Equity and bond markets square off

Dave Mohr, Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Buoyed by a supportive macroeconomic backdrop and surging reported earnings, global equities posted the third best January return (5.6%) since the launch of the MSCI All Countries World Index in 1987. The US, where company profits will now get an extra boost from lower tax rates, was the top performing developed market, but the weaker US dollar also boosted dollar returns from other markets. The bull market has finally captured the imagination of retail investors, with equity mutual funds worldwide reporting the best monthly inflows on record, according to Bloomberg.

The S&P500 returned 5.7% in the month on the way to fresh record highs, which lifted the return over one year to 26.6%. Fourth quarter financial results released during the month were mostly above the already optimistic forecasts of analysts.

The Eurostoxx 600 was positive in January with a 1.7% return in local currency, but the stronger euro limited gains. Similarly over one year, the 13% euro return looks subdued compared to the US (but in a common currency the returns are similar). The euro gained 15% against the greenback over 12 months and 3.7% in January alone, ending at a three-year high of $1.25. The Japanese Nikkei 225 returned 1.4% in January in yen, and 23% over 12 months. The yen gained 3% against the dollar in January.

Emerging market equities posted another strong month, supported by a weaker greenback with the MSCI Emerging Markets Index returning 8.4% in dollars, and 41% over the past year. Despite outperforming developed markets since early 2016, the index has not made up for the underperformance from 2013 to 2015. China, Brazil and Russia were the top performers in January.

Bond sell-off

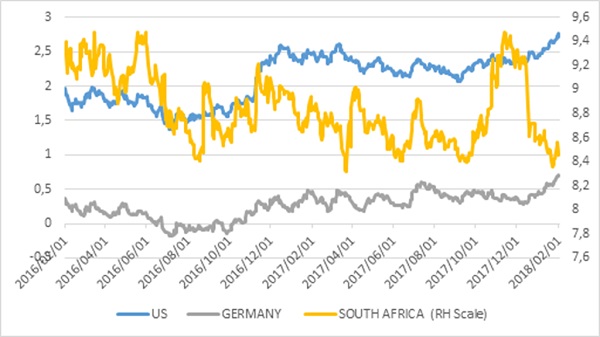

However, the optimism of equity investors was tempered by a sell-off in global bonds last week, resulting in rising bond yields and falling share prices. This was accelerated by Friday’s US labour market reports which showed not only decent payroll growth (200 000 new jobs in January), but also a surprise jump in wage growth to the highest level since 2009 (2.9%). Faster wage growth could result in higher inflation and therefore speed up the Federal Reserve gradual interest rate hiking cycle. The increase in yields was driven largely by expectations of higher inflation as global economic activity gains momentum, and a view that central banks would eventually respond by tightening policy. The US 10-year Treasury yield rose above 2.8% for the first time since April 2014. The equivalent German yield increased from 0.4% to 0.7% and the Japanese 10-year yield from 0.05% to 0.09%.

Low bond yields supported the post-crisis equity rally by lowering companies’ borrowing costs, but also making equities relatively more attractive as equity earnings yields were (and still are) well above bond yields. As bond yields rise, equities could in turn become somewhat less relatively attractive. However, since bond yields are rising for “good” reasons (i.e. a stronger economy) rather than “bad” reasons (surging inflation), it should not lead to heavy equity losses.

In terms of the sustainability of economic growth, the main ingredients remain in place. Confidence is high in the world’s major economies, as evidenced by purchasing managers’ indices and other surveys. This means consumers are spending and businesses can continue to invest. Capital expenditure by businesses is running at the fastest pace in several years.

Gradual removal of monetary stimulus

The other key ingredient for sustained global growth is that emergency monetary policy measures put in place after the financial crisis – such as zero (or negative) interest rates, quantitative easing (bond buying) and forward guidance (a commitment to maintaining loose money) – are not withdrawn too quickly. As long as inflation does not jump unexpectedly, this should be the case. The US Federal Reserve is the furthest down the road of removing stimulus, but is treading carefully. Its meeting last week, the last under the leadership of Janet Yellen, did not result in any policy change. But the big question is how quickly it hikes in the months and years ahead. The Fed is currently expected to deliver three small rate hikes this year, although a fourth increase might be a possibility. It will also continue reducing the size of its balance sheet by $50 billion a month by not reinvesting maturing bonds.

Despite strong economic growth and rising interest rates, the US dollar weakened through the course of 2017 and further in January (though it picked up a bit late last week as risk aversion increased). This can be partly explained by the fact that growth outside the US has picked up nicely, with higher interest rates to follow eventually. (The dollar surged between 2011 and 2015 as the US economy grew much faster than its peers and markets anticipated interest rates rising from near-zero levels.)

In many respects, a weaker dollar is good for the world. It supports emerging market currencies, which in turn creates scope for lower interest rates in those countries. It also eases the burden of servicing the billions of dollars of dollar-denominated debt that companies in emerging markets incurred. Finally, it tends to support higher commodity prices.

Bucking the trend

In contrast to the bond sell-off in developed markets, local bonds delivered a positive return in January, supported by a stronger rand and optimism of political change. The All Bond Index returned 1.8% in the month and 10.8% over 12 months. The 10-year South African government bond yield declined from 8.6% at the start of January to 8.4%. At the end of January 2016, the 10-year yield traded at 8.8%. Yields are still comfortably above expected inflation and bonds can therefore deliver attractive real returns.

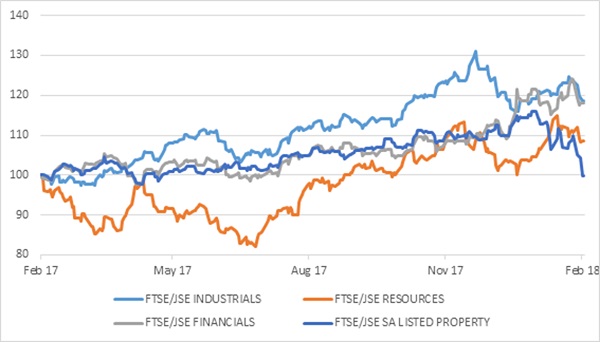

Local equities are also bucking the global trend so far in January, with the JSE pretty much flat. But last week it followed global markets lower. The FTSE/JSE All Share Index returned 0.1% in January, but the return over 12 months is still a respectable 16%. The FTSE/JSE Shareholders Weighted Index (SWIX), with a larger weight to Naspers, lost 0.68% in the month, limiting the 12-month return at 17.3%.

Naspers was down 2% in January, by no means the biggest loser, but its 20%-plus weight in the SWIX has a massive impact on the index. It fell further last week. Despite the Naspers loss, industrials were marginally positive in January as consumer goods (Richemont), general industrials, retailers and telecoms posted good gains.

Resources had the best month of the three main economic sectors on the JSE. Led by platinum and general mining, resources returned 3% in January. However, it lags industrials and financials over one year with a return of 9.8%.

Viceroy jitters

Financials lost 2.9% in January. Capitec plunged after short-seller Viceroy released a note attacking the bank’s lending practices and provisioning for defaults. The Reserve Bank, which regulates all banks in South Africa and significantly stepped up scrutiny after the collapse of African Bank in 2014, immediately expressed confidence in Capitec’s capitalisation and liquidity. S&P Global Ratings also announced that it saw no reason to change its credit rating of Capitec. Viceroy, is a small firm whose outsized impact on local market sentiment stems from it having successfully shorted Steinhoff (a short seller bets on falling share prices).

Listed property companies are also classified as financials although most local investors consider it as a separate asset class. The 9.9% slump in the SA Listed Property Index in January contributed to the weak month for financials. Companies in the Resilient stable - Resilient, NEPI Rockcastle, Greenbay and Fortress - suffered sharp losses of between 15% and 30%. The reason appears to be speculation that it might also be a target of overseas short-seller.

Looking ahead, three factors are likely to drive returns from local equities. Firstly, global markets will set the pace and the JSE will move up or down with global risk appetite, and particularly sentiment to emerging markets. Secondly, the JSE is dominated by large rand-hedges, meaning that if the rand continues to appreciate (i.e. the dollar continues to weaken), it is likely to put downward pressure on returns at an index level. Finally, domestically focused shares will depend on the extent to which the domestic economy recovers in line with the global upswing. Political and economic reform can support this recovery by boosting consumer and business sentiment. There are promising signs. The first post-Nasrec survey showed the Absa Manufacturing Purchasing Managers’ Index (PMI) rising to 49.9 index points in January. This is the best reading since May 2017, but still lagging its global counterparts by some distance. However, the sub-index measuring expected future business conditions jumped to the highest level since 2010, suggesting much greater confidence.

A time to keep calm

The sudden jump in market volatility and equity sell-off late last week should be seen as a re-pricing of interest rate expectations. After a strong surge upwards over the past couple of months, a correction is pretty normal and not entirely a bad thing. The economic fundamentals remain solid and this means companies can still grow profits, which is what long-term investors should care about. Short-term moves are usually driven by sentiment. Now is the time to keep calm and focus on the underlying picture that is actually quite healthy.

Chart 1: 10-year government bond yields for major economies

Source: Datastream

Chart 2: Global equities in US dollars

Source: Datastream

Chart 3: JSE main sectors

Source: Datastream