When patience meets politics

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

“It’s the economy, stupid” was the mantra of Bill Clinton’s 1992 election campaign. He beat incumbent president George Bush largely because of this focus at a time when the US slipped into a brief recession. James Carville, the Clinton adviser who coined the phrase, is also known for saying that, if reincarnation existed, he would like to be reincarnated as “the bond market” because it can “intimidate everybody”.

Things are quite different now, obviously. For one thing, it seems to be a case of “the politics, stupid”. Political uncertainty is dominating global markets in a way that it hasn’t in years. At least, that is what it feels like at the moment. A quiet week on markets was rudely interrupted when US President Donald Trump announced that an additional $200 billion of Chinese imports would be subject to tariffs. This is over and above the tariffs on $34 billion of imports that came into effect earlier this month. China has so far retaliated against US tariffs dollar for dollar, but it doesn't import enough to match the new tariffs announced last week.

Investors are becoming increasingly concerned over the tit-for-tat tariff increases, but so far all threatened and implemented tariffs apply to only 5% of global trade. The backlash inside the US over Trump’s tariffs - including from within his Republican Party and its large corporate backers - should prevent extreme outcomes. The uncertainty created is still a bigger risk to global growth than actual tariff increases.

Still, New York-listed S&P 500 companies are expected to report second-quarter earnings 20% up from a year ago in the coming weeks.

Brussels, Brexit and Brazil

There was more geopolitical angst at the NATO summit in Brussels after President Trump hinted he would pull out of the North Atlantic alliance, which has been a cornerstone of peace and security in the Western world for 70 years, unless European nations increased military spending.

Meanwhile, the carnival of chaos that is Brexit rolled on, with two Cabinet ministers resigning in protest to the adoption of a ‘soft’ Brexit proposal that would aim to retain UK access to the European common market. This could lead to the collapse of Theresa May’s government and even fresh elections, only months before the UK officially leaves the European Union (and at this stage sorely lacking a Plan B).

In Turkey, the lira is back at record lows against the dollar, after newly re-elected President Tayyip Erdogan appointed his son-in-law as finance minister and said he expected interest rates to fall. The Turkish central bank is caught between constant political pressure to cut interest rates on the one hand, and fighting rising double-digit inflation on the other.

Brazil’s real is also close to record lows as the country faces its own political uncertainty. The most popular candidate for the looming October presidential election – former president Lula da Silva – is currently in prison for bribery and might not be allowed to stand.

Not intimidating

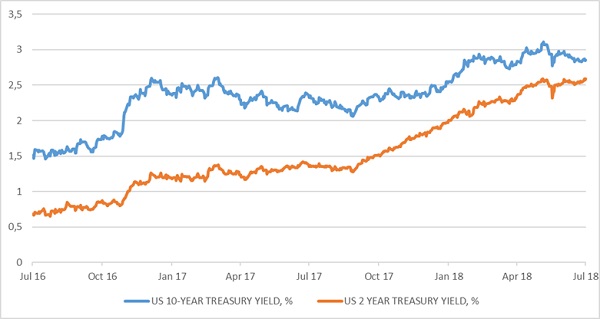

At the same time, the mighty bond market has been quiet. After surging above 3% amid much fanfare in May, the US 10-year government bond yield – the global benchmark - is back at 2.8%. While this is still up from 2.4% at the start of the year, the Federal Reserve has hiked interest rates twice during this period. In other words, short rates are still rising faster than long rates and the yield curve – the spread between long and short rates - is flattening. In fact, it is at its flattest rate since 2007. Rather than intimidating the US government into cutting its widening deficit, the bond market seems to be signalling nervousness that the Fed could be hiking too much.

Last week’s US jobs reports showed strong payrolls growth – 213 000 new positions filled in the month – as well as a slightly higher unemployment rate (4%). This is because a record number of job openings has drawn half a million previously discouraged workers into actively looking for work (the unemployment rate doesn’t count those not looking for work). This pool of previously excluded workers suggests the labour market is not as tight as it seems, and therefore upward pressure on wages and ultimately inflation is muted. This in turn calls for a very gradual pace of interest rate increases. There is a risk that new tariffs on Chinese imports could raise US inflation, but this will depend on a range of factors, including whether consumers switch to goods from other countries.

Returns despite politics

As South Africans, we are of course long used to politics influencing markets. Since South Africa’s birth as a state in 1910, politics has dominated economics and financial markets. Yet, the returns South African investors have enjoyed since then have been remarkable, with the JSE delivering average annual returns of 7% above inflation. This was despite the often traumatic political backdrop. However, these returns didn’t come in a straight line. The good times were interspersed with periods of weak returns. We’ve been in this kind of soft patch for the past while. This too shall pass.

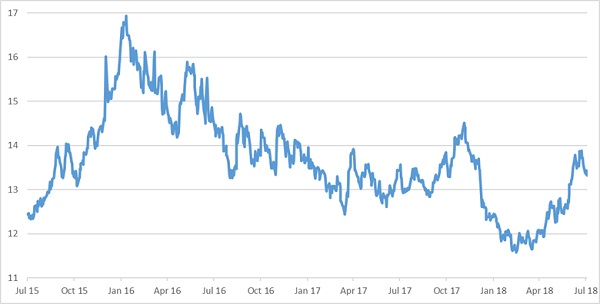

Nevertheless, the influence of local political uncertainty on markets is often overstated. We are fully integrated into global markets and take our cues from them. As a simple example, the rand has been a bit stronger over the past few days, and this has nothing to do with any political or economic developments over this time.

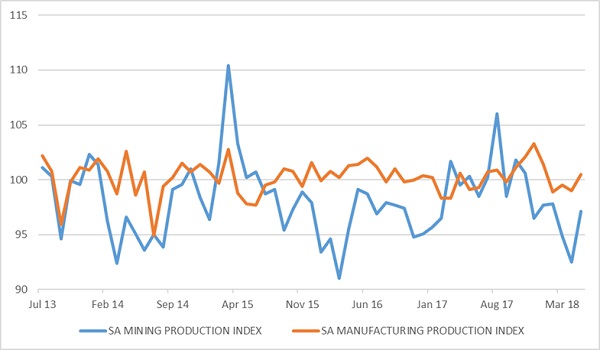

True, mining and manufacturing production both performed better than expected in May, and the second quarter average for both is above the first quarter. The two sectors combined constitute around 20% of the local economy and were both sharply negative in the first quarter. However, mining and manufacturing numbers rarely move the rand. Instead, it seems that trade data from far-away China was behind the currency’s appreciation, showing that the world’s number two economy was still growing its imports and exports at a healthy clip, dispelling fears of an economic slowdown.

This is important, because a sharp slowdown in the Chinese economy would probably do more damage to return prospects than a slowdown in the local economy. The latter remains stuck in a very low gear and the positive sentiment around President Ramaphosa’s arrival in the Union Buildings has been dealt a series of blows, including the uncertainty around land reform and, more recently, the surging petrol price. The sharp drop in the price of Brent crude oil in the past few days helps on the latter score, but policy certainty still appears to be some way away, unfortunately.

It’s the diversification, stupid

The bottom line is that the current environment is still uncertain. This calls firstly for appropriately diversified portfolios that do not bet on any single economic or political outcome, but that can do well in a broad range of conditions. For instance, taking a strong view on the rand in either direction is risky. Secondly, when there is uncertainty, there is market volatility. Volatility in turn can scare investors into selling out at the wrong time. Patient investing that avoids knee-jerk responses to bad headlines is crucial when it comes to generating sound long-term returns.

Chart 1: US 2-year and 10-year bond yields %

Source: Thomson Reuters Datastream

Chart 2: Rand-US Dollar exchange rate

Source: Thomson Reuters Datastream

Chart 3: Mining and manufacturing output indices

Source: StatsSA