The dollar dilemma

Dave Mohr, Chief Investment Strategist at Old Mutual.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

The post-US election rally on global equity markets continues. The Dow Jones Industrial Index hit 20 000 index points to much fanfare, but professional investors pay little attention to the Dow since it is weighted by share price, not market capitalisation. The S&P 500 also hit record highs, buoyed by the prospects of higher profits thanks to President Trump’s proposed tax cuts, a more solid global economy (which predates the election) and rising inflation, which supports corporate pricing power. Locally, the JSE All Share Index has also performed well since the start of the year, in contrast to January 2016 when global and local markets were experiencing turmoil. This means that the 12-month return on local equities is looking very healthy for the moment.

In contrast, the post-election equity rally in the US dollar has fizzled. In the first few weeks of 2017, the greenback has lost ground against the euro, yen and even the struggling British pound. The court ruling that Britain’s exit from the European Union has to be approved by Parliament (who would presumably inject more rationality into the process) lifted sterling from multi-decade lows. The rand has also strengthened against the US dollar since the start of the year, briefly touching a 17-month high last week.

Rates unchanged

Against this backdrop, there were no surprises from the South African Reserve Bank’s Monetary Policy Committee (MPC) meeting last week, with the repurchase (repo) rate left unchanged at 7%. This was despite the most recent inflation data increasing to 6.8% instead of declining as expected. This was largely due to stubbornly high food inflation. Better rainfall and larger-than-expected crops should eventually put downward pressure on food inflation. Exchange traded maize and wheat prices have already declined significantly.

Sticky food inflation and a 20% increase in the oil price since the OPEC agreement late last year resulted in the Reserve Bank raising its inflation forecast for 2017 quite substantially from 5.8% to 6.2%. The petrol price will increase by 29 cents per litre on Wednesday. However, as it noted, there is great uncertainty over whether OPEC members will stick to the agreement. North American shale producers certainly won’t. The core inflation forecast (which excludes food and fuel) was unchanged.

Inflation expectations declining

The MPC doesn’t only consider its own forecast, but also inflation expectations. The logic of inflation targeting is that expected inflation influences actual inflation. For instance, a landlord expecting 6% inflation will increase rent by at least 6%. If people are convinced that the central bank is serious about achieving its inflation target through the painful method of interest rate hikes, they will eventually accept that actual inflation will be close to the target (if the central bank loses its credibility and perceptions of its independence, this process won’t work). Surveyed expectations of future rates among unionists and the general public have finally fallen below 6%. This is a small victory for the South African Reserve Bank (SARB), which is aiming for inflation expectations closer to 4.5%, the mid-point of the target range. Wage settlements are another test for the inflation targeting regime since it should reflect inflation expectations as well as labour market dynamics. Above-inflation wage increases in the face of high unemployment have long been a source of concern for the Reserve Bank. However, wages per worker grew at the slower rate of 5.8% year-on-year in the third quarter.

On the growth front, the latest available data suggest that fourth quarter economic growth may be negative, capping a miserable year. This year is likely to be better, with the SARB forecasting 1.1% gross domestic product (GDP) growth this year and 1.6% in 2018. The Reserve Bank’s composite leading, which points to changes in economic activity a year or so ahead, increased to the highest level in 18 months, after hitting a seven-year low in April.

Our Reserve Bank wasn’t the only central bank in action last week. Turkey’s central bank hiked the overnight lending rate, but left the benchmark repo rate unchanged, raising fears of central bank independence. Turkey’s increasingly authoritarian President, Recep Erdogan has criticised higher interest rates. While the rand has been strengthening since hitting a record low in late January 2016 (and further this year), the lira plunged by 30% over the past 12 months and is the worst-performing major currency this year. Partly as a result of the weak currency, Turkey’s inflation rate was 8.5% in December, against the central bank’s target of 5%. Turkey’s problems are compounded by the large foreign currency-denominated debts of its corporate sector, a burden that can potentially balloon (depending on how prudently these companies have hedged). South African companies have little need to borrow abroad since there is ample local funding available at reasonable interest rates. Foreign currency borrowing is typically done to fund acquisitions and operations abroad, in which case the resultant income stream is a hedge against currency weakness.

The problem dollar

For South Africa and Turkey (and the rest of the emerging world), the key to the interest rate outlook lies in Washington DC. The risk is that the combination of interest rate increases from the Federal Reserve (the Fed) and fiscal stimulus from a White House under new reign may cause a stronger dollar, as was the case under President Reagan in the mid-1980s. This in turn could put pressure on vulnerable emerging market currencies, resulting in inflation and central banks being forced to act (as in 2014 and 2015). “It is our currency, but your problem” as President Nixon’s Treasury Secretary, John Connally, famously told a nonplussed group of European finance ministers. But a strong dollar could also be America’s problem by hurting its exporters, and counteracting Trump’s plans to revive manufacturing. For instance, the Mexican peso has already lost 20% against the US dollar over the past year, largely offsetting any planned tariffs on Mexican imports.

The consensus view among forecasters and commentators is that the dollar will strengthen further but there are reasons to be sceptical. If stronger US growth is as a result of fiscal stimulus, we could quickly return to the ‘twin deficit’ problem of high budget and trade deficits that weighed on the US dollar prior to 2008. What about higher interest rates? Since the Fed is trying to communicate its intentions as clearly as possible, its planned rate increases are largely priced in already. It is only if the Fed hikes faster and further than currently expected that the dollar should react by strengthening. Part of this equation is also what other central banks (notably the European Central Bank and Bank of Japan) do. The assumption is that they will keep policy loose while the Fed tightens, but the ECB in particular will come under pressure from its German board members to tighten policy as inflation moves towards its 2% target. European bond yields increased to the highest level in a year last week, narrowing the gap with American equivalent bonds amid a better growth and inflation outlook for the Eurozone.

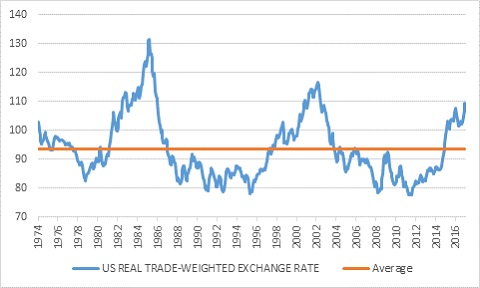

The most compelling argument usually is the valuation case, and the dollar is already expensive, increasing by 30% on a real trade-weighted basis since 2011. Chart 2, which runs until December 2016, shows how the dollar is well into the third historic bull market since Nixon abandoned the gold peg in 1971. A similar real exchange rate approach shows that the rand is still undervalued against the dollar compared to where inflation differentials suggest it should trade, but is more fairly valued against the pound and euro.

Rand important for investors too

The direction of the rand will not only impact the inflation and interest rate outlook, but will also influence returns from various asset classes for investors. But the rand is also unpredictable, and at the mercy of global capital flows, commodity prices, sentiment towards emerging markets and domestic economic and political developments. Given the inherent uncertainty, it is prudent to be appropriately diversified: some assets do well in a strong rand environment, and some benefit from a weak rand.

Chart 1 SARB composite leading economic indicator

Source: SA Reserve Bank

Chart 2: Real trade-weighted dollar

Source: Datastream