The extraordinary outperformance of Index Tracking Exchange Traded Funds (ETFs)

Mike Brown, Managing Director of etfSA.co.za.

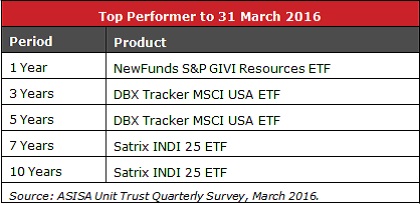

The best performing Collective Investment Schemes (unit trusts/ETFs) for the period ended 31st March 2016 have been passive ETFs and not actively managed unit trusts.

As the table below shows, for periods of 1 year, 3 years, 5 years, 7 years and 10 years, the number one investment performance has been provided by passively managed ETFs and not by active managers.

What has happened to all the active asset managers, with all their fancy technology and marketing propaganda, who promise to outperform the index?.

Basic index trackers that provide the average return of the market, or market sector being tracked, comprehensively and consistently outperform the high cost complex and high risk actively managed unit trusts.

Furthermore, the global surveys by Standard & Poors (S&P), clearly indicate that, across nearly all stockmarkets, 80% or so of active managers cannot outperform representative benchmarks.

To what can this systemic outperformance by index tracking ETFs be attributed?

Costs

The average total expense ratio (TER) of ETFs, tracking SA domestic indices is 0,33% per annum (33bps). Index tracking unit trusts in South Africa have average TERs of 0,76% (76bps), double that of ETFs. Actively managed unit trusts, have far higher TERs, double those of index tracking unit trusts. This “cash drag” is hard to overcome in accounting for total return investment performance.

Furthermore, ETFs total expense ratios almost always include all costs in the product, including brokerage and settlement fees, reinvestment of dividends, accounting for corporate actions, etc.

This is typically not the case with active managers, where brokerage, creation/redemption charges, rebalancing fees, etc. are not reflected in TERs, but will appear in the net asset value (NAV) prices of the unit trust. This explains why unit trust performances, even if they mirror the indices, are often worse than their TER levels.

The undisclosed costs of many actively manged products is proving to be a bigger and bigger obstacle for the issuers of these products, particularly as index tracking products become more efficient and have greater economies of scale, which tends to lower their costs even further. As index tracking ETFs become more popular and more in demand as an investment vehicle, the active managers are required to justify their high fees and underperformance.

Indexation efficiency

As indexation takes over from active management as the financial investment strategy in most developed markets, the construction and calculation of indices has become more efficient. Current indices are:

• Much more representative of the asset class, sector or style they are measuring.

• Have various filters and systems, built-in to their construction to reduce concentration levels in indices, whereby only a small number of shares dominate an index.

• Multi factors, such as free float, liquidity, double counting for secondary listings, etc. are all taken into account in designing modern indices.

• Corporate actions are far more efficiently handled in present day index tracking by calculation agents, whereas some years ago, these would invariably lead to tracking error.

• Index constituents are amended more quickly to reflect changing market conditions.

The index tracking companies worldwide are consolidating thereby providing greater economies of scale and lowering their costs of providing indices. Technology is now driving index construction efficiencies in a highly competitive market. In South Africa, S&P and MSCI, who are the major global providers of indices, are now actively competing with FTSE/JSE in the local market.

Smart indexation

Many indices are now no longer market capitalisation indices, but use specific criteria or objectives, rather than purely size, in their construction. Often called “smart beta”, such indices are formula driven and take analytical approaches to construct indices, with specific criteria in mind to provide a particular investment solution.

The NewFunds S&P GIVI Resources ETF, which was the top performing fund in South Africa over the past 6 months and 12 months, is a good example. This uses an intrinsic valuation formula to select companies in the resources index, based on fundamental criteria, rather than pure price and size (which is the case with market cap indices).

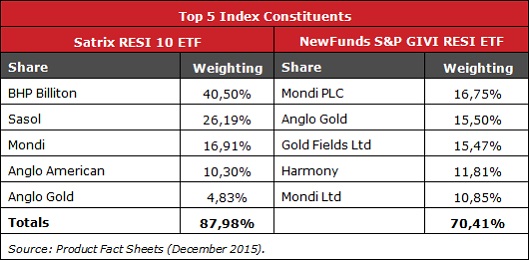

To give an example of how a smart indexation strategy can affect the exposure to a particular asset class, the top 5 shares and their weightings in the Satrix RESI 10 ETF and the NewFunds S&P GIVI Resource ETF are compared in the table below.

Both these products track the JSE resources sector. However, the market capitalisation weighted Satrix RESI ETF has the bulk of its investment in Mining Houses and Sasol and is highly concentrated, whereas the NewFunds S&P GIVI Resources has its focus on gold shares and Mondi with much less concentration.

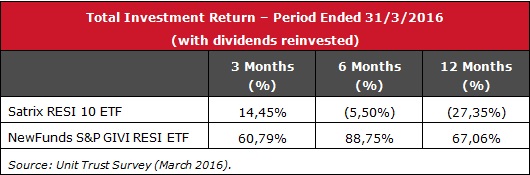

The difference in investment performance returns over the past 3, 6 and 12 months has been marked.

Using smart indexation technology has enabled the smart beta NewFunds S&P GIVI RESI ETF to substantially outperform, not only the market cap Satrix RESI ETF, but also all the unit trusts focusing on the same resources sector.

Smart beta, with its “hands off” formula driven technology, using the best practice developed globally, can be an extremely competitive investment tool, which active managers have yet to counter.

Terms and conditions: Redistribution, reproduction, the resale or transmission to any third party of the contents of this article and this website, whether by email, newsletter, internet or website, is only possible with the written permission of etfSA.co.za. etfSA.co.za, its sponsors, administrators, contributors and product providers disclaim any liability for any loss, damage, or expense that might occur from the use of or reliance on the data and services provided through this website. etfSA.co.za is the registered trading name of M F Brown, an authorised Financial Services Provider (FSP No 39217). etfSA.co.za is licensed to provide financial services in the following categories: Collective Investment Schemes; Shares and Securities; Retail Pension Fund Benefits; Short-Term deposits; Long-Term Insurance, Category C; and Friendly Society Benefits. Professional Indemnity Insurance is maintained. etfSA.co.za®, and etfSA The Home of Exchange Traded Funds® are registered trademarks in the Republic of South Africa

")