush to work and socialise remotely, Altron’s security and digital transformation services will likely be much in demand for the foreseeable future. And their acquisition of Ubusha Technologies – the largest identity security company in Africa — in 2019 has proven prescient. The group is on an undemanding price multiple of 11 times, and with increased opportunities in a post Covid-19 world, this is an example of a great investment case and an attractive price.

The payments sector is also ripe for digitisation. For instance, Al Kelly, CEO of Visa, notes that 56 countries have lifted contactless payment limits this year to support social distancing measures. While ecommerce has traditionally comprised 14% of retail spending, we expect this to increase dramatically globally. And while Visa faces some headwinds due to a slowdown in economic activity, it is well positioned to capitalise on the digitisation of payments.

With the limelight on healthcare, these shares have generally enjoyed the benefits of share price appreciation, a streak of bullish earnings growth, and high price-earnings ratings. Boston Scientific, on the other hand, has not quite shared in the uplift. This is mainly due to the deferment of many elective procedures and surgeries as healthcare workers respond to a rise of critical patient care. These companies have collaborated with hospitals, universities and industry peers in an attempt to find innovative ways to meet the urgent demand for personal protective equipment (PPE) and ventilators. With an undemanding multiple of 14 times, a gross operating margin of 70% and ROE of 41.6%, Boston Scientific is a great investment opportunity, in the thick of the economic fog.

While speaking of structural drivers, there is at least one caveat that must be considered. Crucially, the sweet spot of investing remains unchanged: investing in good companies at great prices. For instance, Amazon is a great example of a company which will likely see increased, or even exponential growth. However, this is a widely acknowledged fact, and therefore the prospects are very much priced in.

Ultimately, then, the search for investment returns will be found in those companies that are able to benefit from the structural drivers that will shape tomorrow’s investment landscape, without paying for years of sometimes inflated and – pandemic or no pandemic – always uncertain, forecasted earnings.