What does a Trump win mean for the energy transition?

Mark Lacey

The election outcome has added another layer of potential short-term pain for the energy transition sector. However, the long-term need to transition our energy system away from fossil fuels has not changed and we continue to see a robust growth outlook for companies across the universe even in a scenario where US climate policy reversals play out to their most extreme.

The election result does not change the fact that renewable energy solutions have become increasingly competitive with fossil fuels, that electric vehicles are becoming ever more compelling with respect to their capabilities and cost, or that energy storage solutions have now become bankable.

It will not change the fact that we are seeing new pockets of electricity demand globally for the first time in decades, particularly from AI-related data centre expansion, but also increased heating and cooling needs too and it will also not change the fact that many major corporates want their operations to be 100% fossil fuel free in the very near future.

It will not change the fact that energy security remains a concern globally, and that renewable power is at least part of that solution, or that many economies globally are rapidly accelerating their deployment of renewables, including India and the Middle East, with growth that can help offset any potential weakness in the US.

And it will not change the fact that this year will mark the first year that global average temperatures will end up more than 1.5C above pre-industrial levels, and that longer-term climate ambition globally must still be addressed.

We acknowledge that if certain policy actions in the US are taken under the new administration – which are by no means guaranteed given the significant investment and jobs the renewable energy industry creates within the US – then we could see lower US growth short-term and further potential earnings disruptions. We also accept that the outcome of other elections globally this year have highlighted that other issues such as defence and inflation have perhaps become priorities over decarbonisation short-term.

But the longer-term, and more powerful forces of investment and technology adoption should not be forgotten, as they will be what ultimately drives the value of sustainable energy companies longer-term. Politics and sentiment will always experience cycles, but industries and businesses with competitive products can still adapt and thrive. Indeed, let us not forget that US wind and solar installations increased 50% between 2016 and 2020 when Donald Trump was last in office, with global renewable installations more than doubling over the same time.

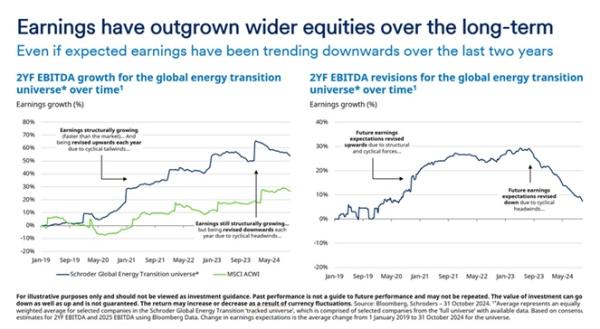

Stepping back, the bigger picture for the sector is still that: long-term growth expectations for the sector remain robust, and that even with potential US market disruption short-term, we are approaching the bottom of the capital and earnings cycle for several key energy markets and stocks. Energy transition equities have outgrown the wider market from an earnings perspective over the last five years, and they are forecast to continue to do so over the next few years as well. With through-cycle earnings growth the best indicator of long-term investment returns, the fundamental set up still looks robust from here.

Click here to read more...