US economy : Weakest performance in three years, supporting the forecast for lower-than-expected growth for 2017

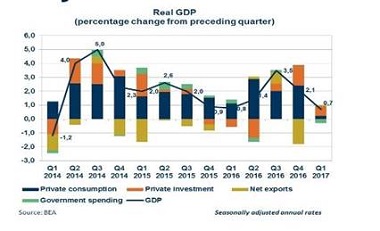

America’s economy grew by just 0.7% in Q1 2017 - at the seasonally adjusted annual rate (Saar) - vs. 2.1% in Q4 2016.

This was below consensus expectations of 1.0% to 1.2% and was the weakest performance since 2014. The deceleration in real GDP during the first quarter was mainly due to the slowdown in private consumption, which accounts for around 70 % of GDP.

Downturns in private inventory investment and in state and local government spending were partially offset by an upturn in exports and accelerations in both non-residential and residential fixed investments.

Private consumption recorded its weakest performance since 2009. Consumer spending, the lion’s share of the economy, rose by just 0.3 % Saar in Q1 2017, compared to 3.5% in Q4 2016 and 1.6% for the same period last year. It was the weakest performance since 2009. Weak auto sales and lower home-heating bills dragged down consumer spending, offsetting a pickup in investments led by housing and oil drilling.

Private investment (residential and non-residential) was the main growth driver during the first quarter, while contributions to trade expansion were slight. Within the scope of private non-residential investments, spending on equipment advanced by 9.1 % (compared to 1.9% in Q4 2016).

Investments, including office buildings and factories, surged by 22.1%, after dropping by 1.9% in the previous quarter. Trade added to growth, as exports increased by +5.8% in first quarter (-4.5% in Q4 2016) and at a faster pace than imports, which grew by +4.1% (+9.0% in Q4 2016).

Government spending was weak. It fell to -1.7% in Q1 2017, compared to the +0.2% increase recorded in the final quarter of 2016. State and local outlays fell by 1.6%, while spending by federal agencies dropped by 1.9%.

Risks

These GDP results will make it tougher for the Trump administration to respect its promises of a higher level of expansion in 2017. The disappointing figures suggest that despite the increase in short-term confidence indicators for households and businesses, this has not, as yet, been able to strengthen economic activity. These preliminary results confirm Coface's forecasts for weaker than-expected growth for the US economy.

Coface forecasts a US growth of 1.8% for this year as market prospects which expects between 2.2%-2.5% growth for 2017. In addition, a series of rises in interest rates by the Federal Reserve is expected for this year. This will probably affect consumption further over the coming months. After raising its benchmark rate by 25 basis points in March, from 0.75% to 1%, the Fed keeps its monetary policy unchanged on May 3. However, the Fed is expected to hike rates again in June. Higher interest rates will increase the payments made by Americans who are repaying mortgages, auto loans and credit card purchases – which will reduce their purchasing power.

The positive impacts of tax reforms on GDP growth remain unclear and are not expected to be seen in 2017. Trump’s administration recently announced its proposed outlines for tax reforms. The plan contained few details and will be refined over time, through negotiations with Congress. The plan proposes the cutting of corporate taxes from 35% to 15%, in order to encourage companies to invest in the US. It also aims to change the personal tax code, mainly by lowering the highest personal rate from 39.6% down to 35% and to allow personal revenues derived from privately owned companies to be taxed at 15%.

The White House seems convinced that tax cuts would create a virtuous circle of growth for the US economy - but has not given details on how the tax reforms would be financed. According to the Committee for a Responsible Federal Budget (CRFB), these tax reforms would cost $5.5 trillion (base-case estimate) – or 20% of GDP in revenue losses over 10 years. Given the shortfall expected in the US Treasury and the Republican aversion to widening public deficit, it seems that Trump’s proposal is already faced with headwinds.

Furthermore, both the House and the Senate are continuing to work on their own tax reforms, which mean that the process of combining ideas from all proposals is likely to be longwinded.

The results of negotiations surrounding tax reforms remain highly uncertain and the US economy is unlikely to benefit from them this year. The same is true for the plans to revitalise the country’s infrastructure particularly with regards to details on financing and timing.