Resurgent rand in a changing global environment

Dave Mohr, Multi-Manager at Old Mutual.

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

It was very easy to be pessimistic about South Africa’s future at the end of 2015 when the rand collapsed even further after the shock removal of Finance Minister Nene. Many investors wanted to flee local asset classes completely. With the benefit of hindsight, that was the worst possible time to go offshore. As investors, we obviously don’t have the benefit of hindsight, but we can make sure that our risks are appropriately spread and managed and that our investment decisions are based on the time horizon of a financial plan and not in reaction to short-term market noise.

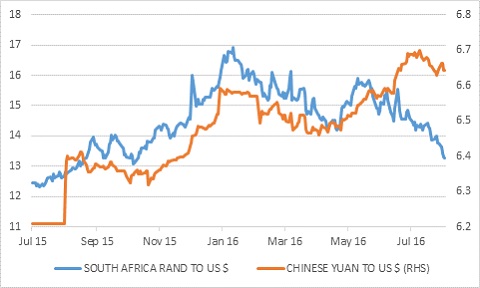

The events of the past twelve months are important in understanding the recent resurgence of the rand. A year ago the Chinese Government shocked global markets with a 1.9% devaluation of the tightly-controlled yuan on 10 August 2015. While small by global standards, it was one of the biggest one-day moves in the yuan ever. This set off a chain reaction of large scale volatility on world markets for the next few weeks. Commodity prices plunged, equities were hammered and risk appetite drained. This came against the backdrop of a rapid decline in the inflated prices of mainland Chinese-listed shares and an alarming deterioration of China’s economic data.

Early December 2015 into the first week of January saw a more steady but sizable yuan devaluation and a large decline in Chinese foreign exchange reserves, which stoked fears that the yuan would fall even more, exporting deflation to the rest of the world. The rand fell from R12.70 against the US dollar at the beginning of August to a record low of R16.90 in January.

Today, the market seems to be paying little attention to the yuan that is now pegged to a basket of currencies rather than just the US dollar. Therefore, China’s central bank is allowing the yuan to fluctuate by a slightly wider margin in daily trading. China’s macro data has certainly improved in recent months and concerns over a hard landing have diminished. Its foreign exchange reserves have stabilised, easing fears of massive capital flight.

The other big driver of global currency moves over the past year has been the outlook for US interest rates. The US Federal Reserve (Fed) increased rates in December last year and has indicated more hikes to come. Its most recent forecasts showed an expectation that the Fed funds rate will be around 3% in 2018. However, the Fed has found it really difficult to pull the trigger on a rate hike. Every time it looked set to go, a string of bad data or market volatility caused a hesitation. Nobody expects the Fed to hike aggressively over the next year or two and the exact timing of the next move is still uncertain.

Moreover, the difference between December 2015 when the Fed first hiked and now is that global yields have fallen substantially. For instance, Germany’s 10-year Government bond yield dropped from 0.6% last year to -0.16%. The equivalent US yield was 2.2% against the current 1.5%, while the Brexit-hit UK 10-year bond fell from 1.9% to 0.6%. Even Italian 10-year Government bonds’ yields are now trading at 1% from 4% three short years ago. In fact, there is currently fierce competition with other markets to attract scarce bonds. Last week, the Bank of England struggled to find willing sellers to buy bonds as part of its restarted Quantitative Easing programme. This briefly sent shorter-dated British Government bond yields into negative territory for the first time ever. The search for yield has therefore intensified, and one or two Fed hikes over the course of the next year are unlikely to derail it.

Therefore, it is important to put the rand’s recent rally in context: although it is one of the best performers against the US dollar this year, the rand is still weak and has not appreciated against the US dollar over any 12-month period since September 2011. This means that the currency will have to make up a lot of ground to retrace its recent losses. At the start of 2015 the rand was at R11.56 against the US dollar and its average for the year was R12.80. It was averaging R10.84 in 2014 and is at R15.17 against the US dollar in 2016 so far. It would probably be a bit of a stretch to get back to 2011, when the rand was trading at an average of R7.25 against the US dollar, commodity prices were still flying and there were no US interest rate hikes in sight. Nothing is impossible though. With sentiment now favouring emerging markets again and commodity prices firming up from historically low levels (in real terms), it is no wonder that the rand has done well.

Local Government election positive for investor sentiment

Against this more favourable global backdrop, local politics are supporting the rand for the first time in a while. The outcome of the 2016 Local Government Elections is positive from an investor’s point of view for a number of reasons. Firstly, the election was peaceful and once again well managed by the Independent Electoral Commission. Secondly, voters have shown that they are prepared to hold politicians accountable to their communities, especially in the metro areas. This strengthened South Africa’s democratic credentials and bodes well for longer term governance. Thirdly, all parties involved accepted the outcome of the polls. Lastly, local governments usually have no influence on macroeconomic policy and it is worth noting that the country’s two biggest parties both favour fairly conservative economic policies. The parties with “radical economic transformation” agendas failed to make big inroads, showing that the risk of a major shift to populist policies seems limited.

Searching for an exchange rate sweet spot

From a South African point of view, the ideal scenario is probably that the rand holds on to its gains but not appreciate too much. The rand will substantially lower the inflation trajectory forecast by the South African Reserve Bank (they are working on an assumption of R15 to the US dollar). This all but removes the need for further rate hikes.

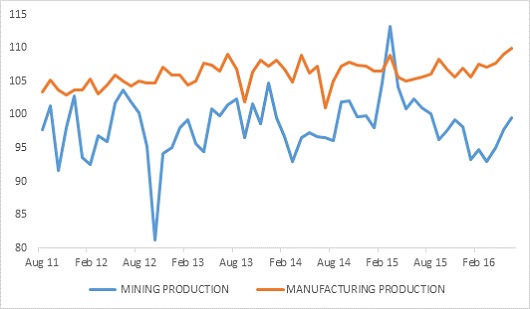

However, we still need a fairly weak rand to maintain the gains in tourism and exports and support domestic producers competing with importers. Data from last week underscores this. Local mining production fell by 2.5% in June from a year ago, but looking over the shorter term, a recovery seems to be underway. Output increased by 1.9% between May and June and by 4.2% in the second quarter. This improvement was mostly driven by a 25% surge in platinum output during the quarter. Iron ore output increased marginally, while coal output was flat. Gold output, despite the higher bullion price, contracted during the quarter.

Manufacturing production increased by 4.5% in June from a year ago, and by 2% during the second quarter. Production of vehicles and parts in particular had a strong quarter, as this sector is experiencing an export boom (sales of new vehicles in the domestic market are in the doldrums). Mining and manufacturing will therefore make positive contributions to second quarter Gross Domestic Product (GDP) growth. Second quarter GDP figures are likely to be positive, and might even surprise on the upside. At the very least, a technical recession (two consecutive negative quarters) and its negative effect on sentiment should be avoided.

Unfortunately, the rand does not have a history of settling down at the “right” level, but has historically had a tendency to over- or undershoot. This makes it difficult for investors and businesses to plan ahead.

Diversified, rational investing remains key

With the global environment changing so much over the past 12 months, some of last year’s investment strategies are struggling this year. This underscores the importance of appropriate diversification, since trends can change quickly and it is impossible to consistently time such turning points in the markets. It also highlights why you have to stick to a proper financial plan instead of letting emotions dictate your investment decisions.

Chart 1: Rand and yuan against the US dollar over the past year

Source: Datastream

Chart 2: South African mining and manufacturing production indices

Source: StatsSA