Reasonable growth expected

Global equities have had a good start to 2015, with many of the major equity indices making new historic highs in local currency terms during the quarter.

2015 so far

The main driver has been policy action, with the ECB announcing a larger than expected QE programme, further stimulus measures in China and a four month extension to the Greek bail-out programme. The European equity markets have been one of the clear winners so far this year after a strong multiple driven rally on the back of QE and some more positive indications of a turn in growth. The US market has lagged in local currency terms, with a stronger dollar weighing on profits at multinational companies.

Despite a growing consensus that the major government bond markets offer little value, yields have continued to fall, particularly in Europe, on the back of the ECB implementing QE. Over the quarter the 10-year German Bund yield fell from 0.54% to 0.18%, a new historic low for Bunds. European periphery bonds also extended their gains over the period with Spanish and Italian 10-year government bonds ending the quarter yielding 1.21% and 1.24% respectively. US bonds were much more volatile with 10-year yields trading between 2.25% and 1.65% before ending the quarter at 1.92%. This volatility was driven by the continued uncertainty over the timing of the Fed’s first interest rates increase.

The key theme in the currency markets during the quarter was the continued strength in the US dollar buoyed by the increasing divergence in monetary policy, particularly with the ECB finally implementing sovereign bond QE. Sterling saw political risk increase as the UK General Election in May draws closer and in the Emerging Market space there was a relatively wide divergence in performance. While the Russian ruble rebounded strongly off its lows the Brazilian real declined sharply on increasing economic concerns.

The year ahead

The global economy is expected to deliver reasonable growth for the remainder of 2015 with the improvement being driven by the developed markets although the growth rate remains higher in some Emerging Markets. Growth expectations are further supported by the lower oil prices. Recent US data has been weaker, likely reflecting temporary factors such as the severe weather and port strikes on the West coast. We expect the US economy to continue delivering reasonable growth, but there may be some downside revision to the current consensus forecasts. Data for April will be scrutinised for signs of a rebound.

The euro area economy is recovering despite the many twists and turns in the Greek saga. Further monetary stimulus, a weaker exchange rate, stronger asset prices, a lower oil price and improved confidence are spurring better economic news from Europe. A potential Greek default and possible euro exit cannot be ruled out, but this is not our base case scenario at present – we expect the Greek government to be able to strike a last-minute deal with creditors. An adverse outcome of a Greek default would certainly be a negative shock to the region but will be mitigated by improving economic fundamentals regionally and the ECB’s QE programme.

Macro conditions in Emerging Markets are diverse. Chinese growth will continue to slow but we expect substantial monetary easing by the People’s Bank of China to soften the fall. In response to recent measures (such as interest rate cuts and lower reserve requirements for banks), monetary conditions are easing. The prospects for India are for an acceleration in growth with the low oil price being a major benefit as inflation trends lower along with structural reforms. Modi’s government’s first full budget struck a fine balance between fiscal discipline and supporting the cyclical economic recovery. We expect further interest rate cuts from the Reserve Bank of India.

If our views on growth are correct, then global inflation is likely to bottom sometime around Q2 or 3 of this year and then start to rise gradually. We expect the oil price to remain under pressure in the first half, reflecting the current over supply. However, as production is cut and demand increases we see the oil market moving towards balance. We expect a slightly firmer oil price in the second half of this year, which will result in some upward pressure on inflation. This should alleviate deflationary concerns. Low inflation will help sustain loose monetary policy on a global basis even if US interest rates move gradually higher. We expect the Federal Reserve to increase interest rates in the second or third quarter.

Implications & our strategy

Against the backdrop of low bond yields, an expectation that the pace of economic growth is gathering momentum, low inflation and loose monetary policy; we continue to favour equities over bonds. However, overall global equity returns are likely to be more muted in the next five years compared to the previous five when they averaged around 10% (in nominal USD terms). After the strong gains in recent years, equity valuations are not depressed but they remain a more attractive proposition to fixed income and cash.

The large overweight position in equities was very slightly trimmed back in March, although we remain overweight the asset class. From a regional perspective, the overweight positions in Europe and Asia was increased using futures, moving us more underweight the US. This reflected better valuation opportunities outside the US, stronger monetary stimulus and better earnings momentum.

We continue to believe that developed market government bonds offer little value at current levels (in the medium term) despite the sharp fall in global inflation and have largely become return-free risk. German bonds are already pricing in an interest rate environment very much like that which Japan has endured for more than 15 years. Meanwhile, the sovereign spreads of European periphery government bonds is the lowest since the Greek crisis first erupted. Although US yields remain higher in absolute terms they do not offer very attractive returns. Corporate bond spreads widened in the US in 2014, especially in the high yield sector where energy companies have a sizeable weighting, but have shown an improving trend of late.

We remain underweight duration within the fixed income component with the main focus on investment grade and high yield corporate debt. Within Emerging Markets, we continue to hold positions in Mexico and India, where we think yields look reasonably attractive given expected interest rate and exchange rate dynamics.

From a currency perspective we still prefer the US dollar against the other major developed market currencies and many emerging markets. The euro remains under pressure from an extremely low yield environment and is also likely to weigh on sterling, which also faces risks from the upcoming election. In the UCITS funds, we have funded currency exposure to the US dollar, Indian rupee, Mexican peso and more recently Brazilian real through a combination of sterling, euro, Swiss franc and Korean won.

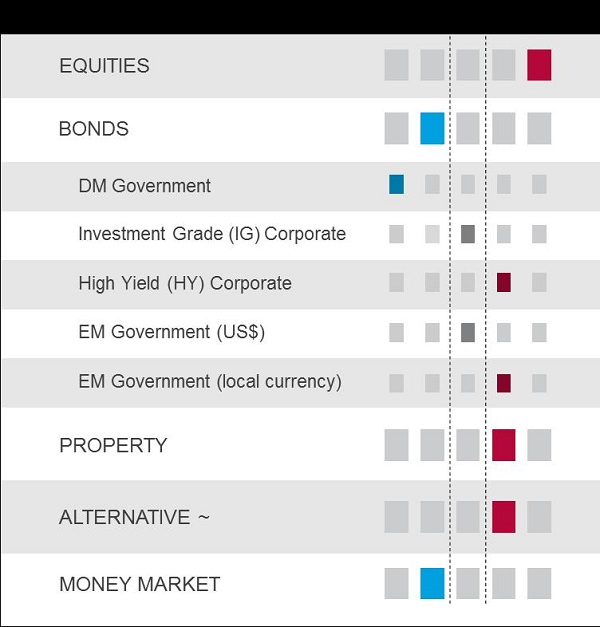

The table below depicts an overview of our asset allocation strategy and is reflective of our views mentioned above.

~ Specifically refers to UK infrastructure assets

Source: Ashburton, 31 March 2015