Safe for now, but ratings risk remains

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

After a round of credit ratings reviews by the three major ratings agencies, South African government bonds will remain part of the Citigroup World Government Bond Index (WGBI), but only just. The immediate risk of forced selling as a result of being excluded from this index has therefore abated for the time being. While each of the agencies has its own specific methodology for assessing creditworthiness, the common thread through all three reviews is that economic growth is too low, leading to pressure on Government’s finances, worsened by underperforming State Owned Enterprises (SOEs).

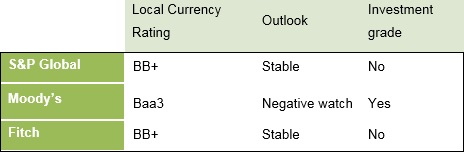

Fitch kicked off the much anticipated (or dreaded) round of ratings reviews by maintaining South Africa’s BB+ rating with a stable outlook. Fitch noted that while the fiscal outlook weakened, the ship could be steadied after the ANC’s elective conference. Failure to implement credible fiscal consolidation measures in February’s Budget could see the outlook changed to negative. To change the outlook to positive, the first step to regaining investment grade status requires improving governance (including of SOEs), reducing the budget deficit and, crucially, accelerating economic growth.

Deeper into junk status

S&P Global Ratings were not so kind, cutting both South Africa’s local and foreign currency ratings by one notch. It means the local rating drops to BB+ and is no longer investment grade, as expected. The foreign rating downgrade was unexpected, and places South Africa on par with Turkey and Brazil at BB, two notches into so-called junk status. Importantly though, S&P has a stable outlook on both local and foreign currency ratings, implying that the worst is over. Unless there is a further substantial deterioration in governance, debt metrics or growth, there is no need for further downgrades as the rating already reflects the current reality.

Moody’s on hold

Moody’s decision was therefore key. Moody’s placed South Africa’s rating on negative watch, which means the next move is a downgrade. But the rating for both local and foreign currency bonds remains investment grade at Baa3, and therefore the local bonds still qualify for inclusion into the WGBI. Moody’s will wait to see whether Government announces credible fiscal consolidation measures and economic reforms in the February budget. Failure to do so will lead to a downgrade.

What are the implications?

The rand briefly lost around 2% against the dollar after the announcement, but the overall market impact of the downgrades was limited as markets respond to the factors that give rise to ratings changes – the growth and fiscal outlook – long before the ratings agencies do. Much of the bad news, including the downgrades, have been priced in. In terms of the local economy, the main impact is negative sentiment. There has been an unusually high level of attention given to what used to be a fairly arcane corner of finance and South Africans have spent the better part of the past two years worrying when the sword will drop (and we will have to wait a few months more). There is no doubt that this has damaged business and consumer confidence. But the downgrades have also played a role in keeping interest rates higher than they need to be.

Rates unchanged

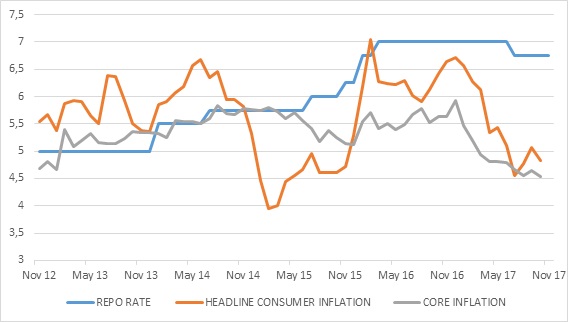

Ahead of the ratings reviews, the Reserve Bank’s Monetary Policy Committee (MPC) kept the repo rate on hold as widely expected. The Reserve Bank has also for long been concerned that potential capital outflows due to downgrades could cause a sell-off in the rand. The firmer global oil price has also emerged as a factor that will not only raise the domestic inflation profile somewhat, but could also lift global inflation, prompting faster interest rate increases in other countries, in turn causing capital to leave South Africa.

The Reserve Bank lifted its inflation forecast somewhat, but the extent of the increases is limited by conservative assumptions on electricity tariff increases and global oil prices. Inflation is expected to remain below, but close to the 6% upper end of the target range throughout 2018 and average 5.5% in 2019.

Headline consumer inflation fell to 4.8% year-on-year in October from 5.1% in September. Food inflation has moderated to 5.3% from 11% at the start of the year. Petrol inflation was 10.8% in October. It will dip to around 8% in November due to base effects, but because of the current average under-recovery of 70 cents per litre, petrol inflation could rise to 15% in December.

Core inflation at five-year low

Core inflation – excluding food and fuel prices – fell to 4.5%, the lowest level in five years. Over this five year-period, core inflation did not exceed 6%.The big swings in headline inflation over this period were mainly caused by food and oil price volatility, worsened by the big fluctuations in the exchange rate. But the fairly steady path of core inflation indicates a lack of underlying inflationary pressures, partly because of a weak economy.

The other notable driver of inflation over the past five years has been electricity tariffs, rising on average 8% (13% over the past ten years) although the pace of increase has slowed to 2.2%. But electricity tariffs are not linked to domestic demand, and firms and consumers have very few other options. It can therefore be considered to be closer to a tax than a price increase. What the SARB is concerned about is whether there are second-round effects of firms hiking their output prices in response to higher tariffs. There is little evidence of this. Nersa is expected to make an announcement on Eskom’s application for a 20% tariff increase in early December.

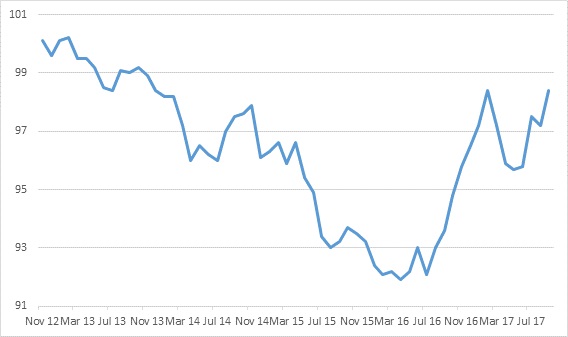

The Reserve Bank’s view of economic growth is “subdued but positive”. The 2017 GDP growth forecast was bumped up a touch from 0.6% to 0.7%. From this depressed level, real growth is expected to almost double to 1.2% next year and 1.5% in 2019. These numbers are similar to the three ratings agencies’ forecasts. The SARB’s composite leading indicator increased further in September, confirming that growth is picking up moderately.

For the first time, the Reserve Bank also published a forecast of interest rates, generated by its economic model. It suggests three 25 basis points increases in the next two years. Importantly, this is what the forecast model suggests the MPC should do, not what the MPC plans on doing or believes it should do. Interest rate decisions are based on incoming data and therefore the MPC meets every two months to assess the latest numbers and how they impact the outlook. However, the general public is unlikely to understand this distinction, and likely to believe that the SARB is signalling higher rates, and adjust behaviour accordingly. This could achieve the aim of higher interest rates, without having to actually hike rates. But unfortunately it does mean that rate cuts are all but ruled out, despite inflation expected to be within the target range over the next few years.

The kindness of strangers

Given our domestic frailties, South Africa continues to rely on the kindness of strangers. Strong global growth could help lift our own growth rate above the anaemic levels currently predicted. Crucially, demand for high yielding emerging market assets still outweighs domestic factors such as politics, fiscal risks and downgrades. Within our peer group, South Africa has gone from one of the best-rated to the worst-rated in terms of the spread (extra yield) investors demand over US bonds. But as long as this demand persists – which in turn will depend greatly on the path of interest rate hikes in the US, global growth, and investor risk appetite - South Africa should benefit from capital inflows, irrespective of its rating.

Responding to downgrades

The muted market response to the downgrade reiterates that investors should not over-react to negative news headlines. Often, as is the case with the ratings changes too, the bad news is already reflected in market prices. On Monday morning following the weekend’s ratings announcements, bond yields were lower and the rand had strengthened. Investors’ long-term returns often suffer greater damage from knee-jerk responses to such events, than from the events themselves. However, if there were to be further negative surprises, one would expect the rand to come under pressure. Our strategies currently have more than 50% exposure to rand-hedges directly and indirectly and should benefit from currency weakness.

Table 1: South Africa’s local sovereign currency ratings

Source: Ratings agencies

Chart 1: Consumer inflation and the repo rate, %

Source: Datastream

Chart 2: SA Reserve Bank composite leading economic indicator index

Source: Datastream