Is it time to ditch SA equity?

Harold Strydom, Investment Strategist and Portfolio Manager, Citadel

Given South Africa’s abysmal economic performance and years of anaemic market returns, negative sentiment has sent local investors sprinting for the greener pastures of offshore equities.

So, while Regulation 28 limits the offshore exposure of retirement funds to a maximum of 30%, a question frequently raised by investors is: does South African equity still have any place in discretionary savings portfolios?

The answer is that although in our view global equity currently represents a more attractive “buy” prospect than local, this does not mean that you should sell out of SA equity.

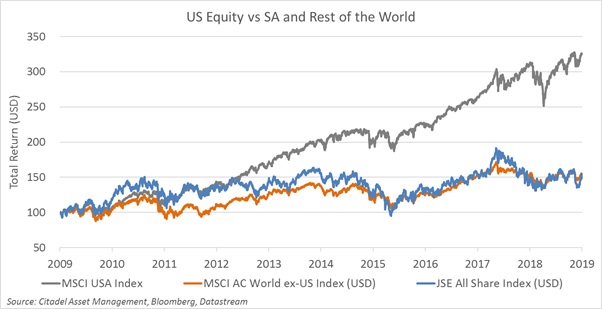

It’s true that global markets have significantly outperformed the Johannesburg Stock Exchange (JSE) over the last ten years. However, this was largely the result of a surge in strength from the United States. In fact, a closer examination of the MSCI All Country World Index (ACWI) excluding the US reveals that global market returns were largely in line with the JSE’s returns in dollar terms.

Moreover, the narrative that poor economic performance in SA has caused the JSE to underperform substantially is patently false. Measured in dollar terms, the JSE’s performance over the past decade is virtually indistinguishable from emerging markets and Europe, even though many of those regions fared far better economically.

And here it is important to note that the JSE is still home to world-class international companies. Some 71% of the JSE Top 40’s earnings are derived outside of South Africa, and in particular the east and China as a result of exposure to Tencent and commodities – which is why the JSE’s movements are often in line with non-US stock exchanges.

Cyclical relative performance

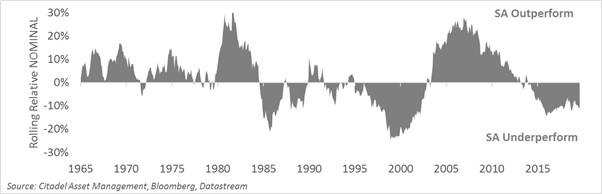

The most compelling argument for SA equity as part of a long-term investment strategy, however, lies in a comparison of the JSE’s historical performance with the US market.

History reveals that the JSE’s recent period of underperformance relative to the US is not a new or once-in-a-lifetime occurrence. In fact, it is the norm rather than the exception, as the SA market regularly goes through cycles of outperforming and then underperforming the US, as seen below:

In 1998, for instance, hot on the heels of the emerging market crisis, a bleak economy and poor returns, especially compared to the US, also saw a number of South Africans disinvest from the JSE and move funds offshore – despite an unattractive rand exchange and poor global stock market valuation levels.

But soon after that, the early 2000s saw the beginnings of what is commonly referred to in the US as “the lost decade.” The turn of the millennium saw US markets reach the height of the dotcom bubble and then subsequently crash, followed just a few years later by the Great Recession. Together, these meant that the US had one of its worst decades in memory. And unfortunately, all those who had disinvested missed out on what would eventually prove to be an amazing decade for the SA equity market, which produced some of its strongest real returns on record.

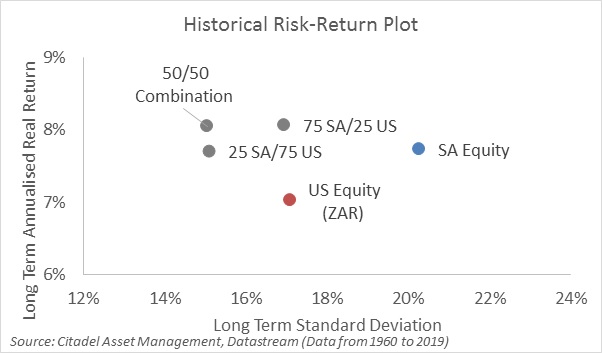

That said, equities are by their very nature long-term investments and, far from advocating that investors should choose SA over the US, evidence further shows that a combination of SA and US equities has historically delivered a superior outcome from both a risk and a return perspective than either alone.

In the nearly 60 years between 1960 to 2019, SA markets delivered real returns of 8% with a standard deviation rate (which is used to measure volatility) of 20%. Also measured in rand terms, US markets over the same period delivered real returns of 7% with a standard deviation rate of 17%. But investors who opted for a 50/50 combination of both would have seen the best results, achieving real returns of 8% with a standard deviation of just 15%, as demonstrated below:

This then suggests that, from a strategic portfolio construction perspective, the contracyclical properties of SA and US markets can be used to ameliorate risk and enhance investment returns.