SA equities set to play catch-up as global investment prospects diverge

Nicolas de Clerq

Could 2025 be the year for SA Equity? 2024 saw US Equity (S&P 500) having another year of stellar performance of 26% in the calendar year after 27% in 2023. The Jury is still out on whether US equity can achieve a third consecutive bumper year, which may leave investors feeling uneasy.

Furthermore, 2024 witnessed a large divergence in global equity market performance with the SA All share index returning 15%, trailing behind China - its emerging market counterpart - which returned 20% in the year (see figure 1 below).

Figure 1: Calendar-year returns

Sources: Prescient Investment Management, Bloomberg (as at January 2025)

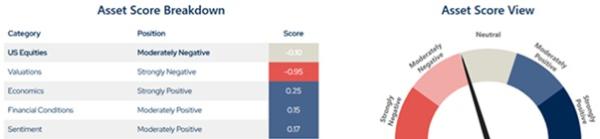

Adding to investors’ discomfort is the historically high valuations of the US equity market with a Price-to-earnings (P/E) ratio of 27. Which has only been higher twice in its history: once in 2021 and once before the dot com bubble in 1999. After which the S&P had drawdowns of up to 47% and 25% respectively. At Prescient, we make use of carefully crafted quantitative models to take views on assets. As of Jan 2026, we hold a neutral view on US equity with the main detracting factor being valuations (including the P/E ratio).

Figure 2: US Equities

Source: Prescient Investment Management (as at 28 January 2025)

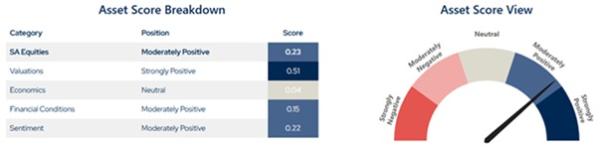

In contrast, we have a moderately positive view on SA equities, driven primarily by valuations. The All share index currently trades at a PE ratio of 12, which is well below its median level. This underscores South Africa’s relative cheapness compared to the U.S.

Figure 3: SA Equities

Source: Prescient Investment Management (as at 28 January 2025)

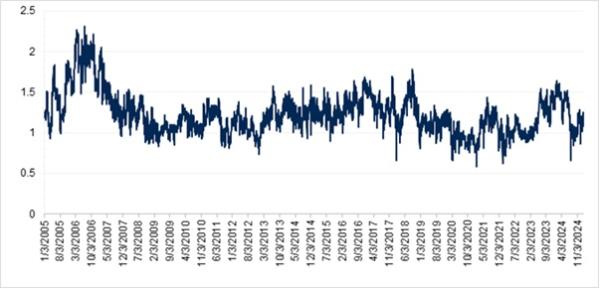

Historically investors would be cautious of emerging market equity due to its relatively higher levels of volatility compared to developed markets. To examine this further, we look at 3-month implied volatility as an indicator of the market’s perception of forward-looking risk for these two indices (shown in the figure below).

Figure 4: Ratio of SA All Share implied vol to S&P 500 implied vol

Sources: Prescient Investment Management, Bloomberg (as at January 2025)

We can see that historically volatility is slightly higher for the SA All share index, however the key finding is that they have somewhat converged recently.

The combination of comparatively cheap South African equities and currently low volatility could attract investors seeking better risk-adjusted returns. This situation has only occurred once before - in 2021 - when the SA All Share Index subsequently outperformed the S&P 500. As a result, 2025 may well be the year in which SA equities begin to catch up on the global stage.