The “Real Guide” to Index Tracking Products in South Africa – Unit Trusts vs Exchange Traded Products

Mike Brown.

Nerina Visser.

Some interest, comment and debate is being generated in South Africa by certain commentators trying to “protect” the position of old fashioned Unit Trust index tracking (passive) products versus the new generation passive Exchange Traded Products (ETPs) that are taking global markets by storm.

Since 2008, net flows of global investor money into ETPs have exceeded that of mutual funds (Unit Trusts) and, in fact, the assets under management by US based mutual funds (Unit Trusts) has contracted since 2007. By contrast, the assets under management by global ETP managers have increased from US$851 billion in 2007 to US$2850 billion in August 2015, i.e. the ETP industry has more than tripled in the last 7 years, whilst the mutual fund industry has contracted .

Why would this be happening if ETPs were less efficient and were inferior products to index tracking Unit Trusts? The truth of course, is the opposite. Exchange Traded Funds and other products are growing at the expense of the Unit Trust index trackers because they are cheaper to buy, to hold and to trade, easier to monitor and much more liquid and transparent than index tracking Unit Trusts. As Suze Orman, the US based financial guru often says “ETPs are the Unit Trusts of the 21st Century”.

So why are certain South African Unit Trust managers trying to fob off 50 year old (20th Century) Unit Trust technology and methods as superior to the 21st Century systems and technology used by Exchange Traded Products?

We will unpack the spurious nature of the defence case for old fashioned and outdated Unit Trust technology in this article.

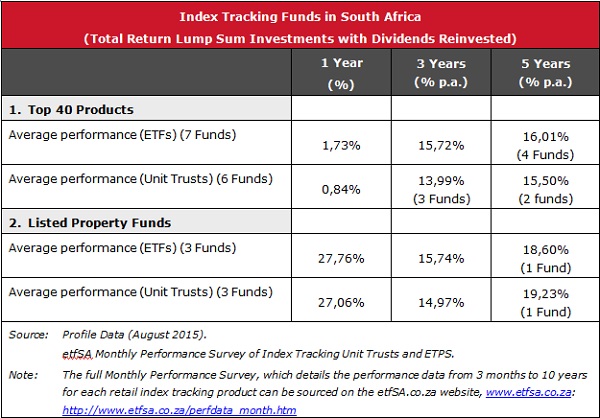

South African index tracking performance comparison

The underlying Table 1 shows the total return performance of equivalent index tracking Unit Trusts and ETPs that track the same benchmark index. A representative sample of index products, for instance, tracking the FTSE/JSE Top 40 index and the FTSE/JSE SAPY (listed Property) index can be compared.

There is a clear performance advantage for the index tracking ETPs, compared with equivalent index tracking Unit Trusts.

Table 1

The full Monthly Index Tracking Performance Survey also indicates that the consistency of investment performance of ETPs is superior to index tracking Unit Trusts.

Volatility

There is a far greater deviation in returns in index tracking Unit Trusts, tracking the same index, than is the case for ETPs. Why is this the case?

JSE Regulations require that any listed index tracker (which of course applies only to ETPs and not to unlisted Unit Trusts) must exactly replicate the index being tracked and must hold 100% physical backing for the securities in issue (in the case of all ETFs).

There is no such requirement for index tracking Unit Trusts, which in terms of their mandates, typically only “endeavour” to track an index. In the circumstances, nearly all Unit Trusts “cut corners” by only holding a portion of the shares making up an index. Quantitative technologies enable them to deliver a replication of the index by only holding a representative sample of the index (say only 20 shares out of the Top 40 indices for instance).

What this means in practice is that the Unit Trust tracker fund can show greater volatility in its returns, i.e. the standard deviation against the benchmark, is greater than for an ETF which exactly replicates the index. This indicates a greater degree of risk is carried by the Unit Trust tracker funds. Over time, lower volatility should deliver more consistent long-term performance, which makes ETPs a better choice for long-term investment purposes, i.e. in retirement funds, for instance.

Tracking Error

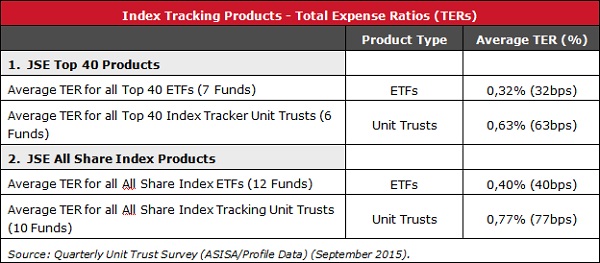

When tracking an index, the manager of the index tracking product, whether a Unit Trust or ETP, will incur some expenses in managing the product – paying asset management fees, audit costs, levies, and meeting staff overheads, etc. This cost is measured by the Total Expense Ratio (TER) of the product. Whilst TERs are not an exact measure, because they exclude brokerage, distribution and other “sales” charges, they do give a representative indication of the “manufacturing” costs of issuing investment products.

As can be seen from Table 2 below, index tracking ETPs have TERs about half the average for index tracking Unit Trusts. This must create a bigger potential for tracking error in Unit Trusts relative to ETPs.

Table 2

The access costs for Unit Trusts and ETPs

ETPs consistently show better investment performance than Unit Trusts in the index tracking Surveys as shown earlier in Table 1, mainly because of their lower costs.

However, Unit Trust companies sometimes try to tilt this cost argument in favour of their products by making somewhat dubious claims about the high cost of purchasing ETFs through the JSE or other stockmarkets. The Unit Trust managers argue that because you buy the Unit Trust “off market” or “over-the-counter”, there are no stockbrokerage fees to be paid so this is a cost saving for the investor.

However, there is a very important distinction between over-the-counter Unit Trust traded directly with the Unit Trust manager, i.e. in the primary market and ETFs, which trade through the JSE, in the secondary market.

Primary market transactions

Unit Trusts can only trade in the primary market. What this means is that every day the Unit Trust manager must create or redeem participatory units according to the number of investors who wish to buy or sell the Unit Trust units. They cannot offset the sales against the purchases.

So every day, the Unit Trust manager has go out and buy the JSE shares that make up the index, pay stockbrokerage fees, CSDP custodian fees, pay the bid and offer spreads, as well as Securities Transfer Tax (STT) for each security. Only once the Unit Trust manager has created such new units, can these are then be sold to the investor by the Unit Trust manager at the net asset value (NAV) of the Fund.

But the NAV of the Unit Trust Fund will now include the cost of daily creation and redemption of units. This cost is not reflected in the TER of the Fund, as TERs do not have to include brokerage and transaction charges in their calculation. The contention by Unit Trust managers that investors do not pay brokerage charges for their units is therefore incorrect. These fees are paid upfront in creating units, often on a daily basis.

Secondary market transactions

The ETF/ETN securities that trade on the JSE have already been created (in the primary market) and they now trade on the secondary market. So the investor typically does not have to pick up the costs of creating the ETP securities, unlike the Unit Trust investor.

As primary creations happen very seldom for ETPs, compared with Unit Trusts where new units are created on a daily basis, the “manufacturing” costs of the ETP securities become almost meaningless. For instance, in only four days of this year (to end November, i.e. some 330 days), have there been either creations or redemptions of the Satrix 40 and DBX World ETFs which are two of the most popular ETFs on the JSE. Accordingly, the “manufacturing” charge of creating an ETP security becomes a meaningless figure in the secondary market where such units trade over and over again. However, the manufacturing charge for Unit Trusts, which takes place daily, is a much more significant cost.

Securities transfer tax (STT)

Of particular impact is the Securities Transfer Tax (STT) of 0,25% paid by the Unit Trust manager, for each JSE security they purchase. As daily creations can occur, this 25bps tax becomes a significant factor in the NAV of the Unit Trust.

For the ETP, the STT was paid on creation, which occurs very seldom, after which the ETP trades on the JSE without any further STT being paid by the investor. In effect, the initial STT payment of 0,25% is not a factor that has to be considered by the investor in an ETP which trades a multiple number of times on the JSE.

In fact, if the investor can purchase an ETP on the JSE at a brokerage rate lower than 0,25% (25bps), ETPs are much cheaper to buy than equivalent Unit Trusts.

Stockbrokerage rates

Some Unit Trust managers have a major focus on the stockbrokerage rates incurred by investors. In practice, most ETP investors use investment platforms, like the Satrix Investment Plan or etfSA Investor Plan, which charge stockbroking rates of 0,08% (8 bps), and “bulk” all the JSE Settlement/CSDP fees, etc. so they are only a few cents per trade.

In practice, if you can purchase an ETP at a stockbrokerage rate lower than 25bps, including settlement fees, ETPs have lower relative trading costs to Unit Trusts because of the STT factor.

Spreads

All JSE listed securities trade at price spreads between bid and offer prices. There are always investors who want to sell at above the current market price, or to buy at below the market price. This creates the spread and ETF securities have exactly the same bid and offer spreads as any other shares on the JSE.

The Unit Trust manager, when they are creating participating units, will have to pay this bid and offer spread on each JSE security they transact in.

However, where ETPs differ from normal shares, is that the JSE Listing Requirements require market makers to be appointed for ETPs which is not the case with other equities. The market maker will make a price at the fair value of the ETP, which is the daily published NAV of the ETP. So the market maker effectively eliminates the spread for any savvy investor, or their stockbroker, who does not want to pay the bid and offer spread on their investments.

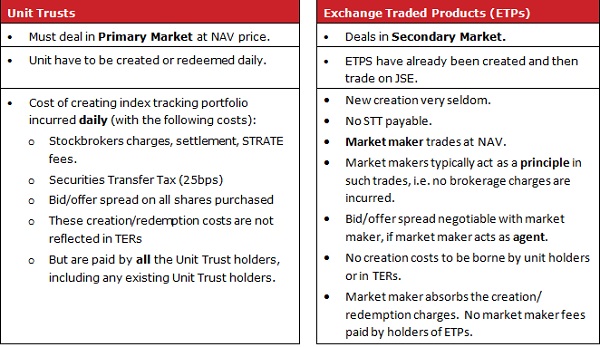

Table 3 summarises the creation/redemption process for index tracking Unit Trusts versus index tracking ETPs.

Market makers

This is an often misunderstood issue. There are market makers for both Unit Trusts and ETPs. In the case of non-listed over-the-counter Unit Trusts, the primary issuer of the Unit Trust has to make a market in the Unit Trust at the daily NAV of the Unit Trust, as all trades have to go through the primary market.

In the case of an ETP, nearly all the trades in the ETP takes place, not with the primary issuer of the ETP, but in the secondary market. JSE regulations for ETPs require that a market maker be appointed by the ETP issuer. The market maker is required to make prices in the ETP at all times, unless there are abnormal market conditions. In practice, the other market participants and investors look to the market maker to make a price at the NAV of the ETP, which, like a Unit Trust, is also published on a daily basis.

There are some distinctive features of the two types of market makers, for Unit Trusts and for ETPs.

• ETP market makers make prices on a continuous basis as long as the stock exchange is trading.

• A Unit Trust prices once a day and that price holds for the following day.

• Unit Trust market makers typically have to hold some cash in order to facilitate their market making. This “cash drag” means they cannot exactly replicate the index which can reduce investment performance as the return on cash is often lower than the return on index constituents. In addition, the investors in the Unit Trust have to pick up the cost of the market making as this is a cost incurred in the Unit Trust management (Manco) company.

• ETP market makers are appointed externally and independently of the ETP Manco structure. So the market making costs are picked up by the market maker themselves and not in the ETP structure.

Also, there is no requirement to hold any cash in the ETP index tracking portfolio, so an index tracking ETP will exactly replicate the index constituents, without any negative impact of a cash drag.

• The ETP market maker has an additional factor to consider. Unit Trusts can only be cash settled, so if you sell your Unit Trust, you will only be paid out in cash.

However, ETPs can be settled “in specie”, i.e. you can exchange physical baskets of index constituent securities for the ETP tracking the index, by either delivering such baskets or by taking delivery of baskets. It follows then, that if the cost of purchasing an index basket and delivering it to the market maker, who trades at the NAV price, is sufficient to create a profit to the investor, they will take up this arbitrage opportunity.

So the market maker must ensure that the “double”, i.e. the price he quotes on the bid-offer spread, if applicable, is sufficiently tight to prevent such arbitrage opportunities. In essence, this creates a put or call on the ETP market maker, which is absent for the market maker in Unit Trusts. This creates higher efficiency and greater discipline in pricing ETPs relative to Unit Trusts.

Investment platforms and LISPS

Some Unit Trust managers give the impression that Unit Trusts can be bought or sold without any costs. They intimate that you can deal direct with the issuers of such products (Mancos) and they will create or redeem units, etc. for you without any costs or fees. This, of course, is cloud cuckoo land for most investors.

A Manco is a Collective Investment Scheme that can issue Collective Investments, but does not have the license to trade in, give advice, or to provide distribution services on its products. For that it needs another license, an FSP I, II or Category III license. If it wishes to offer full administrative services, a Category III FSP license, with very onerous capital adequacy and other requirements, is needed. This is a cost to the investor.

Even if the Unit Trust company runs its own “in-house” administration or linked service provider (LISP) company, this is a profit centre for the company and it must at least recover its costs. Running LISPs is not cheap. So any investor who believes that a LISP will collect 12 debit orders a year (possibly split the debit order into a number of different Unit Trusts), reinvest dividends each quarter, send out statements, tax certificates, etc. and do this for nothing, has to think again. If the investor goes through a financial advisor, or any other distribution channel, the LISP (administrator) will pay commission and fees to these people, and recover the costs from the clients’ Unit Trust investment.

Accordingly, you have to pay access or distribution fees to buy or sell Unit Trusts, except in exceptional cases, where an institution or very large investor, might deal direct with the Manco in the primary market.

For an investor in an Exchange Traded Product, the access to ETFs/ETNs is through:

• the stockmarket (through a stockbroker or online trading portal);

• through a LISP;

• or through Investment Platforms (like Satrix Investor Plan, etfSA.co.za Investor Plan), which operate effectively as LISPs, by using a Category III administrator as part of the Plan.

Or a big investor could go straight to the ETP issuing company or Manco and deal direct in the primary market, just the same as a Unit Trust, but these are exceptional transactions and occur relatively seldom.

In the real world, investment platforms are a reality for both Unit Trusts and ETPs for the great majority of investors. The costs of an investment platform to access units, either in a passive Unit Trust or an ETP, need to be taken into account for the great majority of investors.

Appendix: Summary of features of Unit Trust and ETP index tracking structures.

Terms and conditions: Redistribution, reproduction, the resale or transmission to any third party of the contents of this article and this website, whether by email, newsletter, internet or website, is only possible with the written permission of etfSA.co.za. etfSA.co.za, its sponsors, administrators, contributors and product providers disclaim any liability for any loss, damage, or expense that might occur from the use of or reliance on the data and services provided through this website. etfSA.co.za is the registered trading name of M F Brown, an authorised Financial Services Provider (FSP No 39217). etfSA.co.za is licensed to provide financial services in the following categories: Collective Investment Schemes; Shares and Securities; Retail Pension Fund Benefits; Short-Term deposits; and Friendly Society Benefits. Professional Indemnity Insurance is maintained. etfSA.co.za®, and etfSA The Home of Exchange Traded Funds® are registered trademarks in the Republic of South Africa.

Limited variety available in Index Tracking Unit Trusts

There is a very limited range of index tracking Unit Trusts available – most of them are of the “vanilla” market cap weighted, variety. By contrast, ETPs cover all asset classes, different investment styles (including so-called “smart” indexation), global geographic diversification, and access to physical commodities and currencies which are not available as Unit Trusts. This makes ETPs significantly more suitable for constructing well-diversified, balanced investment portfolios, using the full benefit that index tracking offers.

Terms and conditions: Redistribution, reproduction, the resale or transmission to any third party of the contents of this article and this website, whether by email, newsletter, internet or website, is only possible with the written permission of etfSA.co.za. etfSA.co.za, its sponsors, administrators, contributors and product providers disclaim any liability for any loss, damage, or expense that might occur from the use of or reliance on the data and services provided through this website. etfSA.co.za is the registered trading name of M F Brown, an authorised Financial Services Provider (FSP No 39217). etfSA.co.za is licensed to provide financial services in the following categories: Collective Investment Schemes; Shares and Securities; Retail Pension Fund Benefits; Short-Term deposits; and Friendly Society Benefits. Professional Indemnity Insurance is maintained. etfSA.co.za®, and etfSA The Home of Exchange Traded Funds® are registered trademarks in the Republic of South Africa.