SuperDogs wagging ahead

Doug Turvey, Private Client Portfolio Manager at Cannon Asset Managers, takes a closer look at the unusual SuperDogs portfolio.

For equity investors, 2014 was anything but smooth sailing on the local bourse. Rather, the year was characterised by a significant increase in volatility, particularity towards the latter part of the year. Specifically, investor sentiment turned sharply against resources stocks on the back of fears of a possible slowdown in Chinese consumption, a general oversupply of iron ore and a collapse in the oil price. Overall, cheap shares became cheaper – particularly among resources counters – and large multinational industrial and financial stocks continued to be in vogue, causing a huge divergence in performance among the major sectors.

The All Share Index (ALSI) delivered a 10.9% total return for the year, slightly higher than the 10.2% delivered by the bond index (ALBI). Whilst the equity index performance was below the long-term average of 18% p.a. over the last decade, this stemmed from sharply divergent returns within the sectors rather than from the delivery of below-average performance across the sectors. Financials and industrials returned an impressive 27.8% and 17.2%, respectively. By contrast, resources fell 15.0% for the year, which weighed heavily on the overall market return.

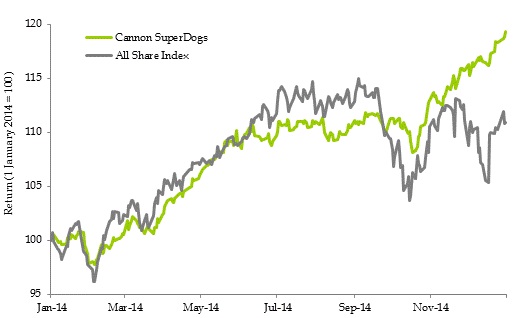

Chart 1: Performance of SuperDogs and the All Share Index (2014)

Managed by Cannon Asset Managers’ CIO, Adrian Saville, SuperDogs returned an impressive 20.5% in 2014, nearly twice that of the ALSI. It appeared to be a close race throughout the year, however, in fine greyhound style, SuperDogs sprinted ahead in the latter part of the year, returning 3.2% in December alone which compares very favourably to the negative 0.2% from the ALSI.

In existence since 2009, the SuperDogs strategy is supported by evidence from global markets which demonstrates that, over time, a carefully-constructed deep-value strategy, that is managed using a repeatable process, can be expected to outperform the market by a healthy margin. The mechanics behind this investment strategy are simple: human emotions – such as greed and fear – and behavioural biases – such as myopia or the belief that “this time is different” – cause assets to become mispriced. As emotions subside and biases reverse, assets become more efficiently (or accurately) priced. By the application of a disciplined philosophy and consistent process, the SuperDogs strategy is equipped to capture investments that are excessively cheap and compellingly priced which means the investment odds become stacked in an investor’s favour.

SuperDogs invests in greatly unloved and/or under-researched companies listed on the South African equity market. The companies in which SuperDogs is invested also exhibit evidence of sustainability, enhancing the likelihood of superior results. The term “dogs” is a function of near-term market sentiment and mispricing, and not a comment on the company itself. Calgro M3 and Santova, which delivered exceptional returns in 2014, are pure breed examples of companies fit for SuperDogs. Calgro M3 is a low-cost residential developer that has been shunned by investors averse to the construction sector. At the start of 2014, Calgro M3 was trading on a price earnings multiple (P:E) below 8x and was priced at a 40% discount to net asset value, most of which is land, with a return on equity in excess of 15%. The share had all the right qualities and characteristics to outperform sentiment and the market. Similarly, Santova Logistics, a small-cap logistics company traded on a P:E below 5x at the start of 2014. The company delivers sustainable earnings growth and benefits from its competitive advantages of industry knowledge, information technology and systems. These two companies went on to return 134% and 147%, respectively for 2014, making them true SuperDogs.

With no resources exposure and a large weight in small-cap shares, SuperDogs is well positioned to continue its performance. Trading below its historic average valuation, the small-cap index is attractive in a market where most sectors and many large companies are particularly expensive. Additionally, with the oil price plunge, local consumer price inflation is expected to subside as fuel prices decrease and the spill-over effects flow into the economy resulting in huge cost savings, especially for smaller companies that are sensitive to the local economy.

The stocks illustrated above are unlikely to have been the top picks of many people at the start of 2014, but their resilience and ability to navigate tricky economic environments stood them in good stead. Given the attributes of the firms that make up the balance of the SuperDogs portfolio, we are confident of the prospects for 2015. The portfolio represents a unique market offering that is invested in some great companies which are off the radar of most mainstream investors.