The rocky road to recovery

South Africa’s economic recovery is rightly in the spotlight, and important questions need to be asked. We need to know not only how we bounce back from the lockdown-induced contraction but also how we raise the longer-term economic growth rate.

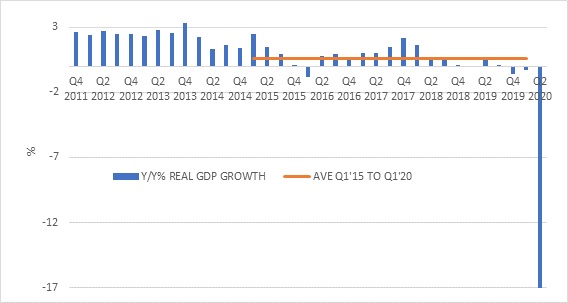

After all, real economic growth averaged only 0.6% in the five years prior to the pandemic. That was below the rate of population growth, suggesting that income per person declined.

In other words, we need to be considering how to get faster growth on both a cyclical and a structural basis. If we think of the economy as a car, the cyclical performance is determined by how hard the accelerator or brakes are applied. However, the structural performance is about how fast it can run without the engine seizing up or overheating.

The better the engine, the faster it can run over time without giving problems. An engine that is not properly maintained will lose its potential speed over time. That is the problem in South Africa. The economy’s engine lost its potency even before Covid-19 slammed on the brakes in the second quarter.

Chart 1: South Africa real economic growth

Source: Stats SA

Of course, the brakes have been lifted and the car is back on the road in the third quarter. Data is still limited, but there are encouraging signs. Mining production continues to recover strongly. Stats SA’s index of production is almost back to pre-pandemic levels. The seasonally adjusted value of mineral sales hit an all-time high in August, thanks to a weak currency and elevated commodity prices. Real retail sales were still 4% lower than a year ago in August, but almost double the level in April. Manufacturing production was still 11% below where it was a year ago in August but posted positive growth every month since May. Although agriculture is a small sector, bumper maize and wheat crops as well as record citrus exports mean it will also make a positive contribution to the recovery.

Ingredients for a positive surprise

This largely represents bouncing off a very low base and will not necessarily be sustained. Yet we also need to acknowledge that expectations are so low that there is scope for a positive surprise. This requires four ingredients.

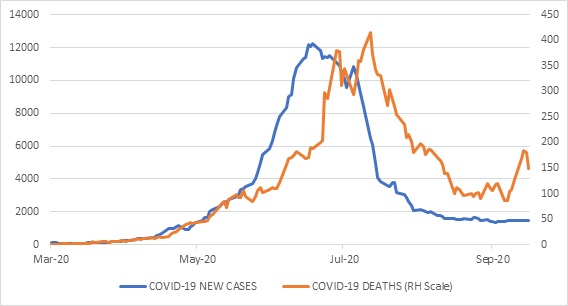

Firstly, the coronavirus needs to remain more or less under control. A return to lockdown level 3 or 4 would be devastating. Even if government regulations did not change, consumers could still opt to stay home and spend less if the outbreak picked up speed again. Whether by luck or design, so far the daily growth in confirmed cases has remained broadly stable since September. So far so good.

Chart 2: Covid-19 in South Africa

Source: Refinitiv Datastream

The second ingredient is a favourable global environment. On this score there is some good news. The global economy is picking up speed again, though this too is at risk of second wave outbreaks. The International Monetary Fund‘s latest forecast shows contraction of 4.4% this year. This would be a somewhat better outcome than initially thought. Next year, global growth of 5.2% is predicted as activity improves off a low base. The pace of growth is likely to taper off in subsequent years. Continued fiscal support will be key, especially in the US.

Markets have been getting increasingly excited about the prospect of a ‘blue wave’ election victory for the Democrats that could lead to substantial government spending and infrastructure investment in the world’s largest economy. Importantly, though, the Federal Reserve has pretty much promised to keep interest rates glued to the floor. This should help emerging markets like ours.

Commodity prices have also been fairly robust, despite the declines in economic activity. The notable exception is oil, but that suits us just fine. The difference between our export prices and import prices - known as the terms of trade – is thus very much in South Africa’s favour. A shift towards a green economy will still require commodities, just a different mix. Less oil and coal, but more materials for batteries, for instance. Unfortunately, tourism is not an avenue through which we can benefit from better global growth at the moment.

Cyclical support

The third ingredient is policy support. The Reserve Bank has already gone as far as it is prepared to go in terms of interest rate cuts, though low inflation means it can keep rates where they are for some time. Interest rate changes typically impact the economy with lag of around 12 months, but there are already anecdotal reports of a fairly robust local property market, or at least in certain pockets. This would mirror the trend in other countries, where low interest rates and a newfound need for space have seen aggressive home-buying in suburbs.

There is very little scope for cyclical fiscal policy support, however, due to the fact that the government went into this crisis with a large budget deficit and rapidly rising debt. Any new borrowing to support the economy has to be done at extremely high interest rates. Unlike in developed countries, it is not clear that new borrowing will pay for itself. In fact, failure to reduce borrowing over time will lead to interest payments consuming an ever larger share of the pie. However, fiscal consolidation – cutting back on spending and raising tax revenues – tends to be a headwind to economic growth, at least in the short term.

Structural reform

The fourth ingredient is therefore implementing reforms to raise the growth potential of the economy, allowing the engine to run faster. This means unblocking bottlenecks, reducing the cost of doing business and other steps to enhance productivity. Some of the things that hold back the long-term economic performance cannot be fixed, such as the fact that South Africa is far from its main markets and that our major industrial centre (Gauteng) is far from a navigable water body, a fairly unique situation globally. Transporting goods by road is significantly more expensive than doing so by ship. This is a version of what in Australia became known as the ‘Tyranny of Distance’. It also applies to our cities, where the poor tend to live furthest away from economic opportunities, largely excluding them from the formal economy. This is perhaps the most pernicious legacy of apartheid.

Some factors can be fixed only over long periods of time, such as improving education. Some bottlenecks exist due to neglect or simple bureaucratic bungling, but some exist because they suit certain interest groups. Economic reforms in most countries are limited by pushback from vested interests, ideology and state capacity.

South Africa is no exception, and therefore a joint sitting of Parliament set the stage for a potentially dramatic announcement. In the end the President’s Economic Recovery Plan did not contain much that is new. After all, it has been through various iterations and rounds of negotiations between government, business and labour. The fact that the Recovery Plan has been agreed to by a broad range of stakeholders is positive and increases the chances of its proper implementation. Such a plan was never going to make everyone happy. Still, some reform is better than no reform, and some progress better than none.

The Recovery Plan centres on four areas: a large-scale infrastructure roll-out; security of energy supply; provision of public employment opportunities and industrial development driven by sector master plans, including through localisation.

Of the four, expanded public employment opportunities and the extension of the special Covid-19 grant offer the most immediate stimulus to the economy. However, the employment plan is limited to R100 billion over three years, while the grants will only be paid for a further three months.

The other elements of the plan will only impact the economy over time, assuming that implementation goes according to plan (which is a big assumption). To illustrate the scale of the challenge, a new Stats SA report showed that the 123 provincial government departments recorded a decrease in infrastructure spending of R1,88 billion in the 2019 fiscal year, a 5% decline from a year ago. With budgets tight, and project and financial management skills scarce, capital expenditure is usually the first area where cutbacks take place. The involvement of private investors in funding and managing the key infrastructure projects is therefore crucial.

Raising growth rates

The Treasury estimates these interventions could eventually lift the underlying growth rate to around 3%, which would be a substantial improvement compared to the performance of recent years, but still well short of the much-vaunted 5% growth rate the National Development Plan hoped to achieve.

Potentially game-changing interventions such as privatisation and more flexible labour laws seemingly remain out of reach. The President did, however, offer the possibility of eventually listing some of the better performing SOEs, which would certainly attract a lot of investor attention.

Importantly for investors, the President reiterated the commitment to fiscal consolidation, though the details will have to wait for the rescheduled MTBPS next week. Faster growth over time is a vital ingredient of restoring fiscal sustainability over time.

There has been a huge, justified outcry over corruption. The President rightly devoted a substantial portion of his speech to highlighting progress in the fight against corruption. Crucially, he stressed it would be free of political interference. While the perception of out-of-control graft has contributed to declining business confidence, we must not forget that corruption per se does not preclude economic growth. Corruption is prevalent across fast-growing emerging markets. It is where corruption distorts policymaking and interferes with delivery – state capture, in other words – that it is extremely harmful to the economy. We do appear to have turned a corner on this front.

Investment scenarios

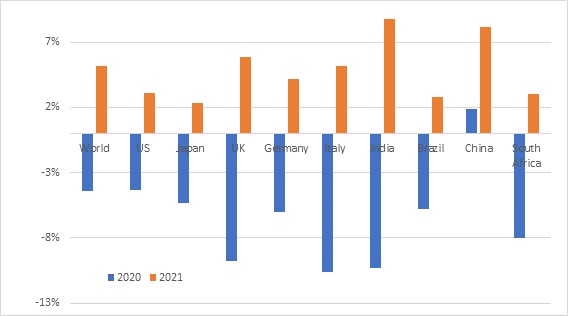

Back to the present. The IMF expects a record 8% contraction in South Africa in 2020. This is worse than total world growth, but in line with some major economies including India, Mexico, the UK and Italy. The forecast growth for 2021 of 3% is largely just a rebound off the low base. The big question for investors is what kind of growth rate is possible from 2022 onwards when the pandemic is hopefully something of the past and some level of normality has returned.

Chart 3: IMF real economic growth forecasts, %

Source: International Monetary Fund

All local asset classes should benefit from sustained faster economic growth in South Africa, apart perhaps from money market and cash-plus products. A stronger economy could result in upward pressure on short-term interest rates, though this might be offset by tighter credit spreads.

Bonds have historically been a defensive asset and therefore sell off as the economy recovers. However, South African government bonds in the current situation would greatly benefit from faster growth as more tax revenue would reduce the government’s reliance on debt. With long bond yields where they are, the potential returns are exciting, but this needs to be balanced with the substantial risks that remain.

While equities is traditionally the asset class geared most directly to economic growth, the preponderance of rand-hedges on the JSE means overall performance could be mixed, if the rand responds favourably to stronger growth. Cheap domestically focused companies would deliver strong returns in such an environment.

Property is also geared to the performance of the economy. However, the contractual nature of the underlying rental incomes means they tend to lag in a recovery. The local listed property sector is also not particularly local anymore, with large exposure to especially Eastern Europe. Across the world, there are questions over the future of shopping malls and office buildings.

It has become a national pastime of sorts to write South Africa off. Although the political and policy changes underfoot will not address all or even most of our problems, they can address enough of them to change the country’s direction. We may never be a Singapore or South Korea, but we won’t end up a failed state either. A virtual cycle of rising business confidence, investment and job creation is possible under the right conditions. This is not a forecast, but a scenario, and investors should consider all possible scenarios and diversify accordingly when constructing portfolios.