Recession in perspective

Dave Mohr, Chief Investment Strategist at Old Mutual Multi-Managers.

Izak Odendaal, Investment Strategist at Old Mutual Multi-Managers.

South Africans’ wounded pride was dealt a double blow last week with news of a technical recession and a further credit ratings downgrade. The South African economy declined in real terms at an annualised rate of 0.7% quarter-on-quarter in the first quarter of 2016, pushing the country into a technical recession. The consensus forecast was for gross domestic product (GDP), a broad measure of economic activity, to grow at 0.9% on a seasonally-adjusted and annualised basis, so the data disappointed expectations for a modest recovery.

The GDP numbers emphasise that the weakness of the domestic economy should not be understated and there certainly is an urgent need for policy makers to step up with the right measures and reforms to get the economy back on track. An end to political and policy uncertainty will help tremendously (not that we’re the only country facing political uncertainty; Theresa May’s gamble on a snap UK election failed miserably and she will now have to start Brexit negotiations with a minority government instead of a strengthened mandate).

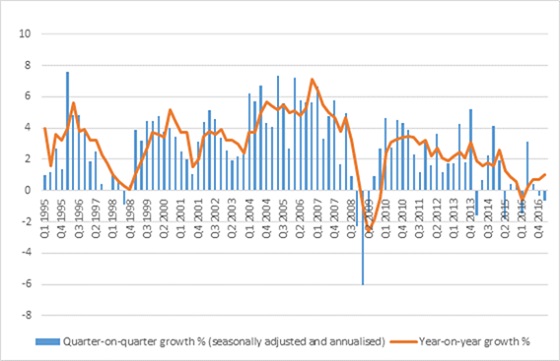

At the same time, investors should guard against overstating domestic economic weakness. Compared to the first quarter of 2016, the economy grew by 1% in real terms, the fastest growth rate in seven quarters (see chart 1). The economy contracted on a year-on-year basis early last year for the first time since 2009.

Similarly, while the expected one notch credit ratings downgrade by Moody’s is unfortunate, South Africa’s local and foreign currency ratings remain investment grade. This means local government bonds remain part of key global indices and there is no risk of forced selling (for now).

Technical recession not that significant

A technical recession is defined as two consecutive negative quarters (the fourth quarter of 2016 saw a 0.3% annualised contraction), but this is not always a very useful definition. For example, a sequence of very deep negative quarters interspersed with marginally positive quarters would mean an economy avoiding a technical recession, even though it shrank. In the current instance, we are already knee-deep into the second quarter. If this quarter is positive, the technical recession would be over, even if there was no meaningful improvement in underlying activity. Put slightly differently, it is incorrect to say that South Africa entered a recession last week, as was widely reported, since the recession started as early as September 2016 and is probably over already. The data available for the second quarter so far suggests an improvement in the beleaguered manufacturing sector, while the Standard Bank Purchasing Managers’ Index has been positive. A single quarter’s data is also subject to revision by StatsSA who may later find that the first quarter was actually positive. The 1998 recession, which followed the East Asian financial crisis, the Russian debt default and the local prime rate shooting up to above 20%, was subsequently revised away.

A more useful way to think of a recession is a deep, persistent decline in economic activity across a broad range of economic sectors. The actual decline in real GDP over the past two quarters is a mere 0.25% and hardly counts as deep. The improvement in fixed investment spending, which posted a second consecutive positive quarter following four deeply negative ones, is a positive development not usually seen during recessions. This suggests that business confidence is perhaps not as depressed as assumed.

Out of sync with the rest of the world, for now

The first quarter contraction is disappointing, not only because most analysts expected the economy to have bottomed in the fourth quarter of last year, but also because most major economies posted solid first quarter growth. Among our major trading partners, Eurozone growth of 2.4% has been particularly encouraging, while China grew 6.9% (China does not report quarter-on-quarter growth numbers). Even Brazil and Russia, plagued by deep recessions, posted positive first quarters. South Africa typically follows the global cycle with a lag and the recent improvement in global growth is another reason not to be too pessimistic on local prospects.

Agriculture and mining bounced back

GDP data, compiled by StatsSA, shows that the primary sectors of the economy (mining and agriculture) rebounded strongly in the first quarter. The 22% rebound in agriculture follows eight consecutive negative quarters. The secondary sector declined with manufacturing contracting by 3.7% and construction by 1.3%.

Services unusually weak

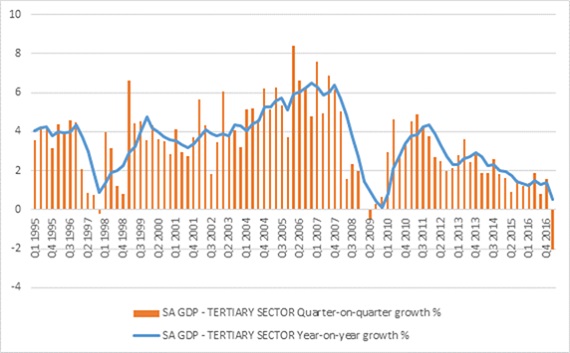

The tertiary (services) sectors declined by an unusual 2% in the quarter. Unlike the volatile primary and secondary sectors, services are normally quite steady. It was the first time the tertiary sector was negative in aggregate on a quarterly basis since 2009, and also the first time all tertiary sectors were negative at the same time. Financial and business services, the largest sector in the economy, declined by 1,2%. General government also contributed negatively to GDP, a sign that fiscal austerity measures are being implemented. The trade and accommodation sectors fell sharply by 5.9%. This reflected a 2.3% decline in household spending which in turn can be explained by a rise in inflation and a decline in income growth. Employee compensation (the economy-wide wage bill) growth slowed to 6%, which was eroded entirely by household consumption inflation.

However, the outlook is for inflation to fall, especially with the rand remaining firm and closing the week below R13 against the US dollar despite the recent recession and downgrade. The decline of the oil price to below $50 per barrel, despite renewed tensions in the Middle East between Qatar and its neighbours, also helps.

The SARB’s inflation forecasts will likely have to be lowered given these and other factors, its forecast for 1% growth this year is now at risk. Faced with both lower inflation and growth outlooks, the case for interest rates cuts has become very compelling.

The SARB has long emphasised the vulnerability of the rand to external shocks. With the Moody’s announcement out of the way, the next imminent hurdle is an expected US interest rate hike this week, which will be accompanied by new projections of where Federal Reserve officials see rates heading (the so-called dot plots). If there is no adverse impact on the rand, that will remove one of the main reasons not to cut. Lower rates and lower inflation should in turn take some pressure off consumers.

While the GDP data supports monetary policy easing, from a fiscal policy point of view it complicates matters. Slower-than-anticipated growth implies a potential shortfall in expected tax revenue.

A 3.2% real decline in exports and a rise in imports also detracted from growth. However, Reserve Bank data shows a positive trade balance of R57 billion in the first quarter, up marginally from the fourth quarter, as well as an improvement in the terms of trade (export prices relative to import prices). This suggests that the current account deficit is still on a narrowing trajectory, removing another long-held concern of the Reserve Bank.

What are the implications for investors?

The words “recession” and “downgrade” all over the media will not help the widespread pessimism. Ultimately though, what’s important is not to quibble with definitions, but rather to determine whether investors should alter their portfolios in response to this news. We’ve always cautioned against reacting to headlines, and this is no different. We’ve long held a view that local bonds are attractive. The Reserve Bank is even more likely to cut rates now, and that should be good for bonds. At the same time, we’ve maintained an underweight position in local equities, partly because the weak local economy weighs on domestically focused shares (although it is worth repeating that the JSE is largely globally focused these days). We’ve also maintained maximum global exposure on valuation grounds and as an appropriate diversifier. We have not made any changes to the Strategy Funds in response to last week’s news and they remain well positioned to navigate the current challenging environment and deliver real returns.

Chart 1: Quarterly and annual growth rates of SA gross domestic product (GDP)

Source: StatsSA

Chart 2: Quarterly and annual growth rates of tertiary sector

Source: StatsSA