That which fools you

Aadil Omar

“Beating the market” in investing could be considered an endeavour prone to the trickery of randomness.

If we simplify the task at a portfolio level, beating the market averages entails some combination of:

- Owning more of the stocks that have beaten the market – the winners;

- Owning less (or fewer) of the stocks that have underperformed the market – the losers.

This is easily understood, but how does one construct a portfolio with a higher probability of winning than losing?

Raw odds

What are the chances of selecting a winner in a portfolio?

This requires more context to be useful but to illustrate the point, let’s consider a simplified, probabilistic game where the odds of success are known ahead of time – roulette. Let’s assume we play the double-or-nothing bet – red or black. The odds of winning on any spin of the wheel are around 48% , so close to even against the house. These odds are not drastically out of the player’s favour, but that changes quickly depending on the number of spins a player is willing to bet on.

The best odds (48% chance of winning) are achieved on the very first spin of the wheel. The odds of success then drop precipitously as a player continues to wager, such that by the fourth successive spin of the wheel the odds of maintaining a winning streak drop to only 5%. By the sixth spin, they’re barely 1%

Turning now to the raw odds of blindly selecting a winning stock, there are a few nuances to consider, with time frame being the most pertinent.

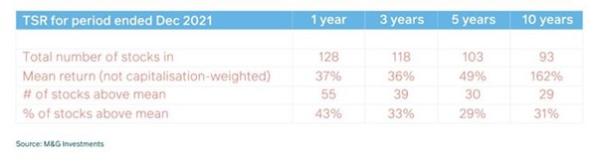

On any given day, the odds of holding a stock that will beat the market range from 20% to 55%. This is a wide range since there are an untold number of forces acting on the price of a stock in the short term. As we lengthen the time horizon, observations become steadier and more intuitive. The table below summarises the FTSE/JSE All Share Index over the last decade based on publicly available data, showing total share returns inclusive of dividends and share price performance (TSR) for ALSI constituents for which we had a complete dataset (after removing listings/de-listings, etc).

Analysing JSE-listed stock outperformance over time

The results were unsurprising and the general trend was intuitive; however we noted two key observations:

- Outperformers reduce as the holding period lengthens;

- Returns are more dispersed as the time horizon increases

Randomness ahead, ignore at your peril

So, at the casino, how does the house manage to win around half of the time?

The answer lies partly in how they structure the game (the house has the edge) and partly in how each participant is permitted to play (the house can extract the edge at the players’ expense). The house draws its edge because there is no way of predicting the outcome of any spin of the wheel – it’s 50/50.

The casino exploits its edge of around 1.5-2.5% by playing against multiple players, spread over many tables across numerous locations. With so many thousands of spins of the wheel and the casino’s inherent, albeit marginal, edge, a steady stream of rather predictable profitability can be extracted, in aggregate. To win at these sorts of games, both an edge and the ability to exploit the edge is required – that is what the house has that the individual player does not.

Most day traders on the stock exchange lose money because the nature of the game they’re playing is closer to roulette. Unlike a casino where the edge is ever-present, the challenge most day traders face is not knowing when their edge will show up. They must keep trying their luck until a winning streak lands, while the cost of trial and error adds up.

Edge toward non-random

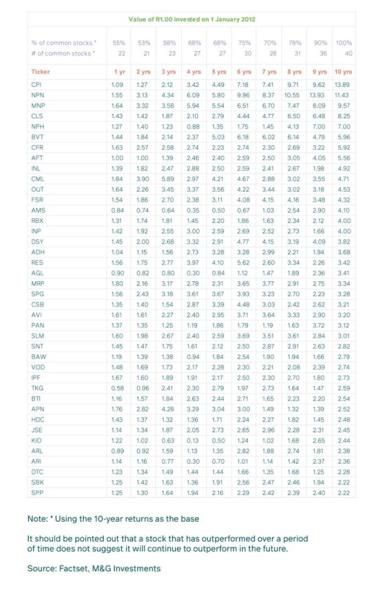

Persistence is apparent in shareholder returns through time not because the winning stocks of yesterday are the winning stocks of tomorrow, but because winning streaks in the winning stocks carry those winners for a long time. The table below tracks the TSR of the top 40 best-performing ALSI stocks over the decade ending December 2021. Included in the figure is a measure of persistence (# of common stocks; % of common stocks). This tracks the number (and percentage of the 40 stocks) that are common to the period in question and the 10- year period. For example, of the 40 top-returning stocks over the 10-year time period, 27 of them were among the top 40 best-performing stocks over five years. There are two noteworthy observations:

- Over shorter time horizons (1-3 years), persistence scores seem closer to random, and it is only over the medium term that a degree of persistence can be perceived.

- Winning streaks tend to carry the best performers as long-term winners even though there may be periods of extended underperformance.

Persistence of stock outperformance improves over the medium term

Removing elements of randomness is how one develops an edge in probabilistic games. By removing the noise of random occurrences, much of which serve to cancel each other out over longer time horizons, we can focus on those elements that lead to outperformance including a company’s ability to earn excess returns over a prolonged period of time and reinvest at rates that maintain those high returns.

Staying lucid in the face of the siren song of randomness is tricky at the best of times, but the line between being fooled and being killed is thin indeed.