The SA equity market: Whereto from here?

The end of the US government shutdown has heralded in an interesting time for equities in emerging markets such as South Africa. Given that markets have begun to take into account a possible end to the Federal Reserve’s accommodating policy stance, what can investors expect? Mark Phillips, an analyst at Sanlam Multi Manager International (SMMI), a division of Sanlam Investments, unpacks the outlook for the South African equity market.

"Many questions have been raised around the ability of emerging market economies to grow independently of developed markets. There is a misconception that emerging markets need the guidance of developed markets to handle their economies. However, since the start of the global financial crisis of 2008, emerging market countries have generally not only survived, but prospered,” Phillips says.

He says financial markets are conscious of vulnerabilities in emerging markets, which will have an impact on future growth. "However, we believe emerging market countries will continue to experience dramatic increases in incomes at national and individual levels as investment in productivity-enhancing technology continues.

The near-term outlook is likely to remain clouded by policy uncertainty, and emerging market economies with large current account deficits remain the most vulnerable to any shift in global financing conditions.

Phillips says the outlook for the South African economy has become less rosy in recent months. Mediocre growth is accentuated by labour unrest, high unemployment and South Africa's twin deficits. Despite this, the local equity market has been a strong performer, delivering 26.97% for the 12 months ending September 2013 and outperforming many major developed and emerging markets. "While the South African market has in the past benefited from flows to emerging markets, we expect investors will become increasingly choosy about where they invest, however.”

The tapering debate will continue to be a worry for emerging markets, Phillips says. "Given the possibility of an emerging market capital flight scenario, South Africa is definitely at risk. Fed tapering has now been pushed out to the first quarter of 2014, assuming an improved outlook on the US recovery. Global interest rates are expected to remain low over the short term, and hence risky assets remain attractive. But we believe the risks to investing in equities are increasing and it is therefore critical to consider which risky assets to be invested in.”

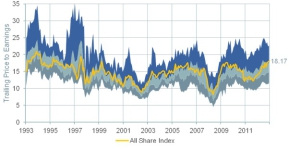

As at the end of September 2013, JSE valuations are riding at a multiple of around 18 times trailing corporate earnings, which is expensive territory for the South African market. "The upward trend in the overall market's price to earnings ratio over the last 24 months has led to the general perception that our market is expensive. However, only a few companies have driven the markets multiple to these stretched levels.

The graph illustrates the trailing price to earnings (PE) ratio of the market and the dispersion between the 20th percentile and 80th percentile company over time. Over the last 18 to 24 months, the PE multiples for already expensive companies have increased faster than those of companies with cheaper PE multiples. Source: Inet, Sanlam Multi Manager International. The area graph takes into account companies with a market capitalisation greater than R6 billion and is not a constituent of J253.

"High quality companies have proven popular in uncertain times, as equity investors are willing to pay a ‘safety' premium to secure the more certain income flows from these companies. As the price to earnings ratios of these companies have crept up, the dispersion in the ratios between expensive and cheap shares has widened. Many quality companies are now expensive relative to their own history and the overall market. By comparison, the valuation of the cheapest quintile of the equity market is still cheap relative to the market.”

Phillips says the sustained rise in price to earnings ratios of already expensive companies may be one factor contributing to the continued underperformance of some equity managers with a more value-oriented bias.

"The real question is: what is next for South African equities? If the global economic environment remains uncertain, investors may be content to continue paying a safety premium for investing in high quality companies with a robust strategy and proven track record. However, in an improving global environment, investors may no longer be keen to pay the safety premium, least of all in a developing market with muted growth outlook,” Phillips concludes.