Shifts and surprising developments so far in 2014

08 May 2014 | Investments | Equities | Dave Mohr, Old Mutual Wealth

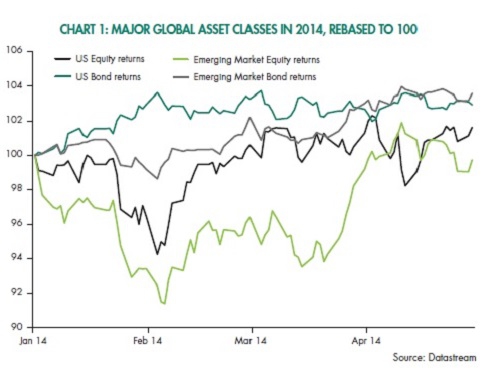

In 2013, equities soared and bonds were hammered as it became clear the Federal Reserve would reduce its bond-buying programme. In 2014, US equity and bond returns have been on par, and reasonably flat for the year. For the last two years, many analysts spoke of a Great Rotation from bonds into equities and investors after years of ‘hiding’ in low risk bond funds, will return to equities as their confidence increases. If this Great Rotation is taking place, so far market returns in 2014 don’t reflect it.

There has also been a shift in the improvement in sentiment towards emerging markets (EMs). In January, an old-fashioned EM crisis appeared to be brewing as some EM currencies fell and EMs again were out of favour. However, since late February, the currencies of the Fragile Five countries – including South Africa’s Rand - have mostly recouped their January losses. EM equities have also outperformed developed market equities over this period, but not by enough to make up for the underperformance of the last two years. Interestingly, EM bonds held up well throughout 2013, bouncing back faster than equities, indicating investors’ hunger for yields and their growing confidence that EMs will not default despite the external funding challenges EMs face.

PIIGS flying and Yuan falling

As emerging markets have battled, particularly the Fragile Five, the PIIGS countries (Portugal, Ireland, Italy, Greece and Spain) have staged a remarkable turnaround. From fears that they were on the brink of defaulting on their existing bonds just two years ago, they are now able to return to the market to issue new bonds. Greece’s ten-year bond yield peaked at 29% in February 2012; it is now below 7%. Spain’s five-year bond yield is lower than that of the US. However, the turnaround in financial markets has been much stronger than the turnaround in the real economy. It is therefore a surprise that the Euro has rallied against the US Dollar over the past year despite prospects of higher interest rates in the US while rates are likely to stay low in the Eurozone.

Another change in 2014 compared to 2013, is that China’s currency has weakened by 3%, which is minimal compared to the Rand’s wild swings, but is substantial given that the Yuan has been steadily (and deliberately in line with Beijing’s policy) appreciating since 2005. Whether this is an attempt to catch speculators off guard, to dissuade offshore borrowing schemes or to give China’s export machine renewed drive remains to be seen.

Local shifts also underway

The big shift has been from believing that there would be no interest rate hikes in the first half of 2014 to now trying to gauge how many there would be. The entire yield curve has shifted up, which means that for each maturity, the yield has risen. For instance, for bonds with a two year maturity, yields rose from 6% (on average) in 2013 to 7.5% in early 2014.

They have since fallen back somewhat, as a slightly stronger Rand has tempered the inflation outlook. Longer-term yields remain above average. After attracting R24 billion in net foreign inflows in 2013, so far this year the bond market has experienced R5 billion outflows. So far in 2014, the local equity market has seen a rotation from Industrials, the star performer last year, to Resources, 2013’s laggard. Financials have also performed well and the JSE has attracted R23 billion after receiving no net foreign inflows in 2013.