How to improve the predictability of equity returns

Guy Fletcher, Head of Institutional Solutions and Research at Sanlam Investments.

Delivering persistent returns above your chosen benchmark doesn’t have to be a function of trying to pick and blend the best active equity managers, says Guy Fletcher, Head of Institutional Solutions & Research at Sanlam Investments.

In his recent research paper ‘How to improve the predictability of equity returns’, Fletcher demonstrates that including systematic strategies such as portable alpha and smart beta can both extract the benefits of diversification while still complementing the process of selecting traditional active managers.

Fletcher makes his point of by showing us how to build a portfolio of strategies to maximise the probability of outperformance.

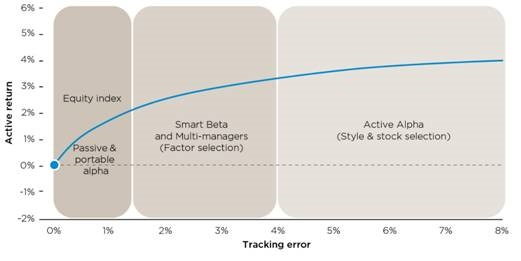

He does this by creating a graphical representation of the opportunity set in relation to the benchmark, using efficient frontiers (see below). Risk (tracking error) is represented on the horizontal axis and alpha (excess returns) on the vertical axis. The efficient frontier is the perfect representation of the goals of investing, ie, you should achieve higher returns as you incur higher risk (represented below by tracking error). It also demonstrates the law of diminishing marginal returns, ie, each additional unit of risk delivers a reduced additional level of return.

Broadly speaking, says Fletcher, we categorise the passive index management world (including portable alpha) as strategies with tracking errors of less than 1.5%, systematic and composite strategies (including Smart Beta and multi-management) to be between 1.5% and 4% tracking error, while traditional active managers are usually in the 4%-plus tracking error range.

Efficient frontier - Active return space

What was interesting to note in the research findings, says Fletcher, is:

1) Strategies are not completely independent of each other, so building a portfolio needs to take into account the way these strategies interact with one another. This is reflected by the covariance matrix, which tends however, to be unstable over time. We therefore need to estimate what the future relationships are.

2) Secondly, relative to benchmarks, index plus portable alpha strategies and Smart Beta strategies behave far more predictably than traditional individual active strategies.

We can therefore use this to build more predictable outcomes in line with the level of risk we are willing to accept.

Fletcher further observes that selecting consistently-outperforming traditional active managers is not only difficult, but individual manager persistence is rare. Indeed, his research revealed that longer-term outperforming active managers tended only to be in the top 25% of all managers less than half the time, on a rolling three-year basis. The desire for excess performance can therefore can lead to inappropriate manager rotation, thereby impacting cumulative returns.

Fletcher concludes that to bring greater levels of predictability to equity portfolio returns, you would need to challenge the traditional preference for merely blending active managers. Instead, his research reveals that the ideal solution would be to include a portable alpha element (that brings stability) combined with a smart beta strategy (to yield maximum diversification) in conjunction with traditional manager selection.

Structuring portfolios to take advantage of these independent processes is far more likely to improve the consistency of returns, he concludes.