Oil markets and energy equities following Middle East conflict

The escalation of conflict involving the US, Israel, and Iran over the weekend has created significant disruption and uncertainty in global financial markets, with multiple critical developments unfolding.

While it is inevitable that broader equity and fixed income markets will suffer weakness, going into the conflict, the energy equity sector had a few supportive elements on its side:

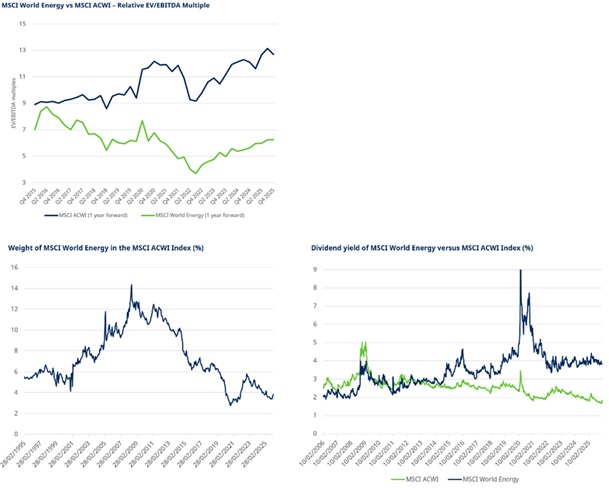

a) Most investors are underweight energy in their portfolios, with many having a zero-weight position right now. This is reflected in the weight of energy in the broader MSCI ACWI being at just 3.5% and the lowest level in the last four decades.

b) The fundamental outlook for oil, gas and power markets is positive. Pre any supply disruption, oil markets are balanced; and as a result of over a decade of underinvestment, the sector needs to go through a reinvestment phase.

c) In addition, driven by an extraordinary period of required growth in power generation, consumption rates for natural gas are growing at a pace of 2–3 times faster than historical rates over the next decade.

d) The lack of reinvestment in both oil and gas markets is matched by high dividend yields and share buyback yields being returned to shareholders.

e) Despite these attractive yields being supported by strong free cash generation the sector continues to trade at a significant discount to the broader market.

The events over the weekend highlight how quickly energy markets can become unbalanced as a result of the challenging political environment.

Below is a simple bullet point summary of what supply disruptions are expected in the short term:

Immediate supply disruptions

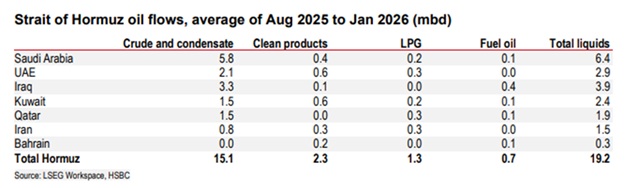

• Oil and gas shipping through the Strait of Hormuz remains just about open for now. This is the critical chokepoint linking the oil-rich Persian Gulf to open seas, as Iran has cranked up threats to vessels transiting through the waterway. On Sunday, only a trickle of vessels were moving out of the waterway, with none appearing to enter.

• Tanker attacks are not off the cards. On Sunday a small oil tanker was targeted off Oman's northern coast near Khasab port. There is already a video of an oil tanker on fire and sinking after attempting to pass through the Strait of Hormuz.

• It is impossible to estimate how much supply will be disrupted to the wider market, but it’s worth noting that around 19mb/day (18%) of the 106mb/day oil market passes through the Strait of Hormuz.

• The potential economic consequences are complex and far-reaching. Both China and Russia rely on Iranian hydrocarbons (China) and military equipment (Russia). For Europe and other economies, the primary risks stem from uncertainty and the potential for higher hydrocarbon prices to push up consumer prices.

• It is also likely that Iran may refrain from attacking broader oil production across the Middle East unless and until its regime faces imminent collapse or prolonged US strikes – and the more damage it suffers from US and Israeli strikes, in theory, the less it would be capable of committing such attacks.

The global gas market will also be impacted. Qatar is a major supplier of liquefied natural gas (LNG) to both Europe and Asia and separately and Jordan has already reported that natural gas supplies from the Mediterranean have been halted.

Expected price impact

• Many analysts are also warning that a prolonged Strait of Hormuz disruption could push oil prices significantly above $100/bbl, potentially sparking a 1970s-style energy shock.

• OPEC+ have agreed in principle to increase oil production by over 200kb/day in April, as key members led by Saudi Arabia and Russia respond to the conflict – but this does not take into consideration any supply route disruption.

• But coupled with the very low reserve lives of some major non-OPEC producers, any actual output boost from the OPEC+ members will be constrained by the group's limited spare production capacity. In essence, the global oil market has been stripped of its usual shock absorbers, risking severe price spikes if supplies are disrupted.

Energy equities versus broader equity market

The Middle East has been thrust into a widening conflict and, without question, broader equity markets face a significant risk-off reaction, given broad equity valuations are just not that cheap.

From today’s vantage point, it is very easy to paint a worst-case scenario, with a strong possibility of attacks on critical Gulf region infrastructure.

In contrast, energy equities are cheap.