80 percent of active investment managers continue to underperform their benchmark index

Mike Brown, Managing Director of etfSA.co.za.

Latest data from the end-March 2018 Quarterly Collective Investment Schemes Performance Survey, shows that, on average, 80% or more of general equity unit trusts and other collective investment schemes (ETFs), fail to produce total investment returns above the FTSE/JSE All Share Index.

Furthermore, of the funds that did outperform the index, increasingly such index beating returns were produced by index tracking products, rather than typical active stock selecting asset managers.

The 80% failure phenomenon

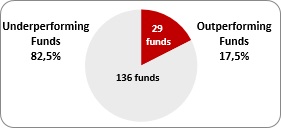

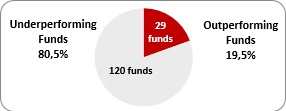

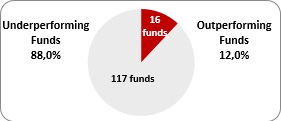

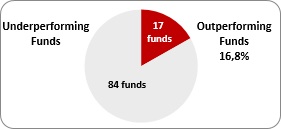

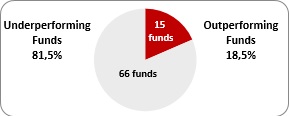

The composite graphics alongside shows that, for periods ranging from 1 to 10 years, 80% plus of the actively managed general equity collective investment schemes, that make up the Survey, failed to produce returns in excess of the total returns of the JSE All Share Index. The number of collective investment funds that are included in the general equity sector of the Survey, range from 66 funds on 10 years to 165 funds for the one-year period. In other words, the sample is very representative.

Unit Trust Survey – March 2018

One Year (165 Funds) JSE All Share Index 9,60%

Two Years (149 Funds) JSE All Share Index 6,01%

Three Years JSE All Share Index 5,05%

Five Years JSE All Share Index 10,02%

Seven Years JSE All Share Index 11,35%

Ten Years JSE All Share Index 9,67%

The numbers show a remarkable consistency in that less than 20% of the active managers in the Survey can outperform their representative benchmark index over the various time periods surveyed, from 1 to 10 years.

The one exception is the 10-year performance survey, which indicates that 71,2% of active managers underperformed the index (i.e. 28,8% managed to produce outperformance). However, as the period surveyed increases in duration, the issue of “survivorship” enters into consideration. Over a 10-year period, some 50% or so of collective investment schemes that have not been successful will close, or merge with other funds. So, the “survivorship bias” tends to distort the picture, the longer the time period surveyed.

The irrefutable conclusion remains, however, that the majority of active collective investment schemes do not deliver alpha investment returns, i.e. in excess of index-based returns.

The increasing alpha returns provided by Index Tracking Products

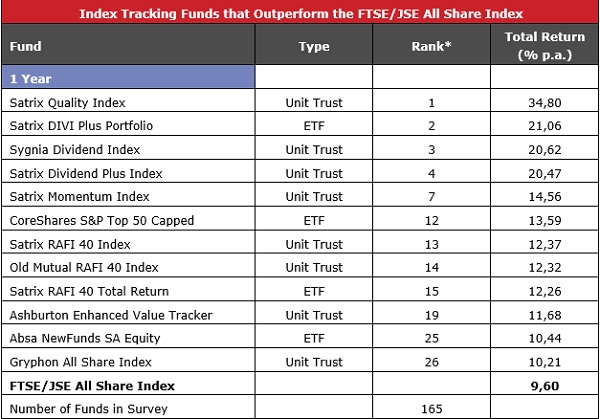

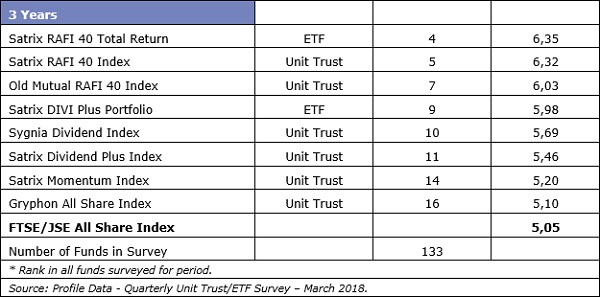

The table below shows that for the periods of 1 year and 3 years, a significant portion of the collective investment schemes that produced investment returns in excess of the index, were index tracking funds, either ETFs or unit trusts. As the number of index tracking products that are available for periods of 5 years or longer is limited, this statistical survey has been confined to 1 and 3 year periods.

The numbers indicate that a significant portion – 12 out of 29 funds for one year and 8 out of 16 funds for the 3 year period, that produce All Share index beating investment returns – are in fact index tracking funds.

This is a somewhat surprising result as you would expect an index tracking fund to provide market average performance – the index, of course, is the average of the market returns. This anomaly is explained, inter alia, by the following:

• Although the Quarterly Performance Survey includes many index tracking funds under the general equity classification sector of the Survey, these products often track indices that differ from the All Share index.

• The majority of index outperforming tracker funds are in fact “smart beta” products, where the objective is to track factor based indices, which look to specifically provide market beating returns or to reduce risk through specific focus on smart indices. Such indices do not replicate market capitalisation weighted returns, but look to take into account specific investment factors, such as volatility, value, momentum, etc.

• The more successful smart beta products for the relatively short time periods surveyed (1-3 years) have been using dividends, momentum or value as the target for stock selection rather than risk containment factors.