The Brexit reality: Britain votes to leave the European Union

Sanisha Packirisamy, Economist at Momentum Investments.

Voter turnout in Britain’s referendum on European Union (EU) membership was high at 72.2% (33.6 million ballot papers).

The final referendum tally

This was lower than the c.82% turnout for the Scottish independence referendum held in 2014, but higher than the c.66% voter turnout at Britain’s general elections in 2015 and the 64.6% turnout at the 1975 referendum on British membership of the then European Economic Community. Although Scotland, Northern Ireland and London voted in aggregate to stay within the EU, these votes were insufficient to offset a significant “leave” vote from Wales and pockets of England, resulting in the “leave” vote obtaining 51.9% of the final tallied votes.

Financial market reaction

The market’s initial response to the shock outcome has been decidedly negative, with the pound dropping to a thirty-year low against the US dollar. Equity markets also experienced massive risk-off moves, with the Nikkei down c8% and S&P futures indicating that the US market will open around 5% lower. Gold benefited from the risk-off sentiment, gaining around 6%, while emerging equity markets were negatively hit, losing between 3% and 6%.

During the period of elevated uncertainty under the Brexit reality, the “safe haven” assets will likely be US Treasuries, the US dollar, the Japanese yen, the Swiss franc and gold. A rising risk-off tendency puts all perceived risky assets under pressure – including equities, the euro, British pound, commodity prices, as well as emerging market (EM) currencies and assets.

The Brexit process

Today’s result does not imply that Britain is out of the EU immediately (see chart 1). The UK will likely remain inside the EU for at least two years (and possibly even longer) as the UK irons out its future trading relationship with the remainder of the EU and the rest of the world. But the outcome of the vote gives the British government the ability to invoke Article 50 of the Treaty of Lisbon which is the necessary legislation to begin the exit process from the EU. A negotiation period will likely follow. In Britain’s attempt to dissolve a 43-year partnership, over 80 000 pages of EU agreements will have to be renegotiated which could take between four and five years to finalise.

Chart 1: Exit process timeline

Source: RMBMS

UK and broader global economic impact

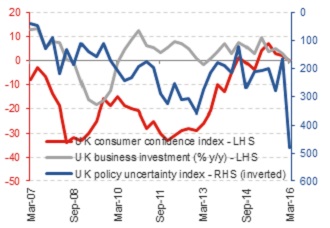

Political and economic uncertainty is likely to linger for some time, leading to a weaker GBP. As a result, UK businesses are likely to hold off investment and hiring, hence curbing growth (see chart 2). UK consumers are likely to feel the pinch as hiring intentions suffer and as inflation ratchets higher.

Chart 2: Rise in uncertainty has dampened consumer confidence and business investment

Source: Bloomberg, Momentum Investments

The Organisation for Economic Co-operation and Development (OECD) estimates that under Brexit UK GDP will be 3% below the level it would have been if the UK stayed in the European Union. It notes that every country in the EU would suffer a 1% growth decline. The OECD further estimates that financial shocks, as well as weaker European demand, could lower the level of GDP in the BRICS (Brazil, Russia, India, China, South Africa) nations and other non-OECD economies by more than 0.5% by 2018 as Brexit stirs global uncertainty among investors, businesses and consumers, resulting in negative consequences for global growth and the flow of global capital around the world.

UK trend growth is also likely to be negatively impacted as supply-side challenges (including a reduction in the size of the labour force through a possible lowering of net migration inflows) impact longer-term growth. The OECD suggests that UK GDP could be over 5% lower by 2030 than otherwise if the exit had not occurred.

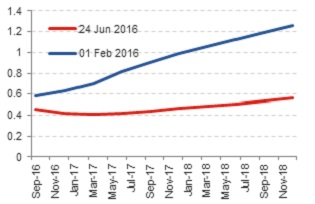

Central banks are likely to lean towards a more accommodative monetary policy stance in light of renewed market volatility and financial market instability. The US Federal Reserve is likely to delay the implementation of interest rate hikes even further in response to potentially softer growth, while the European Central Bank (ECB) and Bank of Japan (BoJ) could react initially via forward guidance. This is likely to be followed by further rounds of fiscal spending and monetary stimulus. Likewise, we expect the Bank of England (BoE) to exercise an easing bias in response to a weak growth outcome (see chart 3).

Chart 3: Futures pricing of interest rate hikes in the UK (%)

Source: Bloomberg, Momentum Investments

Anti-establishment sentiment gaining global momentum

The UK result is a further indication that a global “anti-establishment” attitude is gaining momentum. This is pointing to rising global protectionism sentiment (see chart 4), which results in a “beggar thy neighbour” attitude from voters and is a threat to globalisation and hence global trade flows.

Chart 4: Cumulative count of trade restrictions imposed by G20 (since 2010)

Source: Global Trade Alert, HSBC, Momentum Investments

Europe’s leaders have already expressed concern over the rise of populist anti-EU parties in their respective countries. With Spanish elections (June 2016), an Italian constitutional referendum (October 2016) and French (April-May 2017) and German elections (August-October 2017) on the horizon, European political risk remains high. Moreover, the Office for National Statistics concluded that there are around three million citizens of other European Union countries living in the UK, which amounts to c.5% of the country’s total population. This raises concerns that EU citizens may be forced out of the UK unless an agreement is concluded between Britain and the remaining member states stating otherwise.

Impact on SA economy

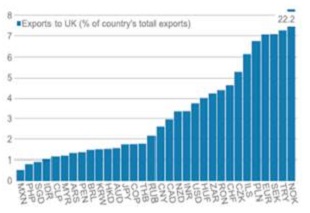

Although exports to the UK only constitute c.4% of SA’s total exports (see chart 5), the EU is SA’s largest trading partner (24% of the country’s total exports in 2015). The Brexit result will create uncertainty around the future of SA’s trade agreements with the UK and EU and likely put SA’s export growth and extended current account deficit at risk. Domestic sentiment is also likely to be negatively affected by the Brexit and could do further damage to the country’s already-fragile growth outlook.

Chart 5: Export exposure to the UK

Source: RMBMS

With mounting pressure on the domestic currency, the SA Reserve Bank’s stagflationary policy dilemma is likely to intensify. The Monetary Policy Committee may be forced to raise rates in spite of a weaker SA growth outlook should currency weakness persist. With SA’s headline inflation print likely to remain outside of the target band in upcoming quarters and inflation expectations remaining stubbornly high, any currency shocks could push inflation out of the target band for a more extended period of time.

Impact on SA financial markets

The rand as a liquid currency in a dissipating global risk appetite framework is likely to feel the selling pressure – particularly as SA’s large twin deficits are always exposed when global trade or capital flows are under threat.

While SA bonds and equities are both likely to feel the Brexit pain, at least the local equity market will be protected somewhat by the offsetting impact of rand weakness on the dual-listed shares, as well as on the companies with large offshore earnings bases.

Impact on Momentum Investments’ portfolios

The primary focus of outcome-based investing is to ensure all Momentum Investments' portfolios deliver on their intended outcomes with the highest probability of success, not losing sight of a strong risk-management focus embedded in portfolio construction and portfolio management. The entire range of Momentum Investments’ outcome-based portfolios are constructed with very specific goals in mind, expressed in terms of an investment outcome or objective, an associated term, as well as a predetermined risk budget or risk tolerance. The investment team’s portfolio construction process is focused on delivering on the above-mentioned objectives and remains grounded in the belief that a diversification benefit exists in the selection of differentiated asset classes, investment strategies or risk premia and that the implementation, by means of traditional or non-traditional mandates, will increase the likelihood of the company’s clients meeting their investment goals or objectives.

Momentum Investments’ portfolios are constructed and positioned to deliver on the robustness that clients have come to expect from an outcome-based investment philosophy and process over appropriate investment horizons. In the current economic and financial climate, the company’s portfolios have a well-balanced risk profile that are expected to provide the necessary market-linked exposure to benefit from further market gains, but also provide the necessary shock absorbers to help guard against unexpected negative market developments, such as the one experienced today. Examples of such dynamic structures and strategies include asset allocation flexibility, which, coupled with the investment team’s in-house-developed beta management programme, is constructed to quantify excess market returns and aims to identify risks from an asset class perspective.

In light of the above, Momentum Investments maintains a marginal underweight exposure to local growth asset classes, which include local equity and property. However, the company believes that maintaining a diversified strategy exposure in these asset classes will continue to benefit its portfolios despite unexpected market events and associated volatility. This is captured by way of a collection of risk premia identified to deliver alpha over the medium to long term. Momentum Investments has also identified various investment opportunities in the global equity market and has allowed its portfolios to participate in recent currency weakness. Where mandate allows, flexible fixed-income mandates are used where the investment strategies have favoured shorter-dated instruments that are less susceptible to changes in bond yields.