The Guns of August

The first half of the year saw a rebound in global equity markets, led by the US, despite the fact that the global economy was clearly cooling. Investors were buoyed by the apparent progress in the US-China trade negotiations, and found comfort in the fact that central banks were acting to cushion the fallout. However, the events of August have shaken these beliefs.

Trade war resumes

On the first day of August, US President Trump stunned investors by imposing 10% tariffs on the Chinese imports not yet taxed (goods worth around $300 billion per year). Equities sold off heavily and investors piled into bonds, driving yields lower. Two weeks later, Trump postponed the implementation of some of these tariffs to prevent a price jump ahead of festive season shopping. This calmed nerves for a few days, until China retaliated by increasing tariffs on $75 billion of US imports. This was not entirely unexpected, and the Chinese argued that it was proportional to the earlier US action. President Trump’s response was severe and seemingly erratic. He not only hiked tariffs on all Chinese goods, but took the further step of ordering US companies to cut ties with China, something he is not entitled to do. This predictably spooked equity markets.

In the past few days, both sides made tentative noises about resuming talks, but it is clear that the genie is out of the bottle now. The world economy will have to function with higher tariff levels and more trade impediments for the foreseeable future. This impacts firms not only in the US and China, but all participants in the complex global supply chains. For instance, SUVs made in the US for export to China by Germany’s BMW and Mercedes are now subject to 25% tariffs. If implemented, this latest round of threatened increases would leave tariff levels at uncomfortably high levels. But the biggest impact is still on business confidence. Given the uncertainty, companies might hold back on hiring and investment decisions.

New York Times columnist Paul Krugman, who won the economics Nobel Prize for his work on international trade, made the point that there have been examples of countries in the past that combined high tariffs with full employment. However, unstable and unpredictable trade policy is a different matter. “If your business depends on a smoothly functioning global economy, Trump’s tantrums suggest that you should postpone your investment plans; after all, you may be about to lose access to your export markets, your supply chain or both.” Even companies not directly impacted by trade could adopt a cautious stance. In this way, the trade war can spill over into the healthy consumer-facing sectors of the economy.

Hope is not a strategy

At this stage, it doesn’t make sense for anyone to hope that there will be a resolution in the short term and a ceasefire is the best we can hope for. The Chinese government might even want to drag it out until after the US presidential elections on 3 November 2020, in the expectation that they will be negotiating with a more rational and pragmatic Democrat. Ironically, it has traditionally been the Republicans who are pro-business and pro-free trade. Indeed, several of the leading Democratic presidential candidates have placed the taming of the power of big corporations and global capital high on their agendas. The unnecessarily long campaign between now and next November could be one of the most eventful ever as far as markets are concerned. Even if Trump loses, he will still be in office until 20 January 2021, with full presidential authority, nursing his wounds. If he wins, it’s potentially four more years of trade wars. The impact of political developments on markets is usually overstated, but these days it cannot be ignored.

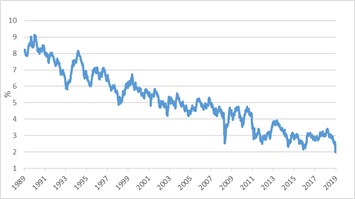

Chart 1: 30-year US Treasury yield, %

Source: Refinitiv Datastream

Many investors piled into the perceived safety of bonds. The benchmark 10-year US Treasury fell sharply from 2% to 1.5% during August (bond yield and prices move in opposite directions). It ended the month with a lower yield than much shorter-dated bonds, leading to a so-called inversion of the yield curve, an event that has in the past preceded a recession. The yield on US 30-year Treasury fell below 2% for the first time ever, suggesting investors expect the Fed to undershoot its inflation target for the next three decades. Meanwhile, a record $17 trillion in global bonds trade at negative yields, including every single bond issued by the German government. The collapse in bond yields does not just reflect the market’s expectation of future rate cuts, but also the market’s concern that such cuts will not be enough to offset the negative impact of the trade wars. Amid this fear, many investors clearly care about return of capital rather than return on capital.

Currency wars

Despite the decline in US yields, the dollar remains supported by the decline everywhere else. Bank of America Merrill Lynch estimates that 95% of all the positively yielding investment grade government and corporate bonds in the world are American. The Chinese yuan took a big hit, losing 4% in the month and falling to an 11–year low. Other emerging markets also slumped in the face of a stronger US dollar. The rand lost 6% to end the month at R15.18. The Brazilian real also lost 8% against the dollar in August, while the Indian rupee, Russian ruble and Turkish lira all lost between 4% and 5%. Over the past year, the rand became 3% weaker, boosting the return from global assets for local investors. For now, there is no sign of any major country, including China, trying to manipulate its currency lower to gain a trade advantage. But the risk is there, and it could lead to further instability.

The big guns

The most important central banks have key policy meetings this month and how they respond to the current climate will probably set the tone for the rest of the year, as markets are clearly pricing in a lot of policy easing. For the US Federal Reserve (Fed), the one challenge is that it characterised its July cut as a tweak in its stance, rather than a major shift. It has to cut rates without looking like it’s panicking. The other challenge is that it has not in the past wanted to wear the mantle of central bank for the world. Under Jerome Powell, it has become more focused on its global role, and the risk that global weakness hurts a US domestic economy that is still in good shape. For the European Central Bank (ECB), the challenge is simply the lack of room to ease. It is running out of bonds to buy (particularly since Germany runs a surplus), and rates are already negative. The Bank of Japan also has negative rates. Its problem is the surge in the safe-haven yen, which puts even more downward pressure on inflation. In short, central banks are acting to offset economic weakness, but they are far from omnipotent and there are limits to what lower rates can do.

Equities shell-shocked

All the above concerns, fears and unknowns hit the equity market hard. The S&P 500 lost 2% in August, but its 16% year-to-date return is still impressive. US markets continue to lead the rest of the world. The MSCI Emerging Markets Index declined 5% in the month, with about half the loss from currency weakness against the dollar. The local equity market took a hammering. The 2.4% decline on the FTSE/All Share Index means the year-to-date return is now 6%. Unfortunately, the weaker rand did little to support the market in the face of a global sell-off, though the six Top 40 shares that were positive in August were all rand-hedges (three precious metals miners, NEPI, Bidcorp and British American Tobacco). Over twelve months, the local market is down 3%. This is partly due to August 2018 being a particularly strong month, with the All Share briefly hitting 60 000.

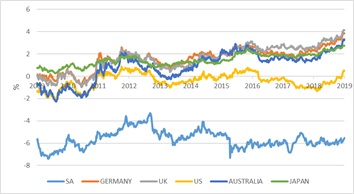

Chart 2: major equity indices, rebased to 100

Source: Refinitiv Datastream

That is all in the past now. Global investors positioning for the future are faced with the problem that fixed income yields are truly historically low, offering poor returns in most scenarios where the world economy does not completely collapse. Despite the many potential geopolitical risks, if things just bumble along as they are doing now, equities should outperform bonds. The link between interest rates and equities are fourfold: firstly, companies borrow, and lower borrowing costs save money. We’ve seen a number of local and global companies struggle with high debt levels; lower borrowing costs would help. Secondly, companies’ customers also borrow, and benefit from lower rates. Thirdly, a share price should in theory reflect the discounted value of future profits. An assumed lower discount rate (interest rate) raises the present value of those future earnings. Lastly, if one asset class becomes less attractive in its own right, others become more attractive on a relative basis. In most major markets, the dividend yields are above bond yields. Unless there is a deep economic slump and companies are forced to cut dividends, investors can therefore earn a higher stable income from equities than bonds. The balance of risks does not argue for increasing exposure to equities, just to maintain an appropriate allocation.

Chart 3: Dividend yields minus 10-year government bond yields in local currency

Source: Refinitiv Datastream

In South Africa, the dividend yield on the FTSE/JSE All Share of 3.3% is elevated relative to its own history and offers value, even assuming that some companies will cut dividends (as Woolworths did last week). But it is still below bond and cash yields that are simply very high - and attractive - in a global context and has shifted dramatically lower in the past month. All the global uncertainties discussed above as well as the local risks are understandably unsettling to many, but there are also risks in hiding away in a single asset class. The key is to have an appropriately diversified portfolio that is not dependent on a single macro scenario playing out, but can deliver in many different possible future states of the world.