US economy and markets: what's the state of play as Trump takes office?

George Brown

David Rees

James Bilson

Duncan Lamont

Bob Kaynor

As President Trump begins his second stint in the White House, Schroders' investment experts consider the current state of the US economy and the stock and bond markets.

With Donald Trump taking office, investors need to pay attention to which campaign trail promises become policy priorities. This will have implications for the economy, equities and bonds. Below, our experts consider the current state of play and lay out what they are watching most closely.

US economy resilient, but stagflation is a risk

Many investors went into 2024 worrying about a US recession, but that did not materialise. Heading into 2025, Senior US Economist George Brown says, “We continue to find market expectations for the US economy too pessimistic. The consumer is in good shape and, with the labour market cooling rather than collapsing, household spending should continue to drive growth. US GDP numbers for Q3 2024 were revised up, and Q4 looks to have been pretty solid in terms of growth.”

The Schroders Economics Team forecasts US GDP growth of 2.5% for 2025, accelerating to 2.7% in 2026. This would see inflation remain higher than previously assumed, with the Federal Reserve (Fed) cutting rates once in 2025 before hiking in 2026.

These forecasts are predicated on certain assumptions around Trump’s policy agenda. “Slim Congressional majorities should limit Trump’s more extreme inclinations but still be sufficient to extend his expiring tax cuts and support his deregulatory efforts,” explains George Brown. “And while we do expect he will implement protectionist policies, we are sceptical they will include a universal baseline tariff. Likewise, we suspect his efforts to expel illegal immigrants may not reach the promised scale of 20 million.”

However, if Trump were to implement his stated policy agenda in full, the implications for the US economy could be rather different. The Schroders Economics Team has also modelled a more aggressive scenario that includes 60% tariffs on all Chinese goods, plus tariffs on the rest of the world, alongside strict immigration limits and deportations.

If that scenario comes to pass, George Brown says, “Weaker trade, a pause in investment decisions and a general shock to confidence would be likely to tip most economies around the world towards recession and lead to significant interest rate cuts.

“But this mix would have more of a stagflationary impact for the US. In other words, while the US’s growth outlook is also diminished under an aggressive Trump scenario, slower growth would be accompanied by more, rather than less, inflation. An aggressive Trump may try to deliver large fiscal stimulus, but stronger demand would quickly run into a deteriorating supply side of the economy. GDP growth would probably slump in the first instance due to huge disruption, before receiving some boost from stimulus measures heading into 2026.”

A key difficulty for investors is assessing the likelihood of any given policy being implemented, and this difficulty will continue until clarity on policy direction emerges. David Rees, Senior Emerging Markets Economist, says, “Financial markets could price in any of these policies during the course of 2025, even if they never actually come to fruition, leading to increased volatility across asset classes.”

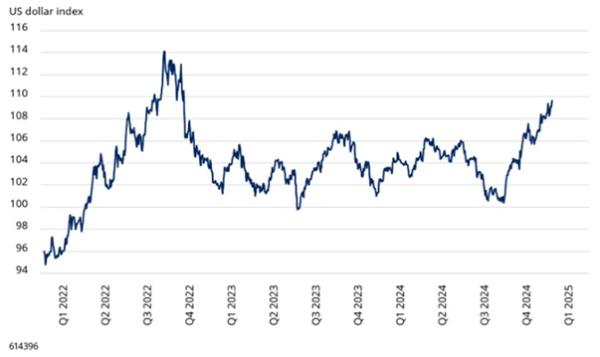

Inflation outlook contributing to dollar strength

Multiple factors combined to send the US dollar higher at the end of 2024. These factors included expectations of higher interest rates in the US relative to other major central banks, as well as higher US growth compared to other regions.

Dollar index close to two-year high

Source: FactSet, as at 10 January 2025. The US dollar index is a measure of the value of the US dollar relative to a basket of foreign currencies. Past performance is not a guide to future performance and may not be repeated.

Policy on trade will also have a significant influence on the dollar. David Rees says, “Any imposition of tariffs would tend to be supportive of the dollar because it would go some way towards equalising out the impact of tariffs on trade and activity. We also expect support from interest rate differentials to re-emerge, so a stronger dollar is likely to remain for a while longer.”

But the dollar could see some swings before policy on trade is confirmed by the incoming administration. An example is the recent leg down on the chart above in early 2025, which came amid reports – later denied - that trade tariffs could be applied more narrowly than feared.

Fiscal outlook holds key to bonds

Fixed income markets have also seen some significant recent moves, as investors price in the likelihood of Trump’s policies and their potential impact on inflation and interest rates.

James Bilson, Fixed Income Strategist, says, “Heading into the second Trump administration, bond markets have been repricing higher in yield due to a combination of strong growth, stickier recent inflation prints and expectations for further reflationary policy under a new government. Bonds now price between one and two 25-basis point (bp) Federal Reserve cuts for 2025, having priced more than four as recently as September.”

Click here to read more...