Five takeaways on the potential rewards and risks facing global equity investors

Simon Webber, Head of Global Equities, Schroders, looks at the ways that increased market breadth and volatility against a resilient economic backdrop should create opportunities for active fund managers.

A soft landing for the US economy remains our central scenario and we expect equity markets to be well-supported in the medium term by modest growth in corporate earnings. In Europe, inflation has remained on a clear downward path as the eurozone and UK have emerged from shallow recessions.

This has allowed the European Central Bank and Bank of England to begin cutting interest rates. Economies such as the UK and Spain have a high percentage of floating rate mortgages and a decline in interest rates will provide some immediate support to the consumer. We are also seeing higher real wage growth in Europe and the UK, which combined with excess savings, should further support consumption growth.

The August market correction saw a de-rating in equities to reflect a more uncertain outlook for the US economy, but they have quickly recovered losses, supported by good earnings growth and the outlook for easier monetary conditions. Equity markets were vulnerable to a correction after a very strong nine months, but company fundamentals are decent and heightened volatility creates opportunities for repositioning where dislocations occur.

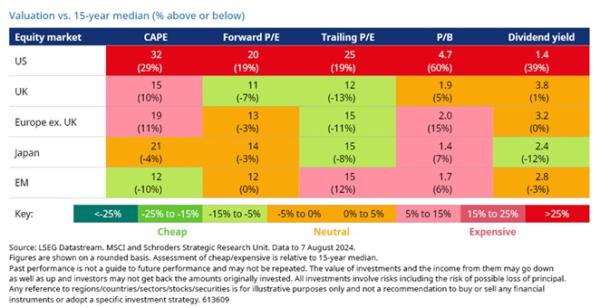

1. Headline valuations continue to favour markets outside of the US

Based on commonly used metrics, the UK remains one of the most attractively valued markets globally relative to its long-term history. In global equity markets, valuations continue to favour ex-US markets, particularly the UK, Japan, and emerging markets (EM) (see table, below).

However, valuations in the US market looks less demanding when you look beyond the “Big Tech” mega-cap growth stocks, which are dragging up the overall P/E multiple of the S&P 500. The Big Tech stocks have, in aggregate, benefitted from both relevant thematic exposures and strong fundamentals. In contrast, the reminder of the market has been contending with a still tough operating environment, which has dampened top- and bottom-line growth for much of this time.

2. Scope for market drivers to broaden, creating opportunities for active investors

Market breadth has remained at extremely low levels over the past year as a narrow set of stocks has accounted for the vast majority of market gains. The narrowness in markets to date has been a function of both top-down drivers – the AI thematic – and bottom-up fundamentals, represented by divergent revenue and earnings growth.

Consensus is now anticipating this gap to close somewhat, with expectations of an acceleration in earnings growth for the broader market, and a significant deceleration for the Big Tech cohort (see chart, below). The mega-cap US tech companies have demonstrated very strong earnings growth in the last 18 months, driven by renewed cost discipline and sustained revenue growth.

The benefits of that cost discipline are expected to wane in coming quarters though, bringing earnings growth down closer towards the rest of the market. In aggregate, these companies remain underpinned by great businesses and strong fundamentals, but they are vulnerable to downside asymmetry on revenue and earnings delivery relative to the rest of the market.

There is also a case for a broadening of equity market returns regionally. European economies will be more sensitive to interest rate cuts than the US economy, and in Japan real wages have turned positive after many months of contraction. Europe and the UK for example both saw a return to positive GDP growth earlier this year following a period of weaker growth and a more protracted earnings slowdown.

These regions should be further supported by interest rate cuts. European consumers in particular have higher exposure to variable interest rate mortgages (relative to the US) and companies are more dependent on bank lending. In contrast, the narrative in the US has shifted from bringing inflation under control to avoiding a recession. While a US recession isn’t our base case, there is the potential for catch-up in some regions.

Click here to read more...