SA investment markets’ returns and equity market prospects

Christo Luus, economist at Third Circle Asset Management.

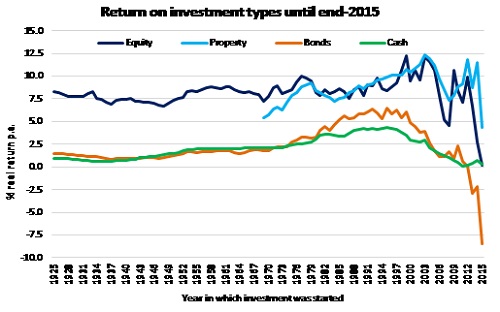

The South African equity market has had and uninspiring performance in 2015. In nominal terms, the FTSE/JSE All-share Index (ALSI) delivered 5.1%, which translated into a real return (i.e. after inflation) of only 0.2%. Five-year average real equity market returns still amounted to 7.1%, while 10-year average returns were 7.8% p.a.

In 2015, real returns on bonds amounted to a disastrous negative 8.4% (year on year) y/y. This was the lowest annual real return since the negative 16.8% recorded in 1994. During the past five years, real bond returns were still positive at 0.6% per year, while 10-year average annual returns amounted to 1.1%.

Real cash returns were marginally positive at 0.3% in 2015. Five-year annual average returns amounted to 0%, while 10-year returns were slightly better at 1.4% p.a.

Listed property (REITs) outperformed the above asset classes with a 4.3% real return in 2015. During the past five years, the average real property return was 9.2% per year, while the 10-year return amounted to 9.7% per year.

Although gold is not normally considered part of a diversified financial investment portfolio, it does have some good diversification characteristics. Even without possessing a yield component—as is the case with the other asset classes — the real rand return of physical gold came to 13.2% in 2015. Five-year returns were 7.7% per year while 10-year returns measured 7.8% per year.

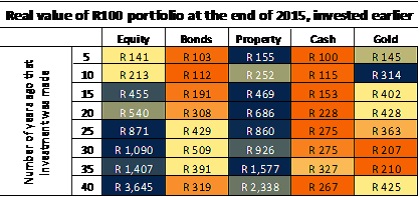

During the past 45 years, real returns amounted to 8.7% for equity; 2.1% for bonds; 2.1% for cash; 6.4% for property; and 5.6% for gold. (See table for other selected five-year periods.)

Because of volatility differences and the often uncorrelated nature of financial asset class returns in relation to each other, diversification among asset classes is usually a good strategy. However, the periodic extreme depreciation periods of the rand adversely affect all rand-based investments and positively influence dollar-denominated investments. Thus, if no maximum allocation constraint is stipulated for gold, an optimal ex-post asset allocation (in a medium-high risk portfolio) over the past 10 years would have called for 26% in cash; 7% in bonds; only 10% in equity; 15% in property (constrained at this level) and 43% in gold.

Considering a medium-high risk portfolio, which excluded gold during the past 10 years, would have called for an allocation of 36% in cash; 0% in bonds; 49% in equity; and 15% (constrained) in property.

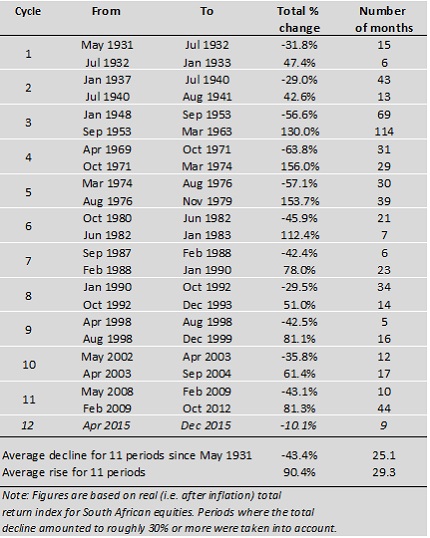

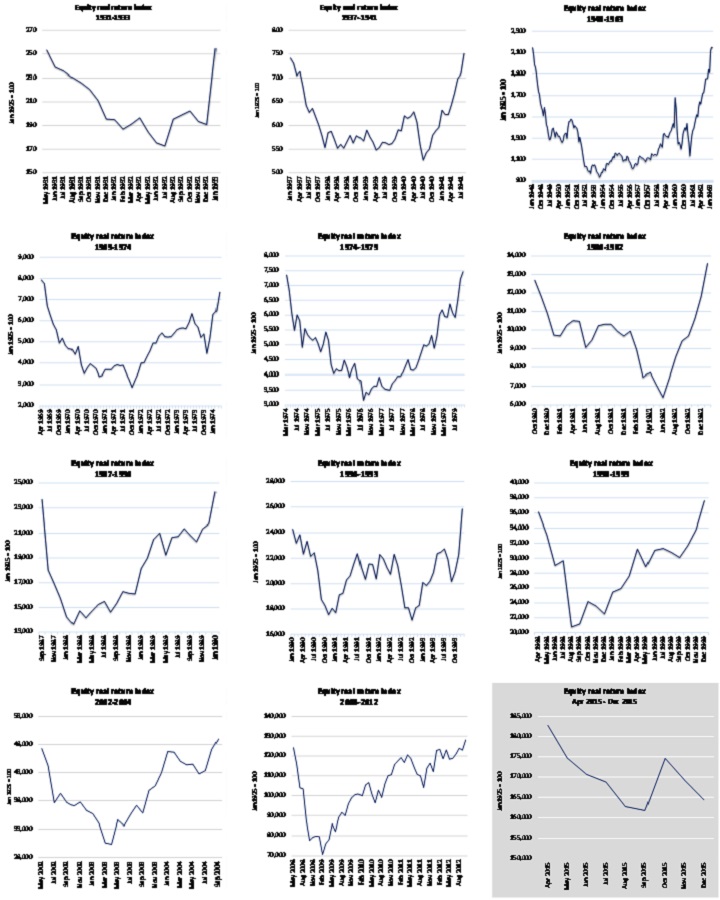

return equity index lost 30% or more of its value. Bear markets associated with such declines lasted on average 25 months, while all losses were, on average, recovered within 29 months.

The longest equity bear market lasted for 69 months (from January 1948 to September 1953) when equities lost 57% of their value in real terms. It took nearly a decade (114 months) for this entire loss to be wiped out and for the market to gain 130% in value. In contrast, the shortest bear market lasted only five months (from April to August 1998) with the real return index shedding 43% in value. In 1931 and in 1982, it took only around six months for the bear market losses to be recovered.

South African equities enjoyed a solid uptrend in value between October 2012 and April 2015, with the real return index appreciating by 43% in value. However, it would appear that a declining trend had commenced in April 2015. This downward move now amounts to around 10% in value (measured at the end of December 2015), so it does not as yet qualify — in terms of the earlier definition — as another bear market. However, some indicators (see next section) point to further equity market weakness in coming months.

Equity bear markets (>30% declines in total real return index) and recovery phases since 1925

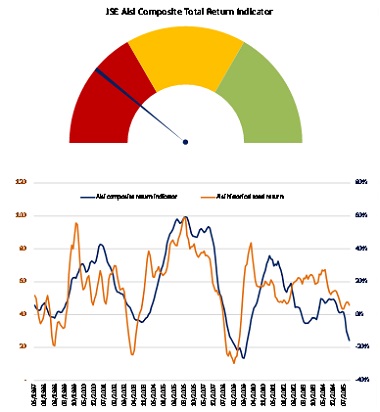

Signalling equity market prospects: Current indicator values (November 2015) and historical trends

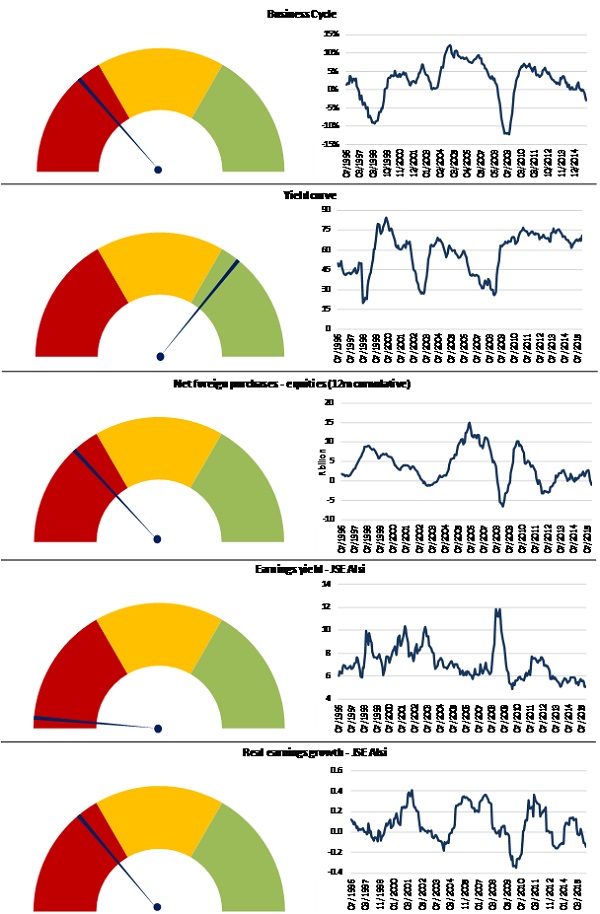

As can be seen from the dashboard on the previous page, most indicators were signalling weakening conditions for the South African equity market in November 2015. These indicator ‘speedometer’ values were obtained by standardising the historical time series to values of between 0 and 100.

• The y/y change in the SA composite business cycle indicator (published by the SA Reserve Bank) has been on a weakening trend since 2011. In September 2015 (latest published value), the leading indicator registered negative 0.6% y/y and the index is expected to have declined by around 1.5% in November 2015. The composite index is compiled from statistics, which include the gross value added measured in the economy; value of wholesale, retail and new vehicle sales; utilisation of production capacity in manufacturing; total formal non-agricultural employment; and the manufacturing production index.

• The yield curve is the difference between long-term interest rates (bond yields) and short-term interest rates. It is often considered an important equity market indicator since it reflects developments relating to monetary policy and inflation. When short-term interest rates rise, future inflation expectations will often decline, which could cause bond yields to decline (and bond returns to rise). Such a flattening — or even inversion — of the yield curve will mean higher money and capital market returns and could be detrimental for the equity market. Since 2009, the yield curve has been positive but fairly flat. The latest interest rate hikes have been quite gradual and contained, while recent bond yield increases have more than compensated for the tighter monetary policy stance. The yield curve has in fact become steeper, making it one of the few factors signalling positive equity market prospects.

• Often, one of the first indicators reflecting negative or positive changes in sentiment, is net purchases of equities by foreigners. The recent fiasco with changing finance ministers on a whim has sent foreigners reeling. During the final four months of 2015, net equity investment on the JSE by foreigners amounted to negative $2.7 billion, which brought the total net amount invested for 2015 at negative $350 million.

• Earnings yields—the inverse of the price-earnings (PE) ratio—has been at or below 6% since around April 2013. Such relatively high valuation levels mean that share prices, in general, are high relative to earnings levels of companies. In November 2015, the ALSI earnings yield stood at 5.1% — surpassed only by the 4.8% yield recorded in February 2010.

• Real earnings growth numbers of the ALSI have been on the decline over the past year — from 13% y/y in January to negative 14% y/y in November. Resource shares’ earnings have been a major downward driver of tumbling ALSI earnings growth rates, but lately consumer goods sector companies’ earnings have also declined, while industrial sector earnings growth has weakened considerably.

The composite index compiled from the above sub-indices shows a potentially weak period ahead for the JSE equity market.