Global and thematic equities outlook for 2022

Supply chain disruption should diminish in most industries in 2022

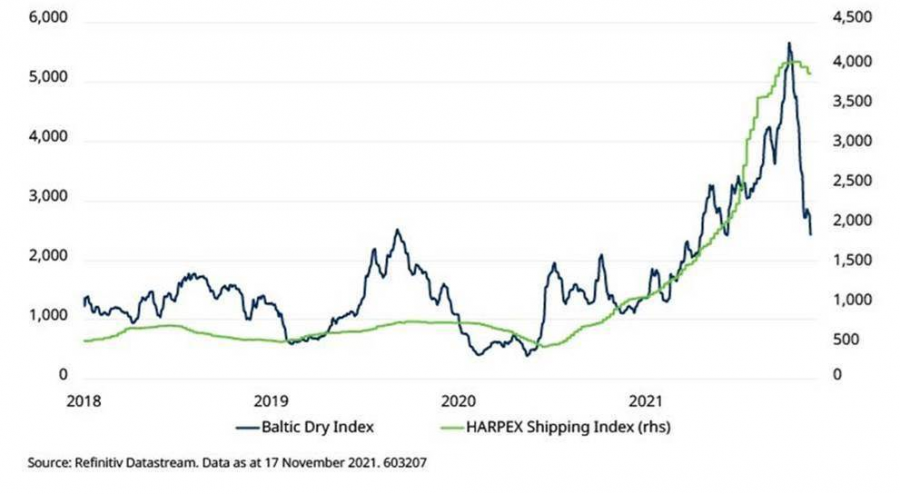

The significant disruption to supply chains seen in 2021, largely linked to Covid-19-related capacity shutdowns and transportation bottlenecks, is set to diminish as we move into 2022.

Supply chain backlogs historically adjust quite rapidly after periods of stress, as the market responds to higher demand and re-builds inventory. We see no reason to assume that this won’t be the case in 2022, and indeed freight shipping rates have already started to fall.

Global shipping indices signal easing supply pressures

However, energy prices are likely to remain elevated for a number of reasons. The economic recovery is boosting demand for oil and gas at a time when supply growth is static. As governments have encouraged energy companies to spend more money on renewables, spending on traditional exploration and production has been cut. As a result of this underinvestment, supply is not only tight but in many cases set to shrink quite rapidly, particularly if emissions targets are to be met. Consequently, traditional energy prices will likely stay high for some considerable time.

There can be little doubt that, in the future, oil and gas reserves in the ground will be worth a fraction of their implied value today. But, for the time being, traditional energy may generate super-normal cashflows and profits. We don’t believe that that is a consensus view.

Inflation remains a concern

Fund managers have been concerned for some time that inflation would prove to be more than “transitory” and, so far, the omens are not good. October US producer price inflation of 8.6% was a shocker and reflects the impact of price rises across the spectrum: from higher energy and commodity prices all the way through to rapidly rising labour costs.

The latter phenomenon has caught many economists by surprise: a meaningful proportion of the workforce in both the US and in Europe has yet to return to work. The resulting labour shortage has put substantial upward pressure on wages, with average hourly earnings in the US now growing at 5% and set to accelerate further as workers respond to higher fuel, housing and fuel costs by escalating wage demands.

Overall, despite some moderation in supply shortages, price pressure is acute and the rise in consumer price inflation in October to 6.2%, the highest rate since 1982, was no surprise to us. It is hard to see a rapid change of direction in price pressures, particularly given that the recovery momentum appears to be strong in all major regions globally.

Margins will be under pressure in many industries

Corporate earnings growth in 2021 has been remarkably strong. Record monetary and fiscal stimulus has supported the rapid turnaround in business activity after Covid-19 vaccines were approved late last year. US companies in the S&P 500, for example, are on track to deliver $225 per share of earnings in 2021, or a 65% increase compared to 2020.

The fact that earnings have been so good in 2021 makes it very likely that there will be significant challenges in 2022. Not only are US margins now back at record highs, but the full impact of higher input costs has also yet to be felt. With the tight labour market creating competition for qualified workers across multiple industries, there will be further pressure on margins, particularly in the service sector. This all adds up to a much more challenging environment for profitability.

Pricing power is likely to be a key factor over the next 12-24 months

Against that backdrop, there are clear risks to equities next year, especially since valuations are now relatively extended (particularly in the US). The old maxim that bull markets don’t die of old age certainly seems to be holding true at present.

It is also conceivable that companies will be able to muddle through the next 12 months by passing on higher prices to consumers, whose household finances are mostly in good shape and who may find a 5% price hike for consumer goods tolerable as wages rise.

However, many companies, especially those in fragmented industries with little or no product differentiation, will not be able to pass on higher costs.

In the current environment, the consumer staples and industrial sectors would appear most vulnerable to higher input costs given the sharp rise in base commodities such as grains and sugars or steel and copper. These industries are generally also highly competitive.

But there are notable exceptions: Nestle was able to raise prices by more than 4% compared with 2020 in the third quarter of 2021 on the back of its powerful global coffee franchise, while other companies in the sector, such as Unilever or Proctor & Gamble have struggled to raise prices at all.

Perhaps the best examples of positive pricing power are to be found in the technology sector, particularly amongst the dominant so-called mega-cap platforms. Software companies such as Microsoft or Adobe, which provide essential tools to companies, governments and households, are in a unique position because they can increase their annual subscription charges each year.

Similarly, a handful of very large internet platforms, notably Google-parent Alphabet, dominate the digital advertising market (which in turn is becoming the dominant channel for advertisers of all sizes). In the first nine months of the year, Google revenues grew 45% compared with a year earlier, helped by strong pricing.

Many other software, internet, and semi-conductor companies can build in regular price rises while keeping cost growth extremely muted. These areas will continue to be fertile hunting ground for growth in the coming year.

Mega-trends continue to gather pace

Stepping back from the immediate challenges, there are a number of structural drivers that are likely to have a material impact on equity markets over the next decade and beyond.

Most of these trends (often known as “mega-trends”) are far from new. Climate change, energy transition, demographic change, healthcare innovation, digitisation, automation, and urbanisation have been relevant for many years. However, their relevance is increasing exponentially as populations grow. In some cases, the pandemic has simply accelerated the process of change.

Although there are major challenges that need to be addressed on a global scale, and quickly, there are plenty of reasons to believe that these can be tackled. As evidenced by the production of a revolutionary vaccine just nine months after the emergence of Covid-19, we are living in a golden age of innovation.

The convergence of multiple technologies from processing power, connectivity, bandwidth and memory all the way to power delivery and software is resulting in a wave of innovation across multiple industries, most of which would not have been possible even a few years ago.

The Covid-19 vaccine could not have been developed without DNA sequencing technology. Similarly, the process of energy transition is now possible because of the extraordinary progress in battery capacity, renewable electricity generation capability, and grid technology. The process of global transformation is ongoing, and it is broad-based, pervasive and long-lived.

From an investment standpoint, the opportunities are immense. If we are right about the implications of the mega-trends, then investing in the companies exposed to them could offer the prospect of markedly superior returns than a traditional equity index.

Final word: it pays to engage

According to the old English proverb: “He that converses not, knows nothing.” That certainly applies to investment. And yet it is surprising how often both investors, and the management teams they invest in, fail to interact. Traditionally, public equity investors have chosen to exercise their views primarily via the proxy voting system. As a rule, they have voted, and continue to vote, with company management

In a complex and rapidly changing world, a regular and constructive dialogue between the providers of capital and their investees would seem essential. A management team may not appreciate the importance of a specific issue, such as sustainability or social welfare, from an investor’s point of view.

Equally, an investor may not appreciate the extent to which a company has committed to evolving its business model in order to meet some of the challenges we discussed earlier. Investment does not stop at buying a share. Active engagement is a must.