State of the SA ETP Industry – Half year review (January to June 2017)

Mike Brown, Managing Director of etfSA.co.za.

The total market capitalisation of all ETFs/ETNs, listed on the JSE, as at 30 June 2017, amounted to R79,7 billion, an increase of 7,5% on the total market capitalisation at the end of 2016.

Market capitalisation

Following rapid growth in the South African ETP industry from 2008 to 2013, the total size of the industry has stayed fairly constant for the past 3½ years. This is rather a reflection of the stagnation of the value of the local markets, with the JSE All Share Index and other indices failing to grow at all over this period, rather than a lack of activity in the ETF industry.

Shares in issue and capital raised

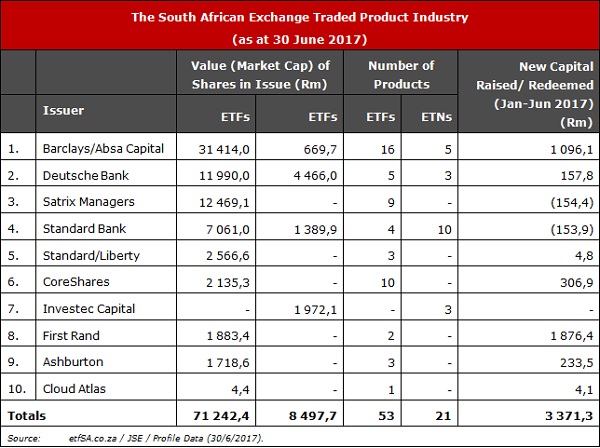

A total of R3 371 million (R3,3 billion) new capital was raised by the ETP industry, from new listings on the JSE, during the first 6 months of 2017. Whilst most trade in ETFs/ETNs occurs in existing securities that are already listed and traded on the stockmarket, from time to time, the ETF/ETN management companies have to issue or redeem new shares to meet changes in market supply and demand conditions. This is to ensure that the exchange traded product, trades at the net asset value of its constituent index tracking portfolios and is not affected by excess supply or demand for such products.

The bulk of new capital raised in the first half of 2017, came from the new listing of Krugerrand and US Dollar Custodian Certificate ETFs by First National Bank (R1 876 million), plus new issues of commodity ETFs by NewGold (R1 096 million).

The Table below shows the number of ETFs in issue and total market capitalisation for each issuer of ETPs in South Africa.

During this half year period, BNP Paribas decided to delist their BNP GURU ETNs on the JSE, reducing the overall market cap of the industry by some R600 million and by 4 products.

Market returns in the first half of 2017

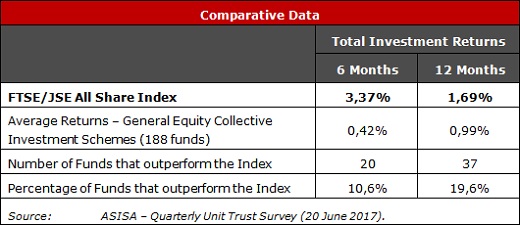

The South African equity markets have shown a small improvement over the first six months of 2017, although most indices still continue to languish below the all-time highs achieved in late-2014. The FTSE/JSE All Share Index, for instance, rose by 3,37% in the past 6 months, but by only 1,69% over the past year.

Certain ETFs/ETNs, have, however, quite comfortably outperformed the market benchmark, indicating, as always, that the choice of indices can be critical in investment performance.

Comparative investment performance

In current difficult conditions for equity markets, given the political, economic and financial uncertainty in South Africa, it is sometimes suggested that active investment managers, who try to beat the index returns, are a better proposition than buying the index, i.e. investing in an index tracking ETF.

It would appear that the majority of active managers cannot outperform the general returns in the SA equity market, even in poor market conditions. For the past 6 months (89,3%) and 12 months (80,4%) of active managers have failed to match the index returns. The hypothesis that active managers fare better in declining markets remains a fallacy.

")