Retail sales growth exceeds market expectations, but momentum soft

Sanisha Packirisamy, Economist at MMI Holdings.

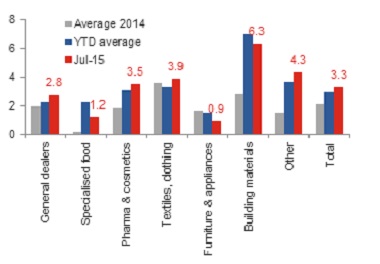

Stats SA reported a 3.3% y/y rise in retail sales volumes in July, lower than the (upwardly revised) 3.8% y/y growth rate reported in June, but notably higher than the 2.4% y/y increase captured by the INET BFA consensus estimate.

Growth in building material sales outperforms

Building material sales volumes continued to track well, increasing by 6.3% y/y in July down from 7.0% y/y in June, but significantly higher than the 2.9% y/y average reported over 2014 as a whole (see chart 1). At first glance strong building material sales appears at odds with low residential and non-residential investment rates. Growth in residential investment has declined by an average 6.3% p.a. since the global financial crisis (GFC), while non-residential investment decreased by an average 0.3% p.a. over the corresponding time period. Nevertheless, we suspect that smaller building contractors have been benefiting from an increase in home improvement activity, boosting the demand for hardware and building materials.

Chart 1: Average growth in retail sales volumes (% y/y)

Source: Global Insight, Momentum

Robust growth of 4.3% y/y followed in the “other” retail sector, which largely includes jewellery, sporting equipment and reading material. In contrast, growth in sales volumes by furniture and appliance retailers remained fragile. Volumes inched higher by 0.9% y/y as demand for durable goods deteriorated further in light of challenging economic conditions. Nonetheless, clothing and footwear spend has held up reasonably well despite mounting consumer headwinds, managing a 3.9% y/y rise (in real terms) in July. This can be partly attributed to attractive and competitive pricing as recently alluded to by the South African Reserve Bank (SARB) in their latest (September) Quarterly Bulletin.

Quarterly momentum slowing in light of gloomy consumer and retailer sentiment

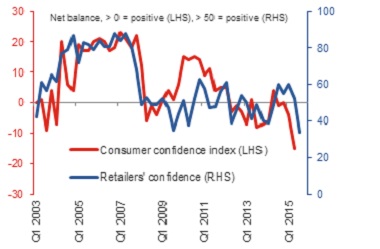

Although retail sales growth remains reasonably positive in year-on-year terms, near flat growth was reported on a month-on-month basis. Moreover, the seasonally adjusted annualised growth rate observed between May-July and February-April dropped to 0% indicating a softening in retail sales momentum. This appears to be in line with the recent plunge in both retailer and consumer confidence levels (see chart 2) as surveyed by the Bureau of Economic Research (BER).

Chart 2: Depressed retailer and consumer confidence levels

Source: Stats SA, Global Insight, BER, Momentum, quarterly data up to 3Q15 for retailer confidence

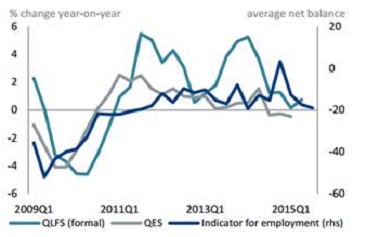

We see a number of factors keeping household consumption spend under pressure over the next year and a half. Although real wages are expected to benefit this year as a result of lower inflation, we expect rising inflation in 2016 to partly erode real disposable income growth. Furthermore, the outlook for employment remains benign. While the Stats SA Quarterly Employment Statistics (QES) survey suggests outright job losses in 1Q15, the Quarterly Labour Force Survey (QLFS) indicated a marginal uptick in jobs growth in 2Q15. Nevertheless, forward-looking indicators of employment remain bleak. The BER’s net hiring indicator shows a net balance of 20% of firms expecting to scale back on employment in the near term (see chart 3).

Chart 3: Net negative hiring intentions

Source: BER

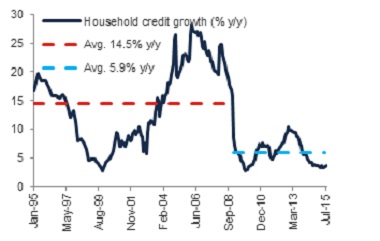

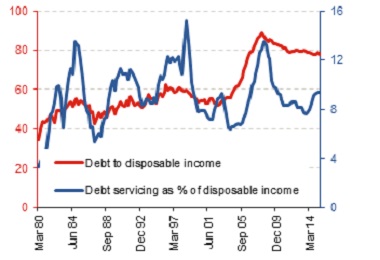

Household credit growth slowed significantly since 2009 (see chart 4), averaging 5.9% y/y from a 14.5% y/y average recorded between 1995 and 2008. More recently credit growth has dipped even lower as household debt levels remain onerous (see chart 5) and as bank lending criteria remain relatively stringent.

Chart 4: Benign household credit growth

Source: Global Insight, SARB, Momentum

Chart 5: Households are still relatively highly indebted

Source: Global Insight, SARB, Momentum, data up to June 2015

Although a rising interest rate environment is likely to have less of an impact on lower and middle-income earning consumers that are more exposed to fixed-rate unsecured loans, higher interest rates could dampen spend at the upper end. Additionally, a dip in equity prices could dent wealth ratios which have started to roll off from elevated decade-high levels.

No change to weak SA consumer view

Rising inflation, poor employment growth, relative household indebtedness, higher personal income taxes and muted household credit growth are dampening confidence and constraining consumers’ ability to spend. Slowing momentum in retail sales corroborates our view that domestic demand will likely remain soft well into 2016.