Shoppers not put off by politics

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

Another week, another Cabinet reshuffle, raising the already high level of political uncertainty. Announced only days ahead of this week’s mini-Budget, the timing is unfortunate, especially as there are suggestions that the reshuffle may be linked to a nuclear deal that would be as unaffordable as it would be unnecessary. While the rand wobbled on the news, the overall market reaction was fairly muted. Why? Firstly, as damaging as they are to the management of departments (there have been three energy ministers this year, while the communications department has had seven ministers since 2009), reshuffles are not a surprise to investors anymore. And it is surprises that move markets, not the known or expected.

Not surprised

The December 2015 reshuffle that saw Finance Minister Nhlanhla Nene lose his position came out of the blue and the rand, bonds and interest-rate-sensitive shares consequently slumped. The rand fell from R14.50 to R16 per dollar within two days, before the reappointment of Pravin Gordhan (another reshuffle). Potentially more damaging (as a weak rand has some benefits), the R186 government bond yield spiked from 8.8% to 10.5%, raising Government’s borrowing costs. But subsequent reshuffles, including Gordhan’s axing in March, which led to credit rating downgrades, saw a much smaller market reaction. They were not unexpected.

Secondly, much of the market adjustment happens in the background, where South Africa’s position shifts relative to other emerging markets. While most South Africans focus only on the rand exchange rate or the Government’s bond yield, investors should really consider how the rand and bonds perform relative to our peers. The additional yield over US bond yields that investors demand to hold riskier emerging market bonds is known as a spread. It is similar to how a bank might charge Customer A the prime rate plus 1% and Customer B prime plus 2%, depending on their credit profile. If the prime rate is hiked 1% but the bank decides that Customer B is actually not as risky and she should pay prime plus 1% instead, her overall borrowing cost will stay the same, but it will have improved compared to Customer A. South Africa’s spread has widened compared to those of Brazil and Russia (two countries we are often compared to) since the start of the year.

Favourable global backdrop

Thirdly, the global backdrop is favourable. When Nene was axed, commodity prices were collapsing, sentiment to emerging markets were at a multi-year low, and the US dollar was surging ahead of the first Federal Reserve rate hike in a decade.

The current global environment is supportive, and more forgiving of political own goals. Global equities have returned 17% this year as companies report strong earnings growth. Several benchmark indices (including the JSE All Share Index) are close to record highs. Emerging market equities have returned 30% in US dollars this year. Global economic activity has picked up momentum. Around the time of Nenegate, there were acute fears of a Chinese “hard landing”, accentuated by two devaluations of the yuan that spooked markets. Last week, China announced that its economy grew 6.8% year-on-year in the third quarter, well ahead of Beijing’s 6.5% target. While there is some scepticism around China’s GDP data, indicators such as retail sales and industrial production are reliable and also point to decent growth.

At the same time, global inflation is low and interest rates in the developed world are expected to increase very gradually. Meanwhile, after a tough period prior to last year, major emerging market central banks have started cutting interest rates. Global investors have been piling into emerging market bonds. Year-to-date, foreigners have been net buyers of local bonds to the amount of R70 billion. Foreigners have been net sellers of local equities this year, despite the JSE All Share Index hitting new highs. However, in US dollars, the JSE’s return this year is only half of that of the emerging markets equity benchmark.

Some good news locally

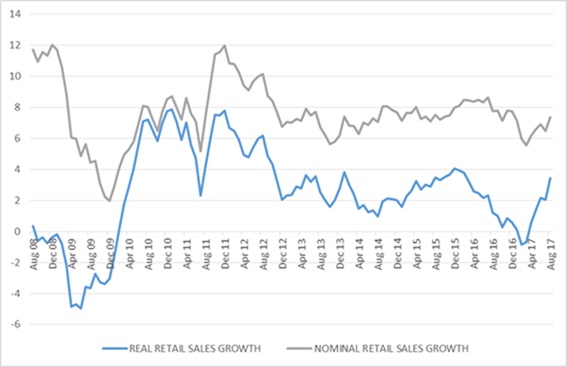

There is also some good news on the local economy. Third quarter data so far has been encouraging, starting with mining and manufacturing production, which is up strongly from the second quarter. StatsSA reported that retail sales grew by 5% in real terms in August from a year ago, the best performance since 2014. Retail sales momentum was greatly helped by lower goods inflation and the June rate cut. Growth also increased in nominal terms, accelerating to 9% year-on-year.

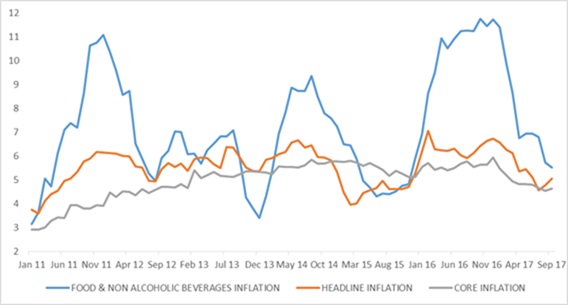

Headline consumer inflation, as measured by the annual change in the consumer price index, increased in September to 5.1% from 4.8%. The consumer price index measures the prices of both goods and services. The increase was largely due to a higher petrol price, but food inflation has declined.

Core inflation – excluding the impact of volatile food and fuel prices - picked up slightly to 4.6%, but remains well within the target range (as it has since 2009). The biggest component of core inflation is the category that measures actual rent, and owners’ equivalent rent (the rent that homeowners would pay to themselves). Actual and owners’ equivalent rent inflation rose from 5% in August to 5.7% and 5.4% in September respectively. However, this was largely due to rental inflation in the Western Cape increasing to almost 11%, while it only increased to 4.8% from a year ago in Gauteng, 3.6% in KwaZulu-Natal and 1.1% in Mpumalanga. (Interestingly, Limpopo posted the second highest increase in rents at 6%). In other words, it would be wrong to characterise the national housing market as overheated. In fact, it is struggling outside the Western Cape and is in need of a boost. A separate date release from StatsSA showed a 10% increase in the value building plans passed in the Western Cape for the first eight months of this year compared to last, but an 8% decrease in KwaZulu-Natal and a 12% decline in Gauteng (adding up to a 2.4% decline nationwide).

Reserve Bank still cautious

The Reserve Bank’s own forecasts point to inflation remaining within the 3% to 6% target in the coming two years, and therefore it can afford to reduce the repo rate further to support the nascent economic recovery. However, it currently places great emphasis on the risks to this outlook, the things that could potentially see inflation rising. One of these is Eskom’s application for a 20% tariff increase. The other bigger risk is that the political uncertainty – as evidenced by last week’s reshuffle – could further impede rational policymaking and fiscal management, leading to further downgrades and a slump in the rand as foreigners dump our bonds. A weaker rand in turn leads to upward pressure on prices (although the “pass-through” from exchange rate weakness to higher inflation has declined substantially, much to the surprise of the SARB).

This suggests caution from the SARB until after the December ANC elective congress. Its caution is bad news for squeezed consumers, but at least the stability and independence of the SARB, certainly compared to other government institutions, helps our standing with global investors and ratings agencies. Forward rate agreements (FRA) already show the odds of a rate cut this year (at the November meeting) and have diminished over the past month. The exact timing of interest rate moves here and abroad is less important than the overall trajectory. Globally, the rate hiking cycle in developed countries is likely to be very shallow. Locally, there is still room for cuts over the course of the next year.

Chart 1: South African headline and core inflation

Chart 2: South African retail sales growth, year-on-year three-month moving average

Source: StatsSA